A short story:

I started investing on the Romanian stock market in 2005, a year in which I almost doubled my money, without any kind of investment strategy.

We knew all the peculiarities of the listed companies, we knew everything about company management, dividends, charts, financial news. It took me a long time but I liked what I was doing.

The next 2 years, 2006–2007 were again very good but the year 2008 brought me a loss of 70–80% of the total portfolio.

I spent the next 3–4 years trying to make up for the loss, and I ended up in 2011–2012 when the sovereign debt crisis (when Greece was close to bankruptcy) brought me losses again.

2013–2014 were years in which I spent much less on the stock market and with much smaller amounts because I felt that I did not understand anything of this whole phenomenon. I felt that I was consuming a lot of time and resources and the results were far below expectations.

The results were much worse than if I had invested an initial amount in 2005 and stayed on the bar all this time. No stress, no wasted time but with much higher gains.

It wasn’t until 2014–2015 that I started investing passively, systematically, without adrenaline and dopamine to darken my judgment, just like a professional.

And the results were much better, managing to get a consistent over 10% annual return on the total portfolio, without allocating more than 30% of the portfolio on shares.

Below, I will describe the 5 steps that any investor should go through in establishing an investment strategy.

To better explain the strategy, I will also provide an ultra simplified example.

Stock market investment strategy:

1.Self-knowledge

- What do I want in the long run? Financial independence: 2000 USD passive income per month.

- How long? 15 years

- What are the intermediate terminals I need to touch? $ 500 per month, $ 1000 per month,

- How much time am I willing to spend on investments? 2–3 hours a week

- Risk profile — how do I feel and behave when I feel a certain volatility / loss? Moderate — can withstand a temporary loss of up to 20–25% of the portfolio

- What are my favorite tools that I trust the most? Shares and bonds

- Do investments in securities or real estate suit me, or both? Investments in furniture because they are more comfortable and I like to keep my nose in my laptop more than managing tenants.

2. Understand the tool you are investing in

Whether we are talking about stocks, stock ETFs, bond ETFs, individual bonds or other more complex instruments, in order to be successful in investing you need to understand the financial instrument very well:

- what it represents at a concrete level;

- how to create added value for the investor;

- when he pays the dividend, the coupon;

- operating rules;

- what are the associated risks etc.

Let’s say we want to invest in stocks and bonds. In this case, we LEARN about actions and obligations until it is very clear to us what they represent: economic, legal, technical, psychological, metaphysical and so on.

The idea is that we need to understand the tool we are investing in. It’s our money at stake.

After learning what stocks and bonds mean, let’s say we selected two ETFs to invest in:

An ETF that replicates the S & P500 — US stocks

An ETF on Barclays Capital U.S. Aggregate Bond Index — on bonds listed in the USA.

3. To know the history of the investment

- What returns has that investment made in the past?

- what was the maximum volatility,

- how it performs according to economic growth, inflation and technological evolution and other specific factors that influence it.

What were the historical yields and maximum volatility for the period 1987–2019:

The average annualized return for the last 32 years for the S & P500 was around 10% and that of Barclays Agregated Bonds — around 5.9% in USD.

Of course, in order to calculate exactly, we should find tools that replicate these indexes and look at their concrete history.

4. Risk management

Don’t lose any money (long term).

- This means diversifying assets; Through the two index funds, we have already diversified into the top 500 US stocks and several hundred US bond issues.

- asset allocation in certain proportions, complementary financial instruments (when one performs better the other performs poorly and vice versa); Historical government stocks and bonds supplement each other — when stocks fall it is likely (but not certain) that bonds will rise.

- clear distinction between money for investment and money for other purposes; I do not intend to take my house, car, vacation or other things with this money but to invest them for at least 15 years + I already have an emergency fund put in a safe place.

- running a simulation of the most unfavorable scenario and of the optimal solutions in case that scenario materializes.

Let’s see what would have happened if we had an allocation of 50% on shares and 50% on bonds:

At such an allocation we notice that we would have had a compound annual increase of 8.47% and in the worst year of the whole period we would have had a decrease of only 16%.

Hmmm not bad, especially since we’re talking about yields in USD.

The maximum loss was in 2008 (obviously) — somewhere at 16% — which is below our risk tolerance calculated at point 1 of 20–25%.

Also, the maximum drawdown, the maximum decrease on a certain day, was -25%, which is within my maximum volatility tolerance.

So, good to go.

5.To be constant

- Constant savings; Let’s say I save $ 1,000 a month

- Fixed monthly / quarterly payments, or variable monthly payments depending on the evolution of the market (a slightly more advanced strategy); I invest $ 1000 a month in the SP500 and the next month $ 1,000 in the Barclays index, or $ 500 a month in each.

- Confidence in strategy regardless of current variations; 30-year history does not necessarily have to be repeated, but usually history repeats itself.

- Constant reinvestment of profit;

- Knowledge and integration of the notion of compound interest.

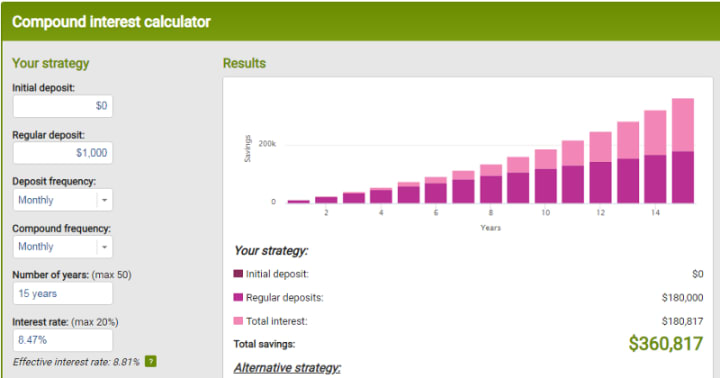

- And speaking of compound interest, let’s see what happens if we invest $ 1,000 a month for 15 years at a rate of 8.47%?

After 15 years we have about 360,000 USD portfolio. At an average yield of 8.47%, this portfolio will produce a profit of USD 30,000 per year, ie approximately USD 2,500 gross per month. After lowering your taxes, you will probably reach $ 2000 net per month. Wasn’t that our goal from point 1?

Conclusions

Without making investment recommendations (and this material is not an investment recommendation), I wonder if you think you could replicate this strategy?

I’m not talking about strategy, not the $ 1,000 a month. The strategy can be adapted and optimized depending on the amounts.

How long would it take you per month?

How much time do you save?

How many years of work do you save?

How many years of your life would you earn?

And this is just an ultra-simplified strategy focused only on the largest and (theoretically) safest market on earth: the USA. There are other stock markets, not just the US, there are other types of bonds, not just US government bonds and highly rated US bonds (those in the Barclays bond index) — other instruments that bring higher returns (and slightly higher risks). big).

The tools presented are for illustrative purposes only.

Above you have seen how to formulate a professional investment strategy but adapted to the level of an individual investor.

Why stay with money in deposits or worse to spend it in vain when we can actually “buy” our freedom?

When is the best time to start investing? Yesterday The second best time is TODAY.

About the Creator

A Glimpse of Light Before the Darkness

Amidst the heavy fog that rolled across the coastal town of Dunsmuir, Eleanor Bennett trudged home through the winding, cobblestone streets. The lanterns lining the path flickered as the evening breeze played with their flames. Eleanor, a young woman of twenty-five, was returning from her shift at the local apothecary. Her heart was heavy with the day's encounters—a child stricken with fever, an elderly man battling rheumatism, and whispers of a shadow looming over the town.

By RAVI KUMARabout 7 hours ago in Journal

Comments

There are no comments for this story

Be the first to respond and start the conversation.