Cash is (Almost) Dead

The numbers are in and show that “Real American Dollars” are diminishing in importance in how we pay for things. And yes, you guessed it: Plastic is now the king of payments and digital cash is the future!

Dead")

Introduction

I must admit that I am a strategic management consultant and professor “of a certain age.” As such, I have to guard against falling into what might be academically called “old fart stories” and telling students/clients about the way things used to be - which, of course, plays no bearing whatsoever on the way things operate today and will in the future. Yes, those of us in our 50s, 60s, and 70s are the last generations that will really remember a marketplace where “cash was king.” We remember paying for items in stores with cash - or even a check. We can even remember writing out actual checks to mail to pay our bills (like in the days of the “Pony Express!”). Today, when the proverbial “little old lady” whips out her checkbook to write out a check to pay for her items at Walmart or Target, people behind her - or him - will often almost get enraged, thinking: “Why can’t she (or he) get with the program - and the times?”

Yes, it’s late 2023. And yes, the world has changed - a lot! Payments have changed, and no doubt, they have changed for the better! Today, we live in a world of “fast cash,” not cash itself! And for businesses and for their customers (yes, that would be all of us), there are far, far more benefits to living in a world where transactions are made as easy as the push of a button, the tap of a card, or even by “double tapping” the side of your phone. And while not everything always works smoothly, as when the reader can’t pick up the chip on your card or recognize your phone - or watch, payment technology is advancing…

very rapidly - and the new way of paying for, well everything, is going to be the way in due course!

And so in this article, we will look at the transformation of payments to a digital environment and away from paper, and look ahead as to what this will mean for all of us in the years to come! We will also see how cash - in a digital form, rather than the paper and coins we think of as “cash” will still play a large role in our lives - and our financial lives - going forward. And we will look “over the mountaintop” to see a future where consumers will love, rather than loathe, self-checkout!

The Rise of Plastic and Digital Cash

Each year now for a decade, the Federal Reserve Bank of Atlanta has conducted a survey of Americans to look at just how we are paying for things. Their Survey and Diary of Consumer Payment Choice has become the “go-to” guide for tracking how - and how much - Americans are making payments in their daily lives. As such, the economists there carry out a survey of Americans who record, in a diary, their spending habits and overall payment activities annually in the month of October. Their work, over time, tracks the evolution of the very fast-changing way in which Americans spend their money, specifically focusing on the modality, frequency, and amounts of those payments.

The recently released numbers from their 2022 survey (yeah folks, good analysis does take time!) show just how much we are integrating plastic and digital payments into our everyday lives - and de facto then - into our financial lives. The headline findings from their most recent survey of Americans’ spending habits show that in 2022:

- The average American reported making 39 total payments each month, a number unchanged from the previous year (2021).;

- American consumers - on average, mind you, made payments - in all forms - totaling over $5,000 dollars per month ($5,029 each and every month - yes, life is getting more and more expensive!).

- Roughly 9 in 10 Americans (87.2%) have at least one credit and/or debit card;

- 1 in 5 purchases (20%) were made remotely - largely online. This is double the amount of remote purchases made in 2019!;

- Approximately two-thirds of Americans (66%) had made at least one automatic payment from a checking or savings account at a bank.;

- Likewise, two-thirds of Americans reported that they had one or more online payment accounts, adopting services such as PayPal, Venmo, or Zelle.;

- Consumers are being offered options for BNPL (Buy Now, Pay Later) much more frequently, as half of all Americans reported this in 2022, as opposed to just a third of shoppers in 2021;

- Despite all the media coverage of these markets, only 1 in 10 Americans owned any form of cryptocurrency or crypto assets.;

And finally,

- Most of us still use cash - at least on occasion - to pay for things. In 2022, 83% of Americans reported making at least one cash transaction in the past month (down 2% from 2021).

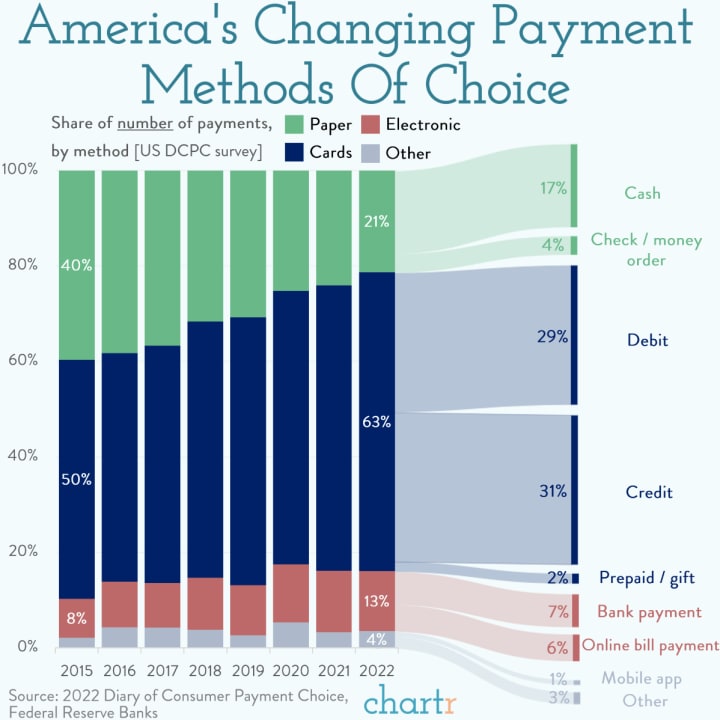

While the economists at the Federal Reserve Bank of Atlanta have put together a treasure trove of data and graphical resources available for anyone who might want to delve deeper into the ways that Americans pay for everything today, to me, there’s one graphic that is the attention grabber from all of their work. It was put together by the very good data journalists at Chartr. Their analysts took the Federal Reserve’s report on the ways in which we pay for things and boiled it down into one chart that spotlights the trends in payments we have seen over the last 8 years.

As you can see in Figure 1 (Share of the Number of Payments Made by Americans by Modality, 2015-2022), there are several major trends that have taken shape in recent years in terms of the number of payments (not the amount of payments - we’ll delve into that in a minute), including:

Figure 1: Share of the Number of Payments Made by Americans by Modality, 2015-2022

Source: Chartr, Cash Stuff, November 2023 (based on data from the 2022 Survey and Diary of Consumer Payment Choice, Federal Reserve Bank of Atlanta) - Used with permission.

- The use of cash has basically halved in less than a decade, falling from 40% of all transactions in 2015 to 21% in 2022. Last year, 17% of all payments were made using “Real American Currency” (paper bills and yes, coins), while checks were written for only 4% of all transactions.;

- The use of “plastic cash” (in the form of both credit and debit cards) has increased by a little over a quarter, rising from 50% in 2015 to 63% of all transactions - again by volume, not amount - in just eight years. And at present, debit card transactions (31% of ALL payments) outpace credit card payments (29%).;

- Online payments make up just over one in all transactions by volume. Thirteen percent of all money movements occur through either bank payments (7%) [think a mortgage, a car note, or yes, a credit card bill] or online bill payments (6%) of various types [think payments for utilities, rent, etc.]. However, these payments make up the vast majority of money being moved through our transactions by dollar volume.

- Despite all the attention being paid to Apple Pay and other forms of “pay by app” platforms, today, only 1% of all payments - again by volume - are paid by consumers using these apps. That should be of concern in Silicon Valley and beyond, as the “hype” for paying by an app on your phone or tablet has - to date at least - far exceeded the actual market penetration of these money apps.

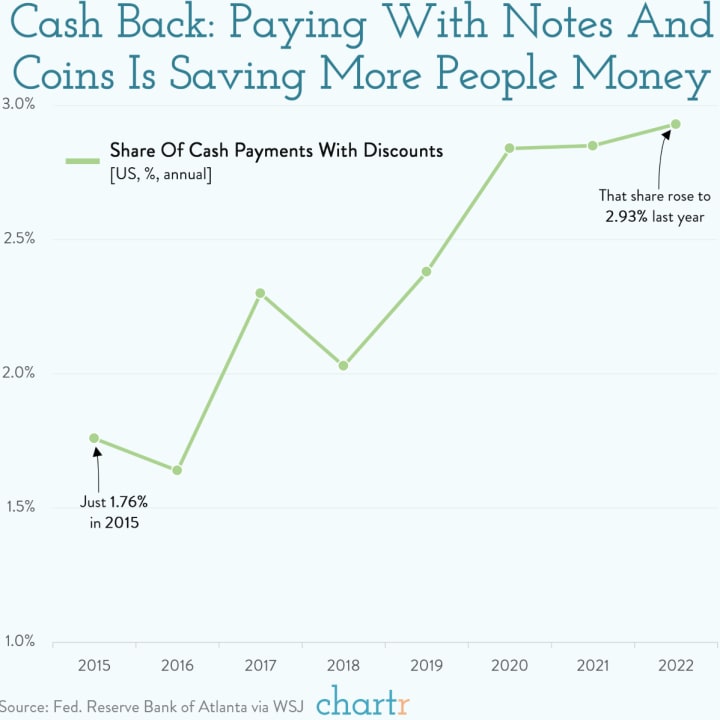

While there is much, much more to explore in the Federal Reserve Bank of Atlanta’s most recent payments survey, another interesting “nugget” is that cash is not dead - yet! In fact, both consumers and merchants alike are finding that cash-based transactions meet both their needs. Retailers, along with restaurants and many other service providers, in trying to avoid the typical 2-4% swipe fees associated with accepting credit card payments, are either offering cash payment discounts to their customers, or, absent that, enticing consumers to pay for a purchase/service in cash in order to avoid a “credit card surcharge” (which the Payments Journal, no less, deemed a “public nuisance!”) to be tacked onto their bill.

Figure 2: The Increasing Frequency of Discounts for Consumers When Paying with Cash, 2015-2022

Source: Chartr, Cash Stuff, November 2023 (based on data from the 2022 Survey and Diary of Consumer Payment Choice, Federal Reserve Bank of Atlanta) - Used with permission.

As you can see in Figure 2 (The Increasing Frequency of Discounts for Consumers When Paying with Cash, 2015-2022), the number of instances in which a cash-paying customer took advantage of such a “cash discount” rose by right at two-thirds (rising from 1.76% in frequency in 2015 to almost 3% (2.93%) of all cash-based transactions! Thus, it is clear that especially on sizeable transactions, where the swipe fees would amount to not pennies or dimes, but tens or even hundreds of dollars, cash discounts - or at least paying cash to avoid a swipe fee surcharge - is the real “growth market” for cash transactions on the retail level.

Analysis

As a strategic management professor and consultant, I think there is one main takeaway from all of this. This is the fact that the future of payments isn’t 3 or 5 years away, or even a decade ahead: The future of payments is here right now - and it’s indeed digital! We are fast transitioning from a cash-based economy to one based on digital cash. Whether the mode of transfer from buyer to seller or to service provider is buy plastic, by a prepaid card (used now in 2% of all transactions) or yes, by an app or online payment method - or even crypto, there will continue to be less of a need for cash in our lives and in our businesses with each passing year. When you free a business from cash - any retailer, any restaurant, any really consumer-facing business - then the enterprise frees itself from having to deal with cash, and management finds that it alleviates itself from a whole host of problems (i.e. physical cash management, banking, employee theft, customer counterfeit schemes and other fraud, etc.). This means millions - perhaps tens of millions of dollars in cost savings - and perhaps even more in preventable losses - for large companies. And for smaller retailers, restaurants, and even service providers, their cost savings, while, of course, on a much smaller scale, are just as, if not more, critical in their success equations than they are for their far larger counterparts - and competition!

Even more importantly, when you move away from handling cash - or at least significantly reduce the need for cash handling - in transactions, you create more and better opportunities to innovate in terms of the very critical consumer checkout/point-of-sale encounters. By having 80, 90, 95 or even 98% of transactions be digitally-based, rather than cash or check-based, you begin to open your business - whatever it may be - to innovations that can vastly improve the speed of - and customer satisfaction with - the “moment of truth” when payment is required. While there is great consumer backlash against today’s self-checkout technologies (basically, putting the onus on the customer to do all the work - and to do it right). In the past, I was one of the early “prophets” of RFID technology, and working still with companies today that are on the leading edge of retail technology today, I dare say that we are getting closer to the consumer dream of a “roll through” or simply “walk through” checkout in many retail environments, where what you bought and how you are paying for it are instantly reconciled in a truly “friction-free” checkout - a far, far cry from the laborious, often customer-angering “self” checkouts that we see today (that largely still require employee intervention and engagement to make the process “work”).

Finally, I think that the “last mile” problem in all of this - the one that prevents a straightforward march toward a better, cashless future, is the size of those swipe fees associated with accepting digital payments. The credit card processors, the digital payment platforms, and yes, even Apple, need to realize just how much of a drag - really, an obstacle - these typically 2-4% fees are for merchants and vendors, and how these fees are slowing innovation, not just in payments, but in the retail and restaurant industries in particular. We could move faster - much faster - in replacing today’s self-checkouts, which are, in truth, a bane of consumers and retailers alike with faster, better, and cheaper checkout technologies if the “ante” wasn’t so high on the part of the credit card processors in particular (I’m looking at you Visa, MasterCard, Discover, and American Express!).

The move toward “cash discounts” highlighted earlier is indeed a backlash against these charges. And yet, by encouraging - and facilitating - more digital payments, with lower swipe fees, the digital payment processors stand to make far more once the “science-fiction level” roll or walk-through checkouts - something that is only used in settings like Amazon’s small concept stores (Amazon Go and Amazon Fresh) today - becomes practical and commonplace. The real question is how fast, and how soon, will the credit card processors and other payment platforms respond to what is a fast-changing payments landscape - and where the pace of change will only accelerate - and yes, benefit them!

So, in the end, I do believe that we are indeed not that far away from that future where you are not the scanner, the bagger, and the payor, a future that all of us - including retailers, restaurants, and more - hope comes yesterday!

+++++++++++++++++++++++++++++++++++

About David Wyld

David Wyld is a Professor of Strategic Management at Southeastern Louisiana University in Hammond, Louisiana. He is a management consultant, researcher/writer, publisher, executive educator, and experienced expert witness. You can view all of his work at https://authory.com/DavidWyld. You can subscribe to his Medium article feed at: https://davidwyld.medium.com/subscribe.

Social Media Links to David Wyld:

on Facebook

on LinkedIn

on Twitter (X)

About the Creator

David Wyld

Professor, Consultant, Doer. Founder/Publisher of The IDEA Publishing (http://www.theideapublishing.com/) & Modern Business Press (http://www.modernbusinesspress.com)

Keep reading

More stories from David Wyld and writers in Trader and other communities.

There’s Only One Solution to Rising Gas Prices: Stay Home!

Overview There’s very real pain at the gas pump today! It seems like every time you go to fill-up your vehicle, the price of gas has gone up not just a few pennies or even a couple of nickels, but by several dimes - maybe even quarters depending on how much you drive and how big your car - and your gas tank - is! Now, more and more of us are seeing it take close to a hundred dollars - or even more if you live in California - to fill up your gas tank. And yes, gas prices have become the hot topic of conversation everywhere! And of course as we do in 2022, people are both taking out their frustrations - and showing their creativity - about the seemingly endless rise in gas prices, both on social media...

By David Wyld2 years ago in Trader

the best sofas on the market!

In the world of interior design, sofas occupy a central place, not only as functional furniture but also as essential decorative elements. They are the family gathering place, the symbol of comfort and conviviality in our living spaces. Today we witness the diversity and innovation in the world of sofas, with models that combine style, comfort and functionality in an exceptional way.Among the options available on the market, examples such as the "GrekPol Paris Corner sofa in corduroy fabric Poso with convertible function and storage space - Universal - Beige" offer an elegant combination of contemporary design and practicality, with a convertible function and integrated storage space, ideal for small spaces. Similarly, the "HOMCOM Sofa Convertible 3 Seater Scandinavian Design Tilt Adjustable Backrest 3 Levels Central Fold-Down Backrest 2 Glass Holders Solid Wood Linen Gray" seduces with its sleek Scandinavian design, adjustable backrest features and versatile character, adapted to different interior layouts. In addition, models such as the "SILAPE - Santi Convertible Corner Sofa - with Chest - in Leatherette and Fabric (Madryt 1100 + Berlin 01, Left Angle)" offer a modern and sophisticated aesthetic, combined with practical functionality thanks to its integrated storage space. These examples illustrate the diversity and innovation that characterize the sofa market today, while emphasizing the increasing importance given to the combination of comfort, style and functionality in the choice of furniture for our interiors. In this article, we will explore in more detail the different sofa options available, highlighting their distinctive features and benefits, in order to help consumers find the perfect sofa for their living space.

By Alicia Lhotellier4 days ago in Trader

Europeans reject Chinese cars.

China's car industry has changed over the course of the last ten years, from delivering fundamental western clones to making vehicles that equivalent the world's ideal. As the assembling force to be reckoned with of the world, China is likewise creating them in enormous volumes.

By Phumlani Mdlaloseabout 12 hours ago in Trader

Comments (2)

Interesting & informative!!!❤️❤️💕

Quite interesting, but one thing what about the chances of the Dark Web somehow obtaining all your information using plastic or cryptocurrency. I still think we should all know how to make change and even write a check for who knows when technology will go down someway.