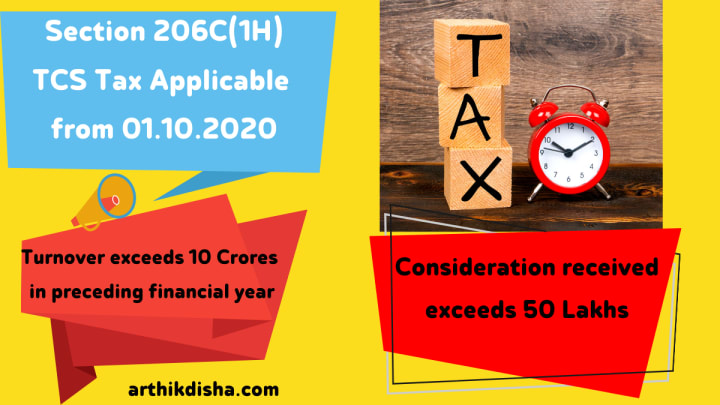

What Is TCS Tax-Tax Collected At Source-Section 206C(1H)

TCS on Sale of Goods applicable from 01.10.2020

What Is TCS Tax or Tax Collected at Source

Full form of TCS Tax is Tax Collected at Source. By this time you might have already known this. The Govt. of India vide Finance Act 2020, has introduced two new provisions of Tax Collected at Source effective from 01.10.2020.

Tax Collected at Source or TCS Tax is not a new concept. As of now, TCS Tax is applicable on certain transactions involving prescribed goods and services both under Income Tax and GST regime.

Now, the new provision of Tax Collected at Source/TCS applicable w.e.f 01.10.2020 vide Section 206C(1H) of the Income Tax Act as passed by the Finance Act 2020 incorporating all the remaining goods under the ambit of TCS Tax.

New Provision of Finance Act 2020 is TCS Tax Collected at Source or TCS on Sale of Goods Under Section 206C(1H) of the Income Tax Act, which is basically a form of advance income-tax not an additional tax burden.

TCS Tax Collected at Source/TCS on Sale of Goods Under Section 206C(1H) w.e.f 01.10.2020 .

As per Section 206C(1H) of the Income Tax Act 1961 :

Every person, being a seller, who receives any amount as consideration for the sale of any goods of the value or aggregate of such value exceeding ₹50 Lakh in any previous year, other than the goods being exported out of India,

or goods covered in Section 206C(1F) or Section 206C(1G) shall, at the time of receipt of such amount, collect from the buyer, a sum equal to 0.1 % of the sale consideration exceeding ₹50 Lakh as income-tax.

Also, Section 206C(1H) has set the minimum criteria for a seller to be eligible to collect TCS on sale of Goods if his turnover exceeds ₹10 Crore in the preceding financial year.

Therefore, it is very important to understand that not every seller is liable to collect and deposit TCS as per the provisions of Section 206C(1H). Both buyer and the seller has to fulfil some conditions as envisaged in this section.

What is TCS Tax w.e.f 01.10.2020?

Earlier Tax Collected at Source was applicable on certain goods but after the introduction of new Section 206C(1H), the remaining goods were included under this TCS system effective from 01.10.2020.

Therefore, TCS Tax is nothing new but the collection of Tax at source by the seller while selling goods to the buyer only if the following conditions are satisfied. So, this is an advance income-tax the Govt. is trying to collect.

- A Seller of Goods is liable to collect TCS from the Buyer on the selling of any goods to him;

- TCS should be collected only when the Turnover of the Seller exceeds ₹10 Crore in the preceding financial year;

- TCS is to be collected if the aggregate value of sales consideration to be received for Goods from the buyer exceeds ₹ 50 Lakhs in a financial year;

- TCS Tax will be applicable on the consideration receipts on or after 01.10.2020;

- So, TCS Tax will be collected on Sales Value minus ₹ 50 Lakhs;

- Rates of TCS: TCS Tax is collected @ 0.1% (0.075% till 31.03.2021) when PAN of the buyer is available;

- TCS Tax will be charged @1% if PAN of the buyer is not available.

Who is a ‘Buyer’ under the provisions of section 206C(1H)?

As per Section 206C(1H) of the Income Tax Act on TCS on Sale of Goods, A Buyer means a person who buys any goods but does not include the following:

- The Central Government, a State Government, an Embassy, a High Commission, Legation, Commission, Consulate and the Tade representation of a Foreign State; or

- A Local Authority as defined in the Explanation to clause (20) of Section 10; or

- A person importing goods into India or any other person as the Central Government may, by notification in the Official Gazette, specify for this purpose, subject to such conditions as may be specified therein;

Who is a ‘Seller’ under the provisions of section 206C(1H)?

As per Section 206C(1H) of the Income Tax Act on TCS on Sale of Goods, A Seller” means a person whose total sales, gross receipts or turnover from the business carried on by him exceeds ₹10 Crore during the financial year immediately preceding the financial year in which the sale of goods is carried out,

and not being a person as the Central Government may, by notification in the Official Gazette, specify for this purpose, subject to such conditions as may be specified therein.

Is the TCS on Sale of Goods to be collected on the TCS Tax Component?

Yes, TCS Tax is to be collected on the basis of actual receipt pertaining to the sales consideration. I mean any other tax component such as GST is included and not to be deducted while calculating the value on which TCS needs to be levied.

So, in a nutshell, TCS Tax will have to be collected on the sales value including GST. Even any discount, sales return not to be deducted from the sales value. The main component is the actual value received or to be received from the buyer.

On what amount TCS on Sale of Goods to be collected U/S Section 206C(1H)?

As per Section 206C(1H), as enacted for TCS on Sale of Goods, TCS will have to be collected by the Seller @0.10%(0.075% till 31st March 2021) on the receipt of sales consideration in excess of ₹ 50 Lakhs from the buyer in a financial year with effect from 1st October 2020 only.

So, TCS Tax Collected at Source on Sale of Goods will be levied in the following manner.

TCS= (Receipt of Sales Consideration – ₹ 50 Lakhs) X 0.10%

Example: 1 – Sales consideration is below ₹ 50 Lakhs up to 30.09.2020

a. Sales made up to 30.09.2020 ₹ 45 Lakhs

b. Consideration received up to 30-09-2020 ₹ 40 Lakhs

c. Further sales made after 01.10.2020 ₹ 36 Lakhs

d. Consideration received after 01.10.2020 ₹ 32 Lakhs

e. On what amount TCS will be charged ????

Solution: TCS on Sale of Goods is calculated on the actual amount received on or after 1st October 2020 only exceeding ₹ 50 Lakhs.

Therefore, the following points are important here:

Total Sales during the year 2020-21(a+c) – ₹ 81 Lakhs

Total consideration received during the year 2020-21(b+d) – ₹ 72 Lakhs

Consideration received after 1st October 2020(d) – ₹ 32 Lakhs

Maximum threshold limit for the F.Y 2020-21 – ₹ 50 Lakhs

So, TCS amount is (72 Lakhs-50 Lakhs)*0.075%= ₹ 1650.TCS is applicable only on ₹ 22 Lakhs and not on ₹ 32 Lakhs.

TCS is not applicable on the consideration received up to 30.09.2020.

Therefore, TCS is chargeable on ₹ 22 Lakhs only i.e. consideration received after 1st October 2020 exceeding ₹50 Lakhs and not on the entire ₹32 Lakhs.

Whether sales consideration received prior to 01.10.2020 would be considered while calculating TCS amount?

CBDT has clearly mentioned in their Guidance clarification note that TCS shall be applicable on the amount received on or after 1st October 2020 only. Therefore, there is no question of collecting TCS on the amount received prior to 1st October 2020.

But this should be kept in mind that the maximum exemption limit of ₹ 50 Lakhs is allowed in a financial year only. Once you exceed the threshold limit of ₹ 50 Lakhs, TCS is chargeable instantly on any amount received on or after 1st October. But no TCS even if you received ₹ 60 Lakhs up to 30th September.

If the sales consideration exceeds ₹ 50 Lakhs before 1st October, it needs to be taken into consideration while calculating the threshold limit from 1st April 2020.

Accordingly, the amount received on or after 1st October exceeding ₹ 50 Lakhs will have to be taken into consideration for TCS calculation.

No TCS on the sales consideration received up to ₹50 Lakhs whether sales made prior to 30th September or on or after 1st October as it is the maximum threshold limit. The threshold limit is calculated from 1st April.

Example: 2- Sales made more than ₹ 50 Lakhs up to 30.09.2020

a. Sales made up to 30-09-2020 ₹ 60 Lakhs

b. Consideration received up to 30-09-2020 ₹ 45 Lakhs

c. Further sales made after 01.10.2020 ₹ 20 Lakhs

d. Consideration received after 01.10.2020 ₹ 31 Lakhs

e. On what amount TCS will be charged ????

Solution: TCS on sale of Goods is calculated on the actual amount received on or after 1st October 2020 only exceeding ₹ 50 Lakhs. TCS is not applicable on the consideration received up to 30.09.2020.

Therefore, the following points are important here:

Total Sales during the year 2020-21(a+c) – ₹ 80 Lakhs

Total consideration received during the year 2020-21(b+d) – ₹ 76 Lakhs

Consideration received after 1st October 2020 (d) – ₹ 31 Lakhs

Maximum threshold limit for the F.Y 2020-21 – ₹ 50 Lakhs

So, TCS amount is (76 Lakhs-50 Lakhs)*0.075%= ₹ 1950. TCS is applicable only on ₹ 26 Lakhs and not on ₹ 31 Lakhs.

Therefore, out of the ₹ 31 Lakhs received after 01.10.2020, TCS is chargeable only on ₹ 26 Lakhs only i.e. consideration received after 1st October 2020 exceeding ₹50 Lakhs and not on the entire ₹31 Lakhs.

Example: 3-Consideration received more than ₹ 50 Lakh up to 30.09.2020

a. Sales made up to 30-09-2020 ₹ 70 Lakhs

b. Consideration received up to 30-09-2020 ₹ 59 Lakhs

c. Further sales made after 01.10.2020 ₹ 24 Lakhs

d. Consideration received after 01.10.2020 ₹ 33 Lakhs

e. On what amount TCS will be charged ????

Solution: TCS on Sale of Goods is calculated on the actual amount received on or after 1st October 2020 only exceeding ₹ 50 Lakhs.TCS is not applicable on the consideration received up to 30.09.2020.

But in the instant case threshold limit was crossed prior to 01.10.2020. So any consideration received on or after 01.10.2020 is liable to Tax collected at source.

Therefore, the following points are important here:

Total Sales during the year 2020-21(a+c) – ₹ 94 Lakhs

Total consideration received during the year 2020-21(b+d) – ₹ 92 Lakhs

Consideration received after 1st October 2020 (d) – ₹ 33 Lakhs

Maximum threshold limit after 1st October 2020 – ₹ NIL

So, TCS amount is (33 Lakhs *0.075%)= ₹ 2475. TCS is applicable only on ₹ 33 Lakhs and not on ₹ 42 Lakhs(i.e. 92 L-50 L).

Therefore, as per section 206C(1H) out of the ₹ 33 Lakhs received after 01.10.2020, TCS Tax is chargeable only on ₹ 33 Lakhs i.e. consideration received after 1st October 2020 exceeding ₹50 Lakhs and not on the entire ₹42 Lakhs.

Are the limit of ₹10 Crores and ₹ 50 Lakhs applicable on TCS on Sale of Goods or Services?

As per the provisions of Section 206C(1H) on TCS on Sale of Goods, as the name itself suggests that TCS is applicable only to the sale of goods and not on the sale of services for calculating the maximum threshold limit of ₹ 50 Lakhs.

Similarly while calculating the threshold limit of ₹ 10 Crores in the preceding financial year, Section 206C(1H) states that the total sale consideration and gross receipts from the business are to be considered. So, it will consist of both the sale of goods and services as well.

Is TCS on Sale of Goods applicable on the export of Goods?

No TCS on Sale of Goods is not applicable to the goods exported outside India.

Is TCS Tax applicable on the Packing, Forwarding and Insurance amount?

Section 206C(1H) basically deals with the TCS on sale of Goods. Therefore, if packing, forwarding and Insurance form part of the sale consideration, it will definitely be considered for TCS Tax calculation.

Is TCS Tax applicable to the advance amount received from the buyer?

Yes. Section 206C(1H) clearly states that TCS on Sale of Goods is to be charged on the consideration received from the buyer whether as advance amount where goods will be supplied at a later date. But the threshold limit of ₹ 50 Lakhs shall have to be taken into consideration while charging TCS Tax on the advance amount.

Will the seller get a credit of the TCS Tax Collected at Source during the financial year?

The CBDT vide its guidance note mentioned that TCS on Sale of goods is not an additional tax. It is nothing but a form of advance tax cum TDS. Which the seller would get a credit of the taxes so paid while filing ITR in the next financial year.

So, TCS Tax as per Section 206C(1H) is basically an advance income tax and no additional burden on the seller which is subject to a tax credit next year.

About the Creator

Arthik Disha

A Personal Finance Blogger. Passionate about finance.

Keep reading

More stories from Arthik Disha and writers in The Swamp and other communities.

International Monetary Fund-Objectives & Functions

International Monetary Fund-How Does It Work? Many occasions we read in Newspapers or in different journals regarding the International Monetary Fund. IMF has done this, IMF has done that and many more. But many of us don’t know Who actually IMF is and what does it actually do.

By Arthik Disha4 years ago in The Swamp

THE HARDER THEY FALL

MAYORS COME AND GO especially when burdened with an era of dilema from a prior administration. That is not to say thatcarrying off a resolution of any prior political height is not accomplishable by an incoming entity; but it reads like an open book, specific to women of color.

By CarmenJimersonCross-Safieddinea day ago in The Swamp

Comments

There are no comments for this story

Be the first to respond and start the conversation.