Why the Housing Market is Going to Be the Demise of Our Generation

The economy is only thriving if you’re rich…

Poverty rates are at an all time low. The housing market is booming. The economy is thriving, right?

Wrong.

I think we all know that the COVID-19 Pandemic has taken its toll on the economy. An unreasonable amount of people have lost their jobs and been affected financially by this global outbreak. However, even if we disregard all of the economic turmoil caused by this virus, us young adults are still in a bad place when it comes to setting ourselves up for long term economic success.

First off, the economy…

If you were rich when Donald Trump took the presidency, back at the beginning of 2017, you’re probably really rich now.

The manner in which Trump has worked on the economy throughout his term has essentially profited only the higher class. Profits have skyrocketed for those that were already rich, making them even richer. Meanwhile, lower to middle class citizens, the category where almost all young adults fall, have been stuck with nearly the exact same wages, while costs of everything around us has spiked.

This same phenomenon has applied to the housing market. If you already own a house, you are probably in a really good financial spot, in a general sense. The housing market is absolutely booming. There are way more people that need houses than there are actual houses and demand just can’t keep up.

Because of this, property values are skyrocketing. If you’re a homeowner in the United States, chances are the value of your property is multiplying week by week. This doesn’t go to say that you’re rich, by any means, or that you may not struggle to balance all of your finances, but it almost certainly does mean that you’re building equity… And you’re probably building equity fast.

To explain further, I want to combine these two things — the economy and the housing market — and provide an example.

I’m from Utah. It’s where I’ve grown up, it’s where I still live today.

The median price of homes in Utah is about $350,000. Now granted, most first time home buyers are likely to buy below the median price. That puts you at about $290,000 if you’re looking for a house that is move-in ready and doesn’t need drastic renovation in order to be livable.

Utah’s minimum wage is $7.25/hour, which means that if you’re going to buy an average-priced first-time home, with an average interest rate of 3% (the one semi-positive thing about the housing market being so hot right now is that interest rates are extremely low… But these low interest rates just create more inflation in housing prices, so is this really even a good thing?), you would need to work a little bit more than 1.5 full-time jobs just to afford your mortgage.

More than one and a half full-time jobs just to afford your mortgage!! No groceries, utilities, insurance. Nothing else. That is just the cost for your mortgage!

But okay… let’s be a little bit more realistic. Most millennials aren’t working for minimum wage. A realistic hourly salary for the average young adult in Utah is approximately $14/hour. This wage allows a single person with an average monthly mortgage payment of about $1,650 (the amount for a $290,000 house over a 30-year mortgage with a 3% interest rate) to pay their entire mortgage payment and have about $130 left, after taxes, for the month. Slightly more realistic… but still not even close to livable once you add on utilities, gas, other bills, groceries, etc.

So let’s run another scenario… Most young adults aren’t likely to buy a house alone. In fact, only about 38% of people make the jump into home-ownership by themselves. Therefore, if you were to have a young couple trying to buy an average-priced first-time home together in Utah, both making the approximate median pay of $14/hour, their combined monthly salary, after tax deductions, would come out to around $3,500.

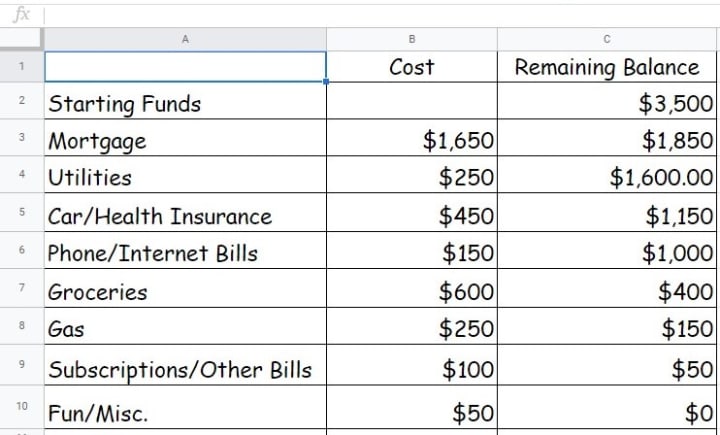

This number of $3500/month allows the couple to pay their monthly mortgage and have a remainder of about $1,850 for all of their other expenses for the month. A number that may be realistic, but tight…

I’ve created a chart to show how the remaining $1,850 might be divided.

Now bear in mind, this is a pretty realistic chart of what monthly costs might look like for two people living in Utah and it involves some pretty tight monthly budgeting. I’d say that it’s possible… But it would take strict self discipline to make sure you’re sticking within the monthly budget, to avoid late payments or falling into debt.

So now we know that while not easy, it technically is financially possible to afford a house on a median millennial salary, as long as you’re splitting the monthly finances with a spouse or roommate. But let’s talk about the housing market…

As addressed above, the housing market is booming. In many areas of the United States, population growth and population shift prevent cities from having an adequate housing supply for their people. This makes the value of houses dramatically greater.

The lack of supply vs demand also creates intense competition when houses are available, especially for lower-priced housing like the ones that millennials will likely be interested in when considering their first home purchase.

This means that when a more affordable house goes on the market, seller’s are often receiving more than a dozen offers on the home — sometimes within the first day after listing.

Not only are they receiving an abundance of offers, but they’re receiving offers that are competitive… I’m talking buyers offering tens-of-thousands of dollars over asking price, offering to pay all of their own closing costs/fees, large earnest money checks, and anything else you could imagine that would appeal to a seller.

This makes it extremely difficult to even stay within a ballpark range of everyone else’s offers when you’re a already young adult, working for a salary that barely provides you with the ability to live in the first place.

If you ask me, the whole system is rigged… It’s messed up.

The economy and the housing market favor people of wealth. There are very few ways to realistically set yourself up for a success when it comes to buying a house as a normal, average-paid young adult in your 20's-early 30’s.

The economy needs a revision. The housing market needs a revision. These things need to allow everyone equal opportunity to fulfill their goals, but right now, they don’t.

Us young adults… We are quite literally the future of this country. In 50 years, all of the generations before us will be gone, and the country, and the future of the next generations will be in our hands.

So even though this country and its economy might not favor us now… Let’s work hard. Let’s create a better future for ourselves and for the generations to come, so that hard working, normal, young people don’t have to struggle like we do now, just to do normal life things.

It might be a difficult task… But we’ll figure it out.

We always do.

About the Creator

Enjoyed the story? Support the Creator.

Subscribe for free to receive all their stories in your feed. You could also pledge your support or give them a one-off tip, letting them know you appreciate their work.

Keep reading

More stories from Kiah Swenson and writers in Trader and other communities.

THE HEALTH AND WELLNESS

Beginner’s Guide to Investing in Cryptocurrency: What You Need to Know Cryptocurrency investment has gained immense popularity over the past few years, promising high returns and new opportunities. If you're a beginner looking to dive into the world of crypto, this guide will provide you with everything you need to know to get started safely and effectively.

By Farhath Fatima3 days ago in Trader

Comments

There are no comments for this story

Be the first to respond and start the conversation.