Balancing active and passive investments

Optimize the balance based on availability of information and liquidity in the asset class

The investing world is very challenging. We are constantly barraged by huge, big-name investment firms telling us to invest our money with them and sharing cherry-picked stories of the happy people who've chosen them. To top that off, they all promote multiple styles of investing, with every one of them having strong long-term results. How does an individual decide which is right for their unique needs? In particular, when it comes to choosing between two diametrically opposed styles of investing: passive versus active.

I recently published a post providing background explanations of these two styles (Active versus Passive Investing), so please read that post if you haven't heard about these styles before. I ended that post saying that I would follow up shortly with details on how I approach determining the right mix of these two types of investments. That's today's topic.

Before I get into the factors that impact my mix of active versus passive by asset class, I want to start with why my base preference is passive investments over active. That base preference is due to the following:

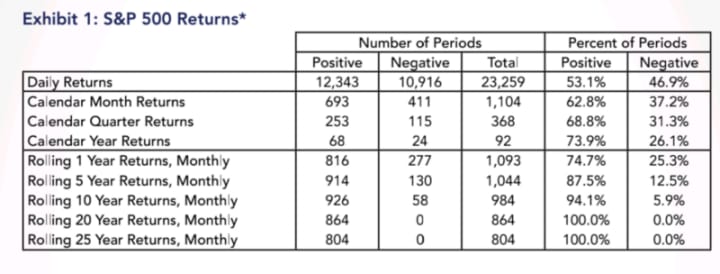

First, over the long term, most investment classes rise in value. As an example, the following table is for the S&P 500, a widely followed US stock market index, from Fisher Investments (Historical Frequency of Positive Returns, quoting data from Global Financial Data, Inc.)

As you can see, since 1926 when this data series started, there have never been any periods of 20 years or longer where the S&P 500 has had negative results. Over this very long time period, the index has risen on average by 11.82% per year (returns from 1928–2021 as quoted in S&P 500 Average Return in Investopedia). Just staying even with such a rising market using dollar-cost averaged investments should provide a meaningful level of return with limited likelihood of loss. That's exactly what I want from the core, safe part of my portfolio.

Next, on average, active fund managers underperform passive investments. Data from S&P Global in their latest SPIVA study shows that "Eighty-four percent of active managers underperform benchmarks after five years. That jumps to 90% after 10 years, and 95% after 20 years." Given the strong likelihood that passive will outperform active, unless I have reason to choose otherwise, I would go with passive.

Notwithstanding my bias towards passive, there are asset classes where having some share of my investment in active vehicles makes sense. I determine which asset classes and how much of a share should be active based on two criteria.

The level of information available for investments in that asset class

According to the Efficient Markets Hypothesis, a share's "price reflect[s] all information and consistent alpha generation is impossible." (Investopedia, Efficient Market Hypothesis (EMH): Definition and Critique). What this theory posits is that markets very quickly absorb and reflect any relevant information into an asset's price so it's always fairly valued. This implies that there is no likelihood that one could find incorrectly-valued assets unless they have information that isn't publicly available or widely disseminated. Information asymmetry is the core of this theory to me. Those who have more information are better placed to determine the true value of an asset.

Depending on asset class, there are different levels of information that are readily available. For example, anybody can find the latest earnings data on a large-capitalization stock such as Apple as they have to file their financial results regularly. On the other hand, it's very difficult to find detailed financial data for a commercial building (real estate asset) in a frontier economy in Africa. In between these extremes are asset classes such as wine. Not everyone has immediate access to information on the quality or value of wine, but with a little digging, one can find specialist magazines which provide pretty detailed ratings of wine quality and estimated value. Across these three example asset classes, there is a higher likelihood that the market inaccurately values wine than Apple stock. It's even likelier than that in the case of the commercial building.

From an investing viewpoint, it is instances such as the frontier-market commercial building with very limited information where active investing with a focus on deep research can uncover and take advantage of mispriced assets. So, when I think about active versus passive investing, asset classes with lots of available information should be invested in primarily through passive vehicles while low-information asset classes should have a higher mix of active.

Liquidity in the asset class

The other factor I look at is how quickly I can get my money out of an investment in times of need. In financial markets, that's called liquidity: "Liquidity generally refers to how easily or quickly a security can be bought or sold in a secondary market. Liquid investments can be sold readily and without paying a hefty fee to get money when it is needed." (SEC in Investor.gov, Liquidity (or Marketability)). Liquidity to me is a measure of the safety of my money in trying times. When there are challenges or panics in financial markets, I want any of my investments in illiquid assets to be actively managed as an active manager can be proactive and quickly get my money out of that investment before liquidity dries up. Passive investments don't do that as they require me to make the decision to take that money and then put in a sell order - by the time I get around to that, it may not be possible to get my money out of an illiquid asset.

While one hopes that there won't be financial panics or other situations where liquidity dries up, that does happen. I'd like to have the comfort in my mind of knowing that there is an active level of oversight in my investments in those asset classes which are lower in liquidity.

Putting the two factors together

To determine what share of my investments in a given asset class should be active versus passive, I use a simple 2x2 chart mapping out the two factors I mentioned above. I put the amount of information available for the asset class and the y-axis and liquidity in the x-axis. To help illustrate how I use the chart, I've mapped out a few asset types in the chart below.

Asset classes which are high information and high liquidity (top, right quadrant) should be all passive. The further down and the further left an asset class is on this chart, the higher the percentage of active should be. However, given my bias towards passive investments, there shouldn't be any asset class with 100% active investments.

This completes today's post on balancing between active versus passive investing. The practical steps you can start taking from today's post are:

- Look across the asset classes in your portfolio: Divide them into two dimensions. Those which are high information versus low and those whose assets are more liquid versus less

- Map out the asset classes in the 2x2 matrix I referenced in this article: Use level of information and liquidity of assets as the two axes

- Determine the relative share of each asset class which should be passive investments: The higher the amount of information and the more liquid an asset class, the higher the passive share should be. On the matrix, these asset classes are in the top, right quadrant

- Slowly adjust your portfolio over time to match the optimal mix of passive versus active: If your portfolio mix differs from the optimal, take time to move that mix. In investing, it's always better to move slowly than to make quick, radical changes

Thank you again for joining me on my journey to build financial literacy for young adults and their families. If you are interested in reading more of my posts, please access my author page (https://vocal.media/authors/sudhir-sahay) where you can see all the posts I’ve published. If you have any questions on today’s post of if there are any topics you’re interested in my broaching in future posts, please let me know. I can be reached at [email protected].

About the Creator

Sudhir Sahay

Sudhir Sahay is a Sales and Marketing executive and a father of two young men. Sudhir hopes to share his journey building basic financial literacy for his children and providing savings and investing advice to their friends and peers.

Keep reading

More stories from Sudhir Sahay and writers in Trader and other communities.

Active versus Passive Investing

Maximizing investment returns in a safe manner requires balancing a number of tradeoffs. First, what you earn through your investments versus the transaction costs and taxes you have to pay. All else held equal, you want the highest net returns. Second, the balance between the amount of risk you take and expected return — as I talked about in my recent post on balancing safe but boring investments with risky but exciting ones, you want the core of your portfolio to be boring but safe. A key variable for managing those tradeoffs is the mix of your active versus passive investments.

By Sudhir Sahayabout a year ago in Trader

"Stride in Style: Discover the ALDO Men's Albeck Oxford"

In the realm of men's footwear, finding the perfect balance between style, comfort, and versatility can often feel like an elusive quest. Yet, amidst the sea of options, there emerges a beacon of excellence that embodies these qualities seamless: the ALDO Men's Albeck Oxford. As a distinguished member of ALDO's esteemed lineup, the Albeck Oxford stands as a testament to the brand's commitment to crafting footwear that not only exudes sophistication but also delivers unparalleled comfort and durability.

By Kim Long Nguyệt Ngữ3 days ago in Trader

2023 Fashion Designer Shoes Men Casual Platform Sneakes Lace Up Trainers Student Sneakes Mens Vulcanized Shoes Zapatillas Hombre

In the ever-evolving world of fashion, footwear has become more than just a functional accessory; it's a statement of style, personality, and individuality. One of the most intriguing trends to emerge in recent years is the fusion of casual comfort with elevated design, epitomized by the rise of platform sneakers for men. These shoes seamlessly blend streetwear flair with high-fashion sensibilities, creating a versatile option that can effortlessly transition from day to night, casual to formal.

By Wedson Vegasabout 18 hours ago in Trader

How the Harvest Mouse Came to Suisun Bay

A long, long time ago there was a family of harvest mice. Mice are common, but these were unique – born to those who had lived in the salty, marshy bay for many generations, these mice ate and drank from the sea as well as the land and rivers. For generations, there were only the southern families, scattered along the marshes of Corte Madera and in the San Francisco Bay (U.S. Fish & Wildlife, 2013). One family, however, would undergo strife and conflict before reaching a whole new world. What became of them after is another tale entirely – but this is how their story begins.

By Taylor Inman7 days ago in Fiction

Comments

There are no comments for this story

Be the first to respond and start the conversation.