Just How Catastrophic Is Digital Lending in Kenya?

Digital loans have led many Kenyans into a debt spiral with their notoriously high-interest fees.

Digital lending is on the uptake across the world and Kenya hasn’t been left behind. This trend is fueled partly by the country’s harsh economic environment and partly by the upsurge of smartphone adoption among the youths. Of course, this has made it easier and more convenient for borrowers to access loans, either for their household needs such as rent and food or for working capital for their SMEs.

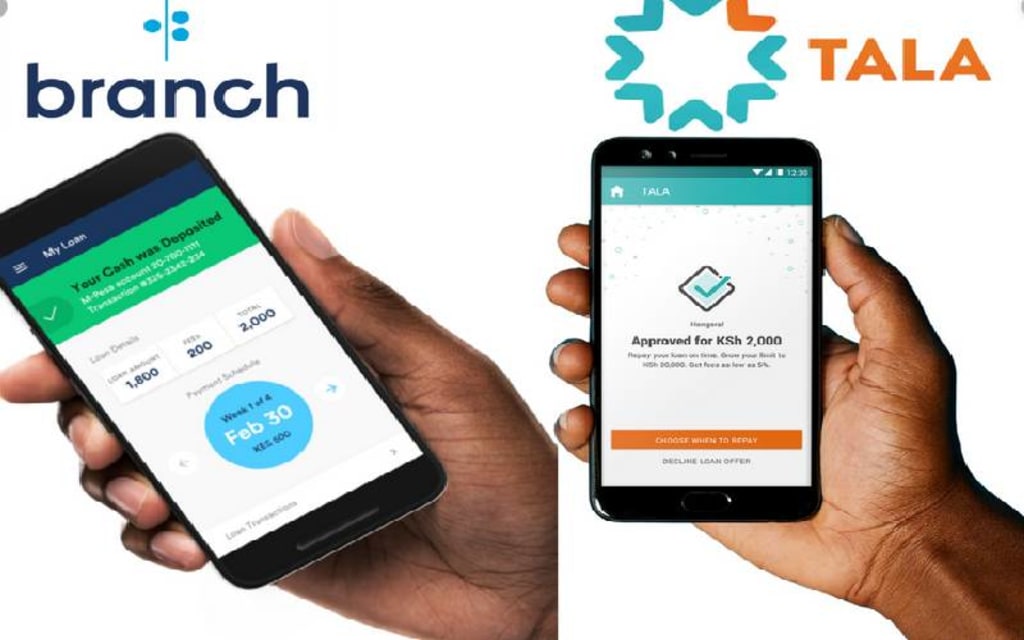

On the flip side, digital lending has grown to become debt traps for many borrowers who now find themselves stuck in a vicious cycle of debt. Many Kenyans under 35 years are struggling with huge Tala, Branch, M-Shwari, and O-Kash loans—name them! Today, there are over 50 digital lenders in Kenya, each one of them having free, easy-to-download apps on Google Play Store.

With that in mind, is the proliferation of digital loan apps a positive or negative trend? In my assessment, this trend is causing more harm than good in the country. Just to put things into a clearer perspective, this post highlights five catastrophic impacts that digital lending has precipitated in Kenya.

1. They are unreasonably expensive

Digital loan services have led many Kenyans into a debt spiral with their notoriously high interest fees.

Think of a lender such as Tala that charges borrowers a service fee of up to 19 percent. If you borrow KSh 10,000 from the platform today, you will have to pay back KSh 12,000 within one month. If you factor in the mobile money transfer charges, that figure fluctuates to about KSh. 12,200.

Take another lender such as O-Kash whose service fee is around 24 percent. If you borrow KSh 10,000, you will be paying back more than KSh 12,600 after 30 days. That’s without forgetting that defaulters are charged over and over, in which case they end up paying up to triple-digit interest rates.

Now consider this: Startup businesses across all industries in Kenya register around 6.5 percent to 10 percent return on investment per month. Simply put, if you borrow KSh 10,000 from Tala or any other digital lender and inject every coin into your small business today, you will most probably have made an extra KSh. 1000 after 30 days. On the other hand, the money will have accumulated more than KSh. 2,000 interest within that time. How do you close that KSh. 1,000 gap?

2. Chances of defaulting are higher than you think

This goes without saying, particularly considering the calculations above. It is almost impossible to repay a loan in one month—At least not when the interest rates are over 20 percent per month. Things get worse. Many borrowers take these loans for non-income generating purposes such as food, utility bills, rent, and entertainment. Poor financial planning, especially among the youths, doesn’t make things any better.

Now the question lingers: If you are borrowing because you cannot manage with your last month’s salary, what makes you confident that you will manage to repay the loan in full using this month’s salary and spare enough money for all your bills until next month’s salary comes? Remember that your income is almost constant and will hardly increase in a month.

In most cases, your options are two: You either repay the loan and borrow again, or delay in repayment time. If you had borrowed 10K, for example, you’ll repay 12K so that you can borrow again, in which case you will be approved for 10K. If you do this for a year, you will have lost over 24K in interest fees, and you will still be in a 10K+ debt. If you default, you risk being listed with the CRB.

There is a third option which is pretty unreasonable. This option is to borrow from another digital credit provider to pay your initial lender; say, borrow from M-Shwari to repay Branch. This will leave you in a huge refinancing crisis. There is a fourth option which is even more unreasonable: You can bet with the loan money, win, repay the loan, and save the balance. That is, of course, if you have comprehensive health insurance in place or if suffering a heart attack is the least of your concerns.

3. Most of them are unlicensed and unregulated

Dealing with an unlicensed and unregulated lender leaves you with little or no legal recourse in case of a financial dispute. 99 percent of digital lenders in Kenya, probably in the whole world, do not accept customer deposits, meaning that they aren’t subjected to the same licensing or lending regulations as mainstream banks and SACCOs. In that case, these lenders don’t give a hoot about debt collection laws and will use any orthodox or unorthodox procedures to recover their debt if you default. It is safe to think of them as digital shylocks.

4. Some are outright thieves

If you are into digital borrowing, then you must have come across at least one mobile loan app that required you to pay an upfront fee before they approved or processed your loan application. These lenders promise the world but will rarely honor their promises after you send them the required fee. There are better ones that will hold up their end of the bargain, but their approved loan amount will in most cases make little or no sense. I’ve seen people pay as much as KSh 500 advance fee only to be approved for KSh 1,000, with a service fee of 25 percent. In the end, they pay KSh. 800 for a KSh. 1000 loan. If that is not daytime robbery, tell me what is!

5. The risk of identity theft

Many borrowers are carried away by the prospects of getting quick loans to the point that they don’t even care about how much of their personal data they give away. Digital lenders tend to ask for your date of birth, next of kin, current and previous addresses, email address, ID number, level of education, etc. during your loan application process. This information is sufficient for a data thief masquerading as a digital lender to steal your identity and precipitate unimaginable trouble for you.

There are also loan apps that request you to turn on the location feature on your smartphone and give them access to your phonebook, messages, and social media apps. The intention here is to mine your data and use it to predict your social and economic standing and interactions. Actually, don’t be surprised when an unscrupulous digital lender calls your boss, parent or partner asking them to help you repay an overdue loan. Isn’t that embarrassing?

Note that even if the lender doesn’t intend to use your data unscrupulously, how sure can you be that they have the infrastructure to adequately protect your information against cyber criminals?

Parting shot

Borrowing from loan apps is unwise, both in terms of leaving your data vulnerable and jeopardizing your financial future. You should avoid them at all costs. If you must borrow from them, however, only borrow as much as you can afford to pay at once. Also, note that digital lenders will gladly increase your loan limit as a way of enticing you to borrow more, in which case you end up paying more interest fees. It is never a good idea to borrow the maximum.

About the Creator

Keep reading

More stories from Robert Gitau and writers in Trader and other communities.

Unpopular Opinion: 5 Reasons Why Manchester United Will Beat Liverpool

Troubled Manchester United plays their sworn arch-rivals, Liverpool, at Old Trafford on matchday 9. The Solskjaer camp will be looking to bounce back from their shock defeat at Newcastle a fortnight ago. Jurgen Klopp’s men, on the other hand, have had a perfect start to this campaign, collecting 24 points out of a possible 24 from their opening eight games. The odds are stuck against Ole and his men.

By Robert Gitau5 years ago in Cleats

THE GRAPHICS CARD WILL MEET ALL YOUR DEMANDS ON YOUR PC

In the dynamic realm of computing, few components command as much attention and admiration as the graphics card. These technological powerhouses, often referred to simply as GPUs (Graphics Processing Units), serve as the beating heart of visual processing in modern computers, enabling everything from immersive gaming experiences to complex visual simulations and professional content creation. Among the latest contenders in this arena stands the ASUS Dual GeForce RTX 4070 Super OC Edition Graphics Card, a formidable specimen boasting cutting-edge features and unrivaled performance.

By Kim Long Nguyệt Ngữ7 days ago in Trader

Comments

There are no comments for this story

Be the first to respond and start the conversation.