Bankable Brilliance

Secrets to making banks cater to you, from a former financier, financial scam buster and bank product developer

You may have noticed that banks don't appear to be all that bright.

When I wrote an article on the most prevalent banking scam in history back in 2010, I was not surprised by the hundreds of attacks and dozens of threats that blasted back at me through the computer screen. After all, it had been perpetrated so successfully, governments had fallen for it, and so had banks, dating back to before the internet, when it was perpetrated by fax. Some consumer victims were so committed in their submission to that confidence game as to have stretched their participation, and hopes of payoff, across two generations. To call the bluff was to shatter the dream.

My 2010 article pre-dates the many which reiterate its assertions since I published it, including the warning distributed by the SEC. The FBI got so fed up with dealing with victims who claimed to be shocked to find they had been scammed when promised astronomical, impossible returns, that the Bureau began refusing to take the cases, and even told some victims that they got what they deserved.

What bank guarantee trading scams tell us

That scam evolved into a hybrid, able to take advantage of nearly every nuanced weakness society had to offer. Bankers who were queried to investigate its validity loved to speak in aloof, jargonized terms. Anxious to appear privileged and powerful, they were non-committal as to whether the concept itself was impossible. Scammers picked up the same lexicon to build confidence in victims. The Feds simply couldn't believe anyone could fall for this. But they did. In droves.

Of all the contributing factors to the longevity of the bank trading scam and its many cousins, one stands out. That is that vapid response from the banks themselves. Rather than take a firm stand and issue harsh warnings to keep customers away from the idea, they were limp in their reply, for years. It would be wise to take into consideration the fact that this scam involved tremendous bank deposits being tied up for years, a feature the banks don't mind so much. That's right - the banks are not without blame. It wouldn't be the only time we saw that phenomenon.

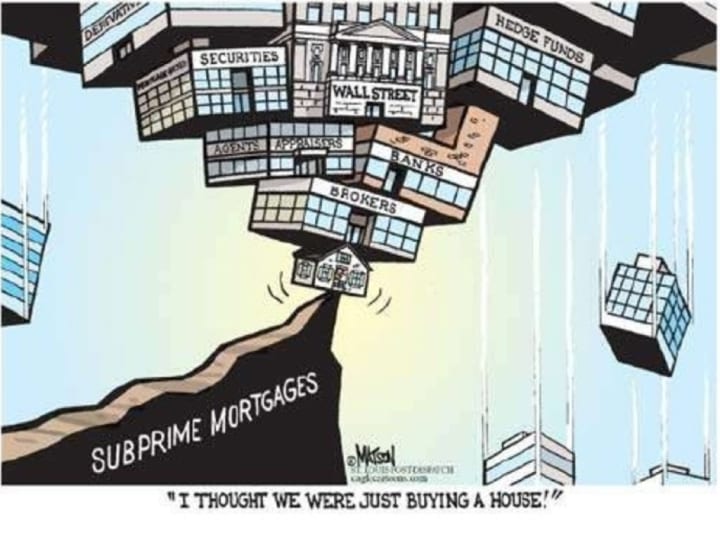

Don't forget the mortgage debacle

With the dismantling of fraudulent mortgage mills in 2009, we saw Wall Street banks deflect the blame for their own crazed lending practices, laying it at the feet of their own public face, their mortgage brokers, whom they pressured and rewarded to do the deals to begin with. That's also who wound up doing the time for them.

During the mortgage boom of the early 2000's, the wholesale lenders became the customer, courted by the mortgage broker. The borrower, who brought nothing to the transaction but the ability to fog a mirror, was fodder, lined up around the block to "buy" houses with no cash, no credit and no income. These people also suffered the blame from the banks.

But mortgage banks made a killing hanging the paper on Wall Street investors for a fat kickback, then acted like they had been hosed. It was a charade, as anyone who was there will tell you, off the record. In reality the banks had private insurance and the government to bail them out, but also sued the borrowers and brokers, in some cases collecting as many as four different negotiated payments on the same loan. Once again, it's hard to see where the banks were not willfully blind.

Lesson learned

Dealing with the banks in those tumultuous times laid bare the fact that it is always the lowest guys on the totem pole who are the first thrown under the bus, when the bank makes a mistake.

Blind faith in one's banker or financier has seen many customers tossed in the clink. You have to know how to protect yourself, and stick to transactions that make sense, even at times when the bank is more keen to be aggressive. A post-mortem on bank management in the US finds them fickle in offerings, flighty in markets, unreliable in product, vague and misguided in advertising. Yet there are certain tactics one can take which will always appeal to the financier of the day, while protecting you from having them make accusations against you, to cover their own missteps later.

There are many unwritten rules in the banking world, and many tricks of the trade unpublished. This is particularly the case when it comes to the task of making one's small business, or even one's self, "bankable."

The Rules of Bankability

"Bankability" is simply banking jargon for the status of being attractive to banks in three basic categories. Bankers love to refer to "the three C's" of bankability. Sometimes they'll want it to seem more advanced, so they'll add a few more C's to the list, which basically repeat the first three. Even within their own ranks, they can not agree on what each 'C' stands for. Let's remove their mystique, and interpret the jargon.

1. Character.

Here bank marketing teams hope to conjure up some Edwardian concept of honor and reputation. But don't grow that 1875 beard or go all gilded age just yet. In reality the 'character' C could simply stand for "credit." And the 'credit bro' who is likely to be evaluating your own credit profile probably can't spell "reputation."

True, banks used to assess much more about your length of time at your address, or on your job. But banks deal only with preferred borrowers now, and all preferred profiles have this information disclosed on their credit report, combined with their payment histories, all encapsulated into one tidy score, so that even some clown who can't spell "reputation" can make a loan decision.

Decipher the algorithmic tracking and you'll find it leads to consideration of only those payments reported by subscribers to the major credit databases, and only the facts about you reported by those subscribers. The creditors, the banks, the various other types of lenders and their employees show no indication that they either know nor care about your reputation. In fact, you may find many business people ranked as premier bank customers, sought after by large financial institutions in your community, who demonstrate a moral code on par with Hannibal Lecter. Meanwhile, I don't think Mother Teresa ever had lunch invitations from bankers.

Also, don't make the mistake of thinking that if you build credit and bankability in your company name, no one will worry about the fact that you perhaps have the personal credit of Charles Manson. If you get financing for your business with no personal guarantee to back it up, it will be in large part because you would qualify for that financing with a personal guarantee. If you would not personally qualify, then don't expect the offer of corporate-only financing without pledging your personal ability to repay.

2. Capacity

Here the banking community would have you believe they will magically ascertain your capacity for repayment, by some mystical comprehension of your earning ability, likelihood of continued employment, work ethic and job longevity, as if they are some kind of all-knowing employment and gig gurus, who would spend days hypothesizing about your career.

Oh, they'll talk about calculating your "uncommitted income" and other equations no one will actually consider until you are borrowing millions. Reality for the small business owner is that all of that is wrapped up in any preferred bank customer's credit score already, and that's what they use. If it is not in your score, don't expect them to delve further.

In truth, you will do better in evaluating your "capacity" if you ask yourself one question. It is what I have found to be the golden rule in bank loan underwriting, all over the world: Does the borrower need this financing? If the answer is yes, then they do not qualify. That may sound extreme, but it isn't. Banks are the top of the food chain in lending, and they can afford to lend only to those who do not need the funds. Your capacity to repay a loan must therefore be demonstrably of a caliber as to make it obvious, to a 4-year-old, that you do not need the requested financing. The lender has to believe completely that you could take it or leave it, and would have other means to do what you intend, should they decline. I have found it to be truly that simple. Kind of like dating - don't look desperate, don't look needy, show only mild interest.

3. Collateral

Collateral actually is not a consideration. Security is. The two words are synonyms, but the literal meaning of collateral would indicate that the security is of similar value to the loan. But, except for cash security, banks don't generally make a loan for which the security is only of even value to the loan amount. They much prefer to make the loan when the other conditions are met, and the value of any non-cash security and personal guarantee offered far exceed the loan amount.

Don't be fooled into thinking that an unsecured loan for which you are applying does not require that you have security. Bank underwriting guidelines tell the bank officer that you still need viable security available, you just may have credit strong enough so that you don't have to pledge it. Remember, you can't need the financing, or chances are it's not happening with a bank.

For all the push by banks to issue loans and especially credit cards, they keep their best under wraps. If a new or expanding small business knows how to position itself to be offered the solutions to the financing conundrum, expansion timelines can be collapsed by years. This is about preparation, about positioning your existing assets and abilities while planning specific, timed actions to to maximize bankability, and expedite your financing objectives.

Like any romance, one must make oneself presentable, desirable. One must manage the ongoing romance and assess the competition at each stage of the relationship. With banks, this means taking very specific steps, at specific institutions offering specific financial products, at specific times, to reach a certain status.

The Best Kept Secret

In 2002 I created a new bank product designed to allow customers to prove themselves to banks, relatively quickly. Unlike others, my product did this without borrowing to buy nonsense consumer items or inventory their small business didn't need, and without adverse affect on the customer's balance sheet. It took off like a shot, and is offered by hundreds of small and large banks and credit unions today.

But despite the widespread usage of the program I created, the bankers themselves seldom realize the underlying feature that is equal in importance to the obvious advantage points they tout. Also, nearly all of them keep it off the menu of offerings for standard customers. They keep it as part of an arsenal used to garner the customers they want to attract. You have to ask for it, and first you have to know how to ask for it. I'll be continuing this series to show you how to turn the tables, and attract the banks to you and yours.

If you'd prefer to finally be on the winning side of this game, subscribe now.

Next in this series:

Credit Building Mistakes: Popular advice that's bad for your bankability

About the Creator

Jonathan Warren

Honorary Consul of Monaco, Chairman of the Liberace Foundation for the Performing and Creative Arts, 50 years in Vegas, Citizen of the world.

www.jonathanwarren.me

Enjoyed the story? Support the Creator.

Subscribe for free to receive all their stories in your feed. You could also pledge your support or give them a one-off tip, letting them know you appreciate their work.

Keep reading

More stories from Jonathan Warren and writers in Trader and other communities.

Selfie Absorbed

Meg was a beautiful grad student, about a year older than me. We were laying on the floor of her dorm room at Columbia University. She rolled toward me and we kissed. With my free hand, I took a selfie at the perfect moment. The photo looked as if someone else snapped it.

By Jonathan Warrenabout a year ago in Wander

Better Semiconductor Stock: Nvidia or Advanced Micro Devices

The semiconductor business remains as a basic mainstay of present day innovation, controlling everything from cell phones to supercomputers. Inside this area, Nvidia (NVDA) and High level Miniature Gadgets (AMD) are two of the most conspicuous players, each with its own assets and vital core interests. Financial backers frequently end up conflicted between these two monsters while thinking about where to put down their wagers. This article dives into a similar investigation of Nvidia and AMD to figure out which may be the better semiconductor stock for your portfolio.

By Amol Deshmukh4 days ago in Trader

Comments

There are no comments for this story

Be the first to respond and start the conversation.