The Federal Reserve’s Federal Open Market Committee (FOMC) Will Meet This Week and Ask: “Are We There Yet?”

Monetary Policy in Perspective

The answer is that monetary policy is so restrictive that the Fed could justify lowering policy rates. The Fed’s preferred inflation metric, core PCE (which measures consumer prices excluding food and energy components), is now rising at a yearly pace of +2.9% (December 2023), down from a peak growth pace of +5.6% (February 2022). The significant difference between core PCE and core CPI (Consumer Price Index) is that the former weights the price components based on the changing preferences of consumers. Suppose the price of strawberries rises and individuals switch to consuming more blueberries. In that case, blueberries will be weighted more heavily (when constructing the price index) as the shift in demand occurs.

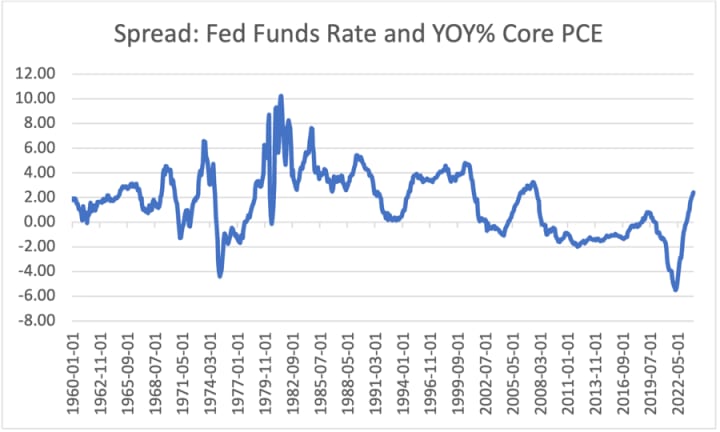

The spread between the federal funds rate and the yearly rise in the core PCE has been at its most expansive levels since October 2007, or 66% higher than its historical average. Although this gives the Federal Reserve enough leeway to cut policy rates, the more salient question is whether it needs to. Real GDP for Q4 2024 rose by +3.3% or about 85% above the economy’s regular potential growth rate. With such growth rates, it is like asking a motorist whether they should stop and fill up their gas tank after driving for a long time at the first sign of a gas station. The obvious answer is that motorists will be motivated to stop and fill up only if they are close to running out of gas. That means that if the vehicle runs more efficiently due to higher gas mileage (a.k.a., the economy is thriving), the motorist/Fed may not need to act!

Source: The Federal Reserve and the Bureau of Economic Analysis

Are We There Yet?

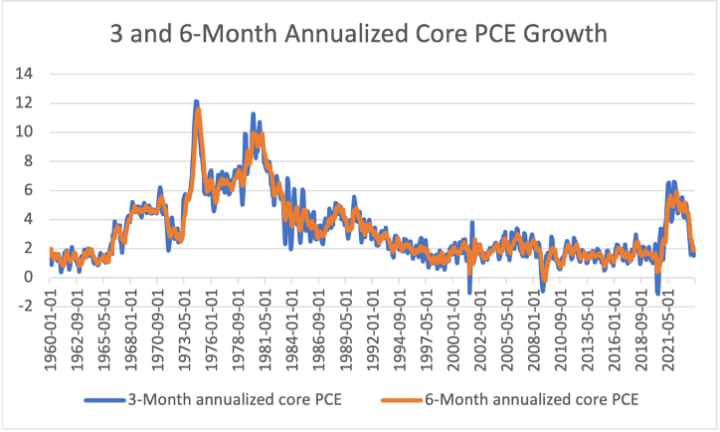

Others might say, “Wait a minute! The Fed’s goal is to bring the core PCE inflation rate to a yearly growth pace of +2.0%, and at +2.9%, inflation is still running hot.” Yes, that is true, but when you look at the 6-month and 3-month annualized growth rates, core PCE is rising at a yearly pace of +1.9% and +1.5%. That means the Fed has already accomplished its +2.0% goal on a 3 and 6-month annualized basis!

Source: The Bureau of Economic Analysis

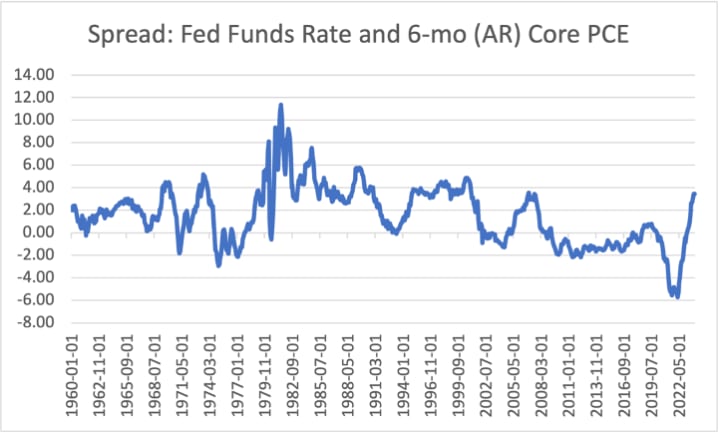

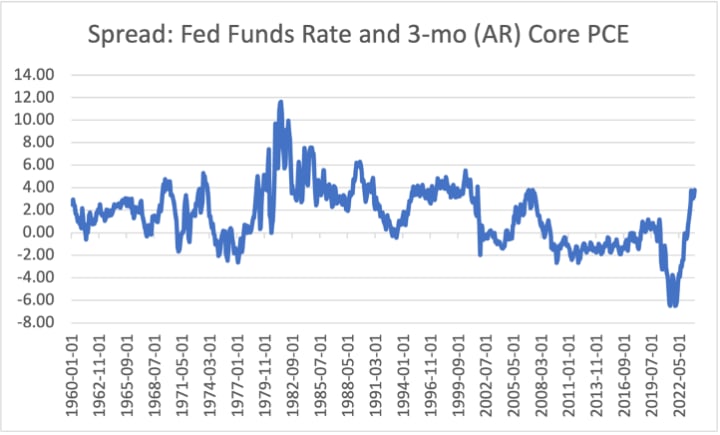

It should come as no surprise that the spread between the federal funds rate and the 6-month annualized growth rate in core PCE is now more than double its historical average. A similar result is generated using the spread between the federal funds rate and the 3-month annualized core PCE growth rate!

Source: The Federal Reserve and the Bureau of Economic Analysis

Source: The Federal Reserve and the Bureau of Economic Analysis

We leave it up to the reader to decide whether the Fed’s job will be done only after the core PCE is down to +2.0% on ALL three metrics, namely, on a yearly, 6-month, and 3-month annualized basis. Still, others may wish to be even stricter and say that the Fed should keep depressing the economy until prices are lower to compensate for the prior inflation excesses, even though these criteria have never been applied to any global central bank! During a recent in-person client presentation, one participant chuckled and told me that if this causes a significant recession, we can always blame the current administration or the central bank!

Why is the Federal Reserve Being So Cautious?

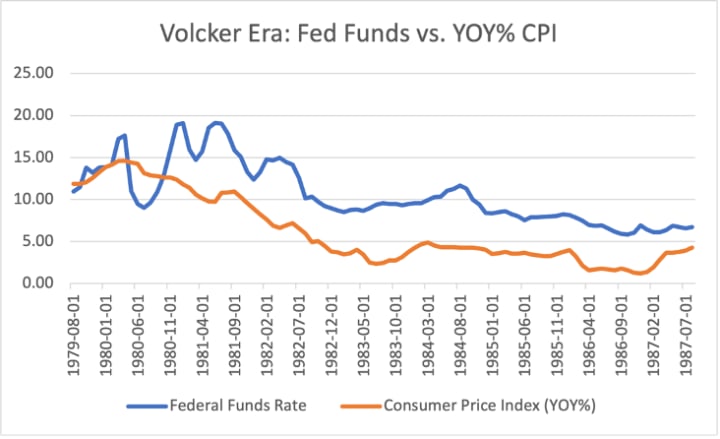

The Federal Reserve remembers the inflation battle that Paul Volcker experienced during his tenure (August 1979 -August 1987). In April 1980, Volcker began lowering the Fed funds rate from 17.6% (April 1980) to 9.0% (July 1980), only to see the CPI drop only from +14.6% to 13.2%! That was a crushing disappointment, causing the Fed to push the Fed funds rate back to 19% (July 1981)

It is interesting to hear so many complaints about the Fed today (with a 5.3% federal funds rate) because the CPI peaked at 9.1% (June 2022) and is down only 2.9% (Dec. 2023). I lived through this period, and if I had a time machine, I could show everyone that back in 1981, if people had observed the CPI rising by 2.9%, they would have invited their favorite high school marching band to celebrate!

Source: The Federal Reserve and the Bureau of Labor Statistics

Summary and Concluding Thoughts

The Fed critics are more assertive today than during the 1980s, even though we all agree that if inflation slows to a +2.0% growth pace, it will not reverse the +9.1% growth pace recorded in June 2022. Imagine if Argentina’s central bank, overseeing a +211% yearly inflation rate (December 2023), was asked to keep its monetary policy restrictive until its prior inflation rate was reversed!

Nothing is wrong with demanding more, but we should never forget history and realize that the Fed is doing better today using the judging criteria employed 50 years ago.

It is amusing that, with an economy registering a +27.9 trillion-dollar nominal GDP figure in Q4 2023, we get upset if the CPI was +0.1% higher than the market expected! The range of errors in all these estimates is so high that no one should be surprised if the correct figure were +0.2 or even -0.2 %!

The only sure thing is that the yearly CPI growth rate of +2.9% (Dec. 2023) is much lower than the +14.6% (April 1980) figure. That means we should acknowledge that as bad as our inflation growth rate might seem today, it is significantly lower than what we witnessed 43 years ago under Paul Volcker, who was widely respected for his inflation-fighting credentials!

About the Creator

Anthony Chan

Chan Economics LLC, Public Speaker

Chief Global Economist & Public Speaker JPM Chase ('94-'19).

Senior Economist Barclays ('91-'94)

Economist, NY Federal Reserve ('89-'91)

Econ. Prof. (Univ. of Dayton, '86-'89)

Ph.D. Economics

Reader insights

Nice work

Very well written. Keep up the good work!

Top insight

Expert insights and opinions

Arguments were carefully researched and presented

Keep reading

More stories from Anthony Chan and writers in Trader and other communities.

Why Has Consumer Confidence Suddenly Rebounded?

The relationship between consumer confidence and the economy's performance has been a subject of intense discussion within financial markets over the past year. Why has consumer confidence been so weak while the U.S. economy appears to have expanded by 2.5% in 2023, with an unemployment rate near 50-year lows? The only logical explanation is that consumers have been upset with high inflation readings that have prevented them from maintaining their standard of living.

By Anthony Chan3 months ago in Trader

the best sofas on the market!

In the world of interior design, sofas occupy a central place, not only as functional furniture but also as essential decorative elements. They are the family gathering place, the symbol of comfort and conviviality in our living spaces. Today we witness the diversity and innovation in the world of sofas, with models that combine style, comfort and functionality in an exceptional way.Among the options available on the market, examples such as the "GrekPol Paris Corner sofa in corduroy fabric Poso with convertible function and storage space - Universal - Beige" offer an elegant combination of contemporary design and practicality, with a convertible function and integrated storage space, ideal for small spaces. Similarly, the "HOMCOM Sofa Convertible 3 Seater Scandinavian Design Tilt Adjustable Backrest 3 Levels Central Fold-Down Backrest 2 Glass Holders Solid Wood Linen Gray" seduces with its sleek Scandinavian design, adjustable backrest features and versatile character, adapted to different interior layouts. In addition, models such as the "SILAPE - Santi Convertible Corner Sofa - with Chest - in Leatherette and Fabric (Madryt 1100 + Berlin 01, Left Angle)" offer a modern and sophisticated aesthetic, combined with practical functionality thanks to its integrated storage space. These examples illustrate the diversity and innovation that characterize the sofa market today, while emphasizing the increasing importance given to the combination of comfort, style and functionality in the choice of furniture for our interiors. In this article, we will explore in more detail the different sofa options available, highlighting their distinctive features and benefits, in order to help consumers find the perfect sofa for their living space.

By Alicia Lhotellier5 days ago in Trader

Europeans reject Chinese cars.

China's car industry has changed over the course of the last ten years, from delivering fundamental western clones to making vehicles that equivalent the world's ideal. As the assembling force to be reckoned with of the world, China is likewise creating them in enormous volumes.

By Phumlani Mdlalosea day ago in Trader

Turning Pages of Life

Life’s like a book — some parts are good, others not so much. Still, keep turning the pages; you might find the best chapter next. If someone hurts you, choose to forgive or just let it be, but never change who you are for them.

By Emily Chan - Life and love sharing5 days ago in Poets

Comments (1)

Thank you, Shawn Kelly for reading my analysis on the Federal Reserve!