7 Things to Know About Fundrise

A great way to become a "landlord" without all the headaches

A middle-aged guy like me who has invested for more than two-and-a-half decades has been around the block a few times.

As such, I have invested and speculated on a very eclectic and wide-ranging variety of instruments over the past twenty-six years. Some of them did quite well, like the Wellington account that helped my late grandfather make me an extra fifty grand and not-quite that amount for my son a few years back to help put my children through college.

Some frittered away into nothing, or even worse, made me lose more than I had due to my stupidity of purchasing shares on margin - one of, if not the, biggest no-no there is.

So I am not new whatsoever to investing in REITs, or real estate investment trusts, for those of you unfamiliar with the term.

For wusses like me who do not have the capital, risk tolerance, or desire to manage an actual rental property, investing in REITs, and derivatives like mortgage trusts, are a far easier alternative.

For those of you who follow specific stocks, four that I can well recall having held for years included Armour Residential REIT (ARR), iShares Mortgage Real Estate Trust (REM), Annaly Capital Management (NLY), and what was among my favorites to trade about ten or fifteen years ago, New York Mortgage Trust (NYMT). I held a few others for shorter durations of time due to having them called away through covered call options that I sold.

Three reasons why I share the above — one is that I have been in the investing game for quite some time. Perhaps even before some readers were born. Prior to becoming an attorney, my younger brother was a real trader for two boutique trading firms in the Chicago financial district. What I mean by real is that he took a train downtown at an ungodly hour and made hundreds of trades per day, including in derivatives and derivatives of derivatives, using millions or tens of millions of other people’s money.

Complex time-sensitive futures spreads between competing currencies, international markets, commodities, and the like. Guys who make as much or more when the market tanks as when it goes up. Purely mathematical trading, including Ph. D-level “quants” from the University of Chicago. A few partners who owned multiple multi-million dollar homes and just as many personal problems.

Ultimately, the job was too stressful, and he decided to pursue a law degree. Around that time, he was making more every few weeks than I would make in a year as a probation officer and then as an entry-level economic developer.

But this is not about him.

I got it into my mind to grow some wealth as a not-quite-day-trader since I have worked full-time since 1993 but as a week- or month-trader while supporting my family on a fairly low government salary with a stay-at-home wife while also saving up as much as I possibly could for our children’s college funds for over fifteen years.

Thus, I speculated on many individual stocks and strove to create a balanced pool, including real estate investment trusts, mortgage trusts, pipeline limited partnerships, retail stocks, tech stocks, gold miners, and the like. I even purchased hundreds of shares in the volatility index and traded options on it.

It took me a solid seven or eight years to realize that I sucked at it and had done better overall by consistently investing in the same index funds that my late grandfather did. Over the years, I sold off individual stocks. Two were acquired, and I was forced into selling my shares, including one that I would have held my entire life if given the chance (Northern Tier Energy — NTI).

Another one that I had heard about through a friend went bankrupt and plummeted down to a big fat zero, causing me to lose several thousand dollars that I had put into it (Powerwave Technologies — PWAV).

My second point is that I now eschew wild speculative investments and generally prefer balanced index funds, a la the Boglehead philosophy of simply steadily investing for years despite the inevitable ups and downs of the market with the belief that the overall market will outperform stock pickers over the long run.

The third point is that I am constantly reading about fortunes built upon real estate investments and spend most of my days working with and assisting shopping center owners, industrial real estate brokers and developers, and investors in them, as well as a few businesses per day that I meet or speak with.

I have been a highly competent and hard-working economic development professional for over twenty-one years now and can personally attest to many vast fortunes, some in the hundreds of millions and perhaps a few over a billion, built by real estate developers and investors who I know personally.

Who would not want a piece of that?

So in my quest to put some lazy funds to work this year to get myself and my family a bit closer to financial independence, I read and read about Fundrise until I was ready to pull the trigger and get into it myself.

Before I detail seven things about my recently-minted account, I will make the disclaimer that I am by no means counting on this to be a slam-dunk winner. The funds may dwindle to zero, or they may double over the years that I intend to hold onto them.

It is just that when I ultimately write follow-up stories about how this investment has performed or the many ways that I generate additional revenue streams, this is the full disclosure that within the past several months, I have placed some funds with this company as many others have and now, once again, own a tiny little piece of the real estate pie here in the U.S. of A.

The following are seven things about opening a Fundrise account, including things that you will answer while doing so:

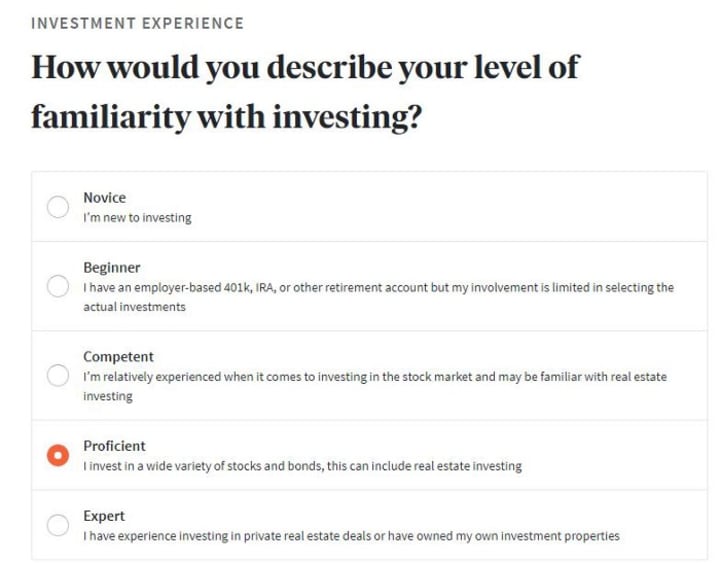

1. Are You a Proficient Investor?

TBH, I am likely somewhere between competent and proficient, but that choice did not exist. I have invested for over two-and-a-half decades, including in a wide variety of stocks, options, bonds, and index funds, and since I do have a fairly strong financial mind and have read many thousands of pages about it, I am at least competent.

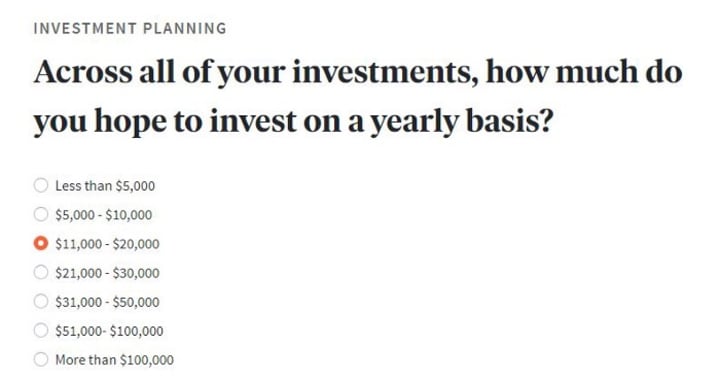

2. How Much Will You Invest This Year?

This year, I will have invested over $20,000, paying ourselves the equivalent of about $56 per day on average. Much of that included funds moved into this new investment.

I currently pay myself over $1,000 and mail a $500 check to Vanguard every month for my wife’s IRA.

I always Pay Ourselves First, and accomplished my simple goal for the year to invest more than the $44.40 per day that I paid ourselves in 2020. I exceeded that by a decent amount in 2021 and my goal for 2022 is to pay ourselves at least $50 per day, or $18,250 for the year.

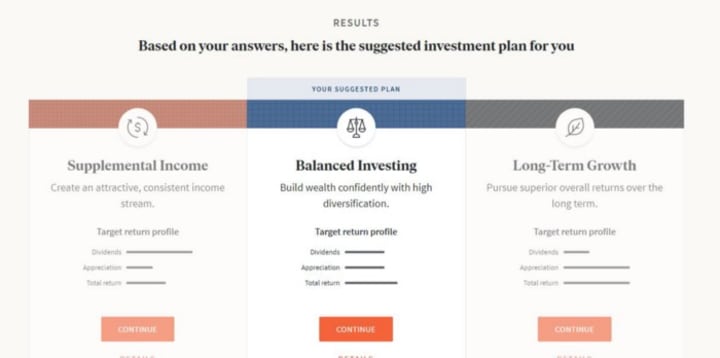

3. A Balanced Guy

I am no spring chicken and do not intend to keep money in Fundrise for ten or more years, although I just might. You never know.

So I am not necessarily seeking very long-term growth, like a thirty-year-old might while purchasing a duplex or a building to rent out long-term. Nor am I simply seeking a few hundred bucks here and there to supplement my income.

I am seeking a mix of dividends and income over the next six to seven years, which Fundrise suggested for me based upon factors like my age, risk tolerance, investing knowledge, and goals.

4. A Five-Year Plan

By its very nature, Fundrise is intended for investors with a time horizon of at least five years.

Per its website:

Can I redeem (cash out) my shares?

Real estate is inherently a long-term, illiquid investment. Fundrise is intended for investors who have a minimum time horizon of approximately five years. However, we have adopted a redemption plan whereby an investor may obtain liquidity quarterly for the eREITs and Interval Fund, or monthly after a minimum 60-day waiting period for the eFunds, subject to certain limitations.

I find this perfectly reasonable, as anyone should. The underlying assets held are in real estate; thus, the funds invested by people like you and me are put towards the purchase and ownership of tangible assets that cannot simply be liquidated in an instant on the equities market.

Since it is my overall goal to put the proceeds from this into use sometime in late 2026 to early 2027, I had originally clicked on my honest answer of a five-year time horizon.

When I originally checked “3–5 years,” Fundrise suggested that I become a “Basic” investor and get started with a simple real estate portfolio.

So I went back and checked off the “6–10 years” category instead and was moved up to a “Core” account level which requires an initial investment of at least five thousand dollars.

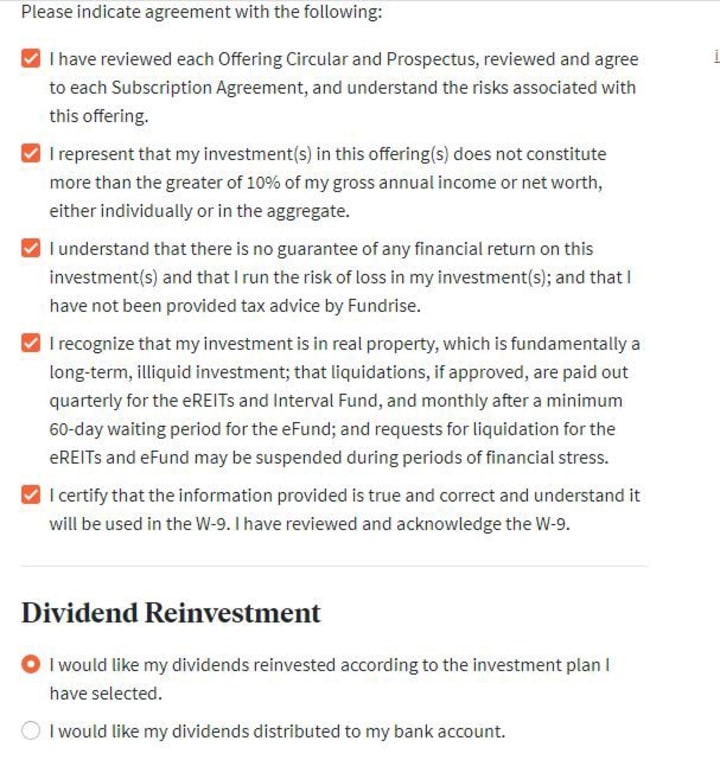

5. The Kind of DRIP You Want to Have

With every single investment that I have ever made, with one exception (NLY), I have always reinvested every dollar received in dividends and capital gains into purchasing additional shares. That is typically known as a DRIP or dividend reinvestment program.

It is not only something that you should do. It is something that you must do in order to attain long-term sustainable wealth.

I did not really read the thousands of pages of offerings but will reinvest dividends.

I suppose that if you already have millions in investments and are at the point of maintaining the capital while living off of the interest, a case could be made for having the dividends distributed to your bank account.

Who knows? I may just go all-in with this over the years and become one of those folks, myself, ten or so years from now.

6. A Humble Goal

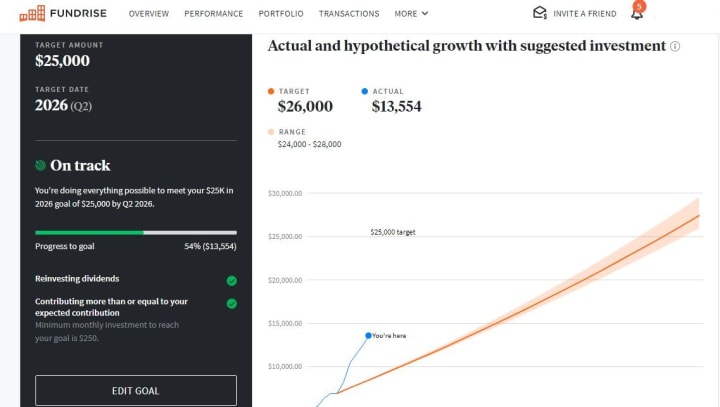

One of the things that I like about Fundrise is that it urges you to set a goal and then lets you know how much you should continue investing in an effort to reach it.

My humble goal is to reach twenty-five grand in five years.

By no means is this going to become my primary investment. My main focus continues to be funding my Roth IRA to the maximum amount every year and also investing on my wife’s behalf plus three to five thousand more in a variety of other accounts.

Once I do max out my IRA at $7,000 in July, I plan on investing no less than five thousand more with Fundrise next year in my effort to reach at least the twenty-five thousand mark or higher five years from now.

I may very well dramatically increase my investment in it or may just invest twenty thousand total into it over these three year and forget about it.

Either way, my family and I will most definitely have a need for these funds five or more years from now, just as we do now and anyone would.

I do like that it helps you set a goal, though.

7. A Real Estate Investor Once Again

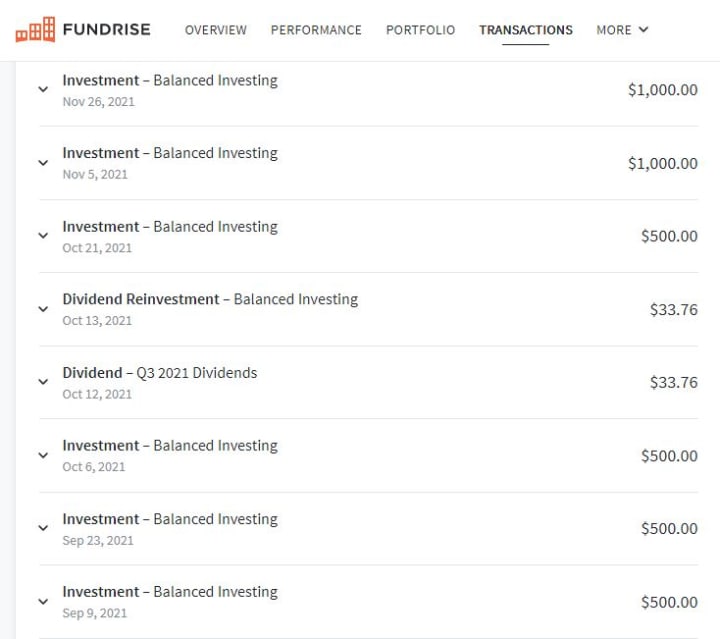

After completing all the questions, linking our checking account, answering numerous security questions, and setting my 25K goal, I saw that the original investment of $5,000 transferred a few days later, and then I continued investing a few hundred here and a thousand there throughout the past few months. I am now a small, nearly microscopic, part of the real estate game once again.

I receive numerous emails from Fundrise about purchases and sales made by my portfolio and now am a real estate investor once again. I have not viewed all “my projects,” although I probably should.

Instead, I will continue logging into my account and making investments in it throughout 2022 and 2023, with the hope and expectation that the rental real estate market in which my portfolio invests will remain solid for the coming years. I realize that continued success with this platform is not guaranteed, but I am fairly comfortable with it for the time being.

Finally, I share the above for a few reasons, one being that some people write posts or stories about successful investments after they have had them for years. I am sharing an investment that I feel good enough about to put some money where my mouth is and recall that it probably took me the better part of a year to save up the initial five grand that I started the account with in addition to saving more than that for each of our children's college funds.

Furthermore, as a builder of long-term wealth, it is imperative to build multiple income streams, and so far this appears to be a good candidate to become a solid one for years to come.

As I will soon share, I am amending my “retirement” goal from FatFIRE 55 to Barista Fire at 56 or 57, and I hope that this particular investment will help offset some costs for my wife and me for a few years in our late fifties.

What I hope to share in the coming years is how well this investment performed and how much I sent to it, etc.

Do I know what these rising funds will go toward in 2026, 2027, or beyond?

A worldwide vacation tour? A payment toward a self-driving Tesla? A down payment on a motor home? Medications to keep someone alive? A robot worker to do our bidding? A synthetic right ankle for me? Down-payment assistance for one of our children? Wedding costs for one of them?

Only God knows.

About the Creator

M. Bernard Bloom

I'm a middle-aged, middle-class family man and long-time economic development professional residing in the northwest suburbs of Chicago. Aspiring writer and NFT artist with interest in personal finance, self-improvement, and digital art.

Keep reading

More stories from M. Bernard Bloom and writers in Trader and other communities.

The 7 Ways We Paid Ourselves $56.30 Per Day

Before I launch into the seven ways how I should issue two disclaimers: First, it can all be boiled down to one way, which is to just do it. However you pay yourself or “yourselves,” or as I like to refer to it, “ourselves” since it also includes my wife, you simply need to do like the Nike ad says — Just Do It.

By M. Bernard Bloom2 years ago in Trader

"Stride in Style: Discover the ALDO Men's Albeck Oxford"

In the realm of men's footwear, finding the perfect balance between style, comfort, and versatility can often feel like an elusive quest. Yet, amidst the sea of options, there emerges a beacon of excellence that embodies these qualities seamless: the ALDO Men's Albeck Oxford. As a distinguished member of ALDO's esteemed lineup, the Albeck Oxford stands as a testament to the brand's commitment to crafting footwear that not only exudes sophistication but also delivers unparalleled comfort and durability.

By Kim Long Nguyệt Ngữ5 days ago in Trader

2023 Fashion Designer Shoes Men Casual Platform Sneakes Lace Up Trainers Student Sneakes Mens Vulcanized Shoes Zapatillas Hombre

In the ever-evolving world of fashion, footwear has become more than just a functional accessory; it's a statement of style, personality, and individuality. One of the most intriguing trends to emerge in recent years is the fusion of casual comfort with elevated design, epitomized by the rise of platform sneakers for men. These shoes seamlessly blend streetwear flair with high-fashion sensibilities, creating a versatile option that can effortlessly transition from day to night, casual to formal.

By Wedson Vegas3 days ago in Trader

Comments

There are no comments for this story

Be the first to respond and start the conversation.