Oil Market Paradox

Low Prices Despite OPEC+ Supply Cuts

OPEC's June 2, 2024, virtual meeting, which included 22 Energy Ministers, extended their prior supply cuts. Previously, OPEC + reduced supply by 5.9 million barrels per day (mb/d), including 3.7 mb/d through the end of 2024 and an additional 2.2 mb/d of voluntary cuts by selected its members through the end of June 2024. In the latest agreement, the 3.7 mb/d supply cuts will now end at the end of 2025, and the voluntary 2.2 mb/d supply cuts will now end at the end of 2024. This means that OPEC+ will continue to remove 5.7% of Global oil supply from the market!

Why Aren’t Oil Prices Sharply Higher?

Even with OPEC’s strategy of restricting its oil supply to the market, OPEC faced the risk that the world could be drowning in oil if it had discontinued its current strategy. The narrowing spread between the spot price of oil and futures prices (a.k.a. backwardation) suggests that oil supply was becoming more abundant.

West Texas Intermediate (WTI) touched $86.91 per barrel on April 5, 2024, and has since moved lower. Despite the death of the Iranian President in a mysterious plane crash, the Middle East war between Israel and Hamas, and the continuing Russian-Ukraine conflict, WTI prices have failed to move higher.

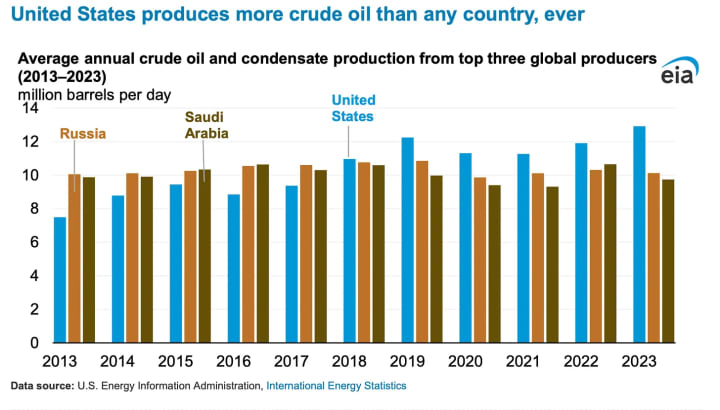

Thanks to its shale oil, oil sands, and regular oil-producing wells, the U.S. is now producing crude oil at its highest output level in history, helping to restrain prices. The U.S. joins other non-OPEC countries that have also boosted output.

According to the IEA, total U.S. liquified energy production has continued to grow with output of 18.5 mb/d, 19.0 mb/d, 20.4 mb/d, 21.5 mb/d, and 22.2 mb/d during April 2020, April 2021, April 2022, April 2023, and April 2024, respectively.

Why is U.S. Liquified Energy Output Larger Than U.S. Crude Oil Output?

The U.S. liquified energy output figures include crude oil production and natural gas liquids (NGLs) produced when extracting or processing crude oil and natural gas. NGLs are hydrocarbons produced when extracting or processing crude oil and natural gas, generating ethane, propane, butane isobutane, and pentanes. In a typical month, NGLs augment U.S. crude oil output by about 50 percent. Processing natural gas generates NGL output, so as U.S. natural gas production has increased, NGL output has moved higher in tandem.

Total U.S. energy output (crude oil plus NGLs) has also increased its share of global energy output (including NGLs). In April 2020, April 2021, April 2022, April 2023, and April 2024, Global energy output levels were at 99.4 mb/d, 94.0 mb/d, 98.8 mb/d, 101.5 mb/d, and 102.1 mb/d, respectively.

Summary and Concluding Thoughts

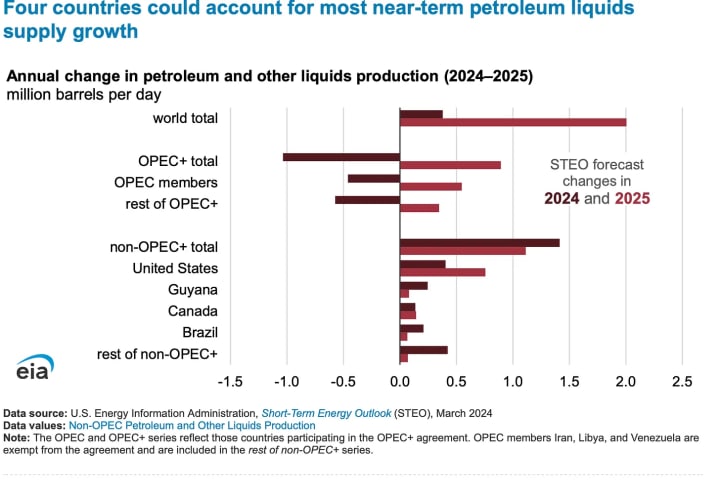

Despite OPEC+ supply cuts, WTI prices remain below the highs of $145.29 or $86.91 observed on June 29, 2008, and April 5, 2024, respectively. Global supply has continued to grow due to the supply growth emanating from the United States, Canada, and other non-OPEC countries. Still, one must acknowledge that geopolitical risks continue to pose a potential upside pricing risk.

Looking into the future, we have two U.S. presidential candidates who are likely to continue supporting increases in energy output. In a recent fundraising event, former President Trump asked oil executives to help him raise $1 billion for his campaign so he could be reelected and honor his “drill, baby drill” campaign promise. There is little doubt that U.S. energy output would surge if he is reelected.

In contrast, despite struggles with climate energy activists, President Biden has presided over a period during which the U.S. has produced the highest energy output in history, which will likely continue if he is reelected.

Still, from a nonpartisan perspective, the rhetoric from the campaign trails suggests that the U.S. energy supply will likely rise more aggressively under a future Trump administration than in a second-term Biden administration. However, because increasing energy output is a polarizing topic, I will leave it to the reader to decide whether they are in favor or against increasing U.S. fossil fuel output.

Finally, there is little doubt that with the actions undertaken by OPEC + today, oil prices are unlikely to revisit their 2024 or 2008 highs unless other risk catalysts enter the picture!

About the Creator

Anthony Chan

Chan Economics LLC, Public Speaker

Chief Global Economist & Public Speaker JPM Chase ('94-'19).

Senior Economist Barclays ('91-'94)

Economist, NY Federal Reserve ('89-'91)

Econ. Prof. (Univ. of Dayton, '86-'89)

Ph.D. Economics

Enjoyed the story? Support the Creator.

Subscribe for free to receive all their stories in your feed. You could also pledge your support or give them a one-off tip, letting them know you appreciate their work.

Keep reading

More stories from Anthony Chan and writers in Trader and other communities.

How Strong Is the U.S. Economy

Deciphering the state of the U.S. economy is an intriguing challenge, given the polarizing views we hear daily from various sources. On one hand, there's a narrative of prosperity; on the other, there's a narrative of impending doom. This dichotomy engages our curiosity and prompts us to seek a balanced perspective. To understand this issue, we consult our unbiased credit markets, where people put money, not politics, to work to settle this question.

By Anthony Chan2 months ago in Trader

How Do Businesses Generate Data for MIS Reports?

Data has become the primary component of strategic decision-making in today's corporate atmosphere. Management Information Systems or MIS reports are necessary documents that present information on various facets of the business including operational and customer relations. MIS reports provide accurate and detailed information about the business that helps companies track performance, forecast future trends, and plan competently.

By Prasanth M7 days ago in Trader

Dollar rebounds as Fed's Williams talks down rate cuts

NEW YORK (Reuters) -The dollar rebounded on Friday after Federal Reserve Bank of New York President John Williams pushed back against the market’s rate cut expectations, though the dollar indexremained on track for its worst weekly performance in a month.

By mathias delight7 days ago in Trader

Comments (1)

Very informative appreciate the both sides view on the political angle