What is Dollar Cost Averaging and How Can It Help You Maximize Investment Returns

An easy way to pay yourself first and lower your average cost

Buying low and selling high is how one maximizes investment returns. But how can I consistently buy low when asset prices change all the time? Haven't I been taught that trying to time the market is a fool's errand?

Spoiler alert: There is no secret way of consistently buying low. However, today's post is about a purchasing technique for long-term investors which can help smooth your costs: Dollar Cost Averaging. For volatile investments this technique can actually lower your average cost over time.

What is Dollar Cost Averaging?

Investopedia has a great article on Dollar Cost Averaging (called DCA in the rest of this post) where they describe DCA as "involves investing the same amount of money in a target security at regular intervals over a certain period of time, regardless of price." DCA is typically executed by automatic investments of the same amount of money each month or, in the case of pensions / 401(k)s, each pay period.

I am a big proponent of DCA for the following reasons:

- It is a good part of "pay yourself first budgeting": As I described in a recent post on that subject (Pay Yourself First Budgeting: Build Automated Savings and Investment Into Your Budget), building savings into your ongoing budget and having it invested automatically is a strategy that I recommend for everyone. It forces you to save as it eliminates the temptation to spend monies allocated to savings by keeping those dollars from ever getting into your hands

- It can help lower the average cost of your investments: This is a very important benefit of DCA as it helps you get on the path to "buying low". In the next section, I will walk through the mechanics of how this works

- It aligns with a passive investment strategy: As I stated in my article on Balancing Active and Passive Investments, passive investments are an integral part of any diversified portfolio and should actually be the base preference for investors. Using DCA to invest into index funds is an ideal way to build up the passive investment portion of your portfolio

- DCA reduces the time and effort necessary to research investments and set buy targets: While I have written a number of posts about how to value an investment, most people don't have the time and patience necessary to actively do the research and analysis. Without doing this legwork, it's very difficult to determine buy targets for investments. With DCA, one doesn't spend the time to determine a buy target. After having decided which passive investments one wants in their portfolio, DCA is a simple "set it and forget it" strategy to build that investment. Over time, DCA will lead to a smoothed out and, in many cases, lower average cost which increases your profit on that investment

How does DCA lower my average cost of volatile investments?

A major benefit of DCA is that it helps smooth out the costs of an investment. For investments which are volatile with both upward and downward swings, DCA can help reduce the average cost as you build up your position.

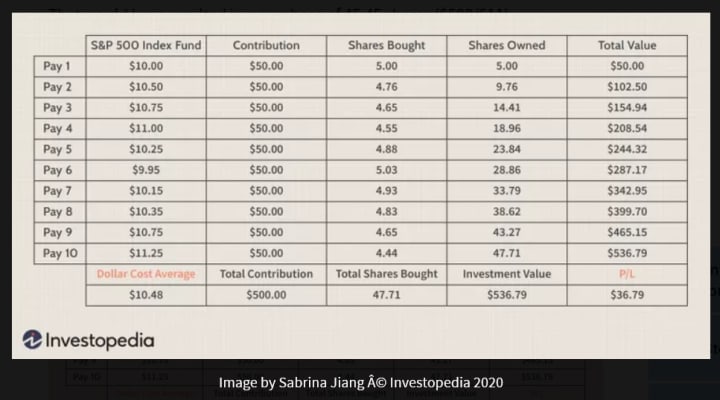

I'm going to lean on an example from the same Investopedia article that I cited earlier to illustrate how it works. In this example:

- A worker invests $50 per pay period into and S&P 500 index fund

- When prices rise, they buy less shares with that $50 and when prices fall, they buy more shares

Over time, because of the magic of mathematics, their weighted average cost of investments falls closer to the lower end of prices paid than the average. This sounds very counterintuitive so I want to provide a simple example of this magic:

- Say the worker buys $50 at $10/share and $50 at $12/share. They get 5 shares in the first purchase and 4.17 shares in the second for a total of 9.17 shares

- The average price per share turns out to be $10.91 (vs. $11 as many people might guess) because there were more shares bought at $10 than at $12 and the average price is a weighted average which puts more emphasis on purchases where more shares were bought

In the Investopedia example above prices paid per share ranged from $9.95 to $11.25, with the average coming in at $10.48, so DCA has helped bring the worker's average cost into the lower end of the distribution of prices that were paid. That's how DCA can maximizes your investment returns - it helps get you to "buy low".

Are there easy ways for me to get started with Dollar Cost Averaging?

Yes, there definitely are ways to get started with DCA that are easy to set up. The two big ones I use in my household are:

- Automatic deductions from paychecks into pensions: My wife and I both maximize our contributions to our pensions as part of our pay yourself first budgeting. In addition, as I shared in Make Your Pension Contributions, contributing to your pension has the added benefit of tax-advantaged investing and free matching funds from our employers

- Automatic transfers from our bank account to our brokerage account: Like most brokerages, the company with whom we invest offers the ability to set up automatic monthly withdrawals from our bank account that go straight into our investments. We had to first decide which investments we wanted to make and then it only took a few minutes to set up the automatic withdrawals online

This completes today's post on Dollar Cost Averaging and how it can maximize the return of your investments. The practical steps you can start taking from today's post are:

- Use DCA as an explicit part of your pay yourself first strategy, focused on passive investments: Set up DCA plans for your passive investments as part of a pay yourself first budgeting strategy. Use the two channels describe below

- Leverage the built in DCA option for your pension at work: As described in my post Make Your Pension Contributions, there are a lot of benefits (free money, tax advantages and access to investments that a typical retail investor doesn't always have) that come from investing in your pension, so take advantage of it. Being able to DCA is a built-in feature of your pension

- Set up DCA in your brokerage account or mutual fund: Brokerages and mutual fund companies offer the opportunity to set up automatic investments into mutual funds or ETFs. The same is the case for other investing platforms like Fundrise in the real estate space. Once you have determined where you would like to invest, contact your brokerage or mutual fund provider and set up automatic withdrawals that DCA into your investments

Thank you again for joining me on my journey to build financial literacy for young adults and their families. Please share any comments or questions that you have in the comments section. If you are interested in reading more of my posts, please access my author page (https://vocal.media/authors/sudhir-sahay) where you can see all the posts I’ve published. Also, if there are any topics you’re interested in my broaching in future posts, please let me know. In addition to the comments section, I can be reached at [email protected].

About the Creator

Sudhir Sahay

Sudhir Sahay is a Sales and Marketing executive and a father of two young men. Sudhir hopes to share his journey building basic financial literacy for his children and providing savings and investing advice to their friends and peers.

Keep reading

More stories from Sudhir Sahay and writers in Trader and other communities.

Balancing active and passive investments

The investing world is very challenging. We are constantly barraged by huge, big-name investment firms telling us to invest our money with them and sharing cherry-picked stories of the happy people who've chosen them. To top that off, they all promote multiple styles of investing, with every one of them having strong long-term results. How does an individual decide which is right for their unique needs? In particular, when it comes to choosing between two diametrically opposed styles of investing: passive versus active.

By Sudhir Sahayabout a year ago in Trader

The Rollercoaster Ride of a Trader's Career

Unveiling the Drama and Humor Behind the Trading World Wanted: Adventurous souls with nerves of steel, a passion for numbers, and a flair for risk-taking. Does this sound like you? Welcome to the chaotic and exhilarating world of trading. Strap yourself in for a wild ride filled with highs and lows, thrills and spills, wins and losses. In this article, we'll delve into the heart-pounding journey of a trader's career, where drama and humor mingle in a dance of chaos and order. Hold on tight as we explore what it truly means to embark on a path where fortunes are made and lost in the blink of an eye.

By Max Gachet6 days ago in Trader

Comments

There are no comments for this story

Be the first to respond and start the conversation.