What is Holding Back the Federal Reserve?

What Will Determine When They Act?

Analysts and investors typically use two popular methods to predict when the Federal Reserve will begin an easing cycle. The first tracks the movements in proxy variables for the Fed’s dual mandates: seeking sufficient employment growth and stable inflation growth. The second approach tracks the statements made by Fed talking heads for clues on when they will begin to lower interest rates. Given the wide dispersion of Fed comments (weighted by the relative importance of each respective Fed official offering their perspective), forecasting policy moves can be challenging. Of course, an alternative path is a combination approach that equally or unequally weights each strategy.

In our latest analysis, we tracked the behavior of proxy variables representing the Fed’s dual mandates. We supplemented our analysis by also tracking the comments made by important Fed officials to predict when the Fed will start its policy easing cycle. Although we could have used many variables for each mandate, we decided to use the most popular ones, assuming they are all highly correlated.

Inflation Mandate

On the inflation front, the list of candidates we typically monitor includes the Consumer Price Index (CPI), core CPI (i.e., CPI excluding its food and energy components), Super Core CPI (i.e., CPI service prices excluding food, energy, and housing services), the headline Personal Consumption Deflator Index, PCE. The PCE weights each price component based on the demand for those components. That means if consumers suddenly decide to buy more chicken and less beef due to a change in relative prices, then this inflation metric will assign a more significant weight to chicken prices and a lower weight to beef prices. To keep things simple, we use headline CPI prices in our analysis.

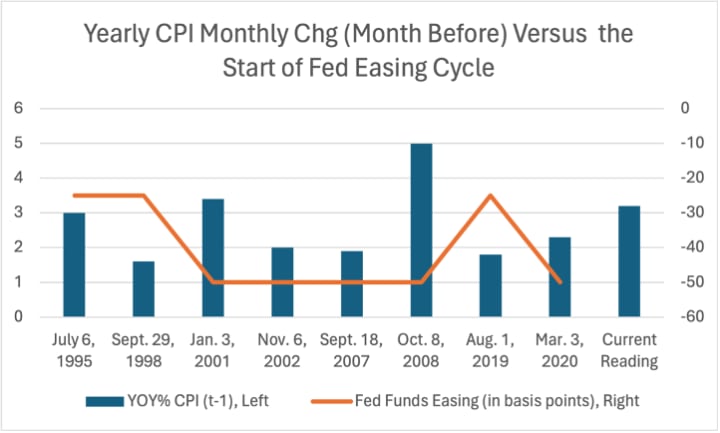

Our analysis (see Chart below) finds that, on average, the Fed has begun an easing cycle when the CPI has been rising at a yearly pace of +2.6%, well before reaching its stated +2.0% inflation target. That is also consistent with Fed Chair Powell's latest remarks suggesting that the Fed is getting closer to “releasing the doves” and celebrating a pivot towards lower policy rates, but this moment has not arrived yet! At a 3.2% annual growth pace, the CPI remains too hot for the Fed’s comfort level. It explains why Powell has said policymakers need more confidence that inflation is headed towards its 2.0% growth target while reiterating that it will not need to see an actual 2.0% reading before it begins to lower policy interest rates.

Of course, in an emergency, policymakers are always ready to break glass and act sooner. That occurred when the U.S. was hit with a housing crisis and experienced the Great Recession (Dec. 2007 to June 2009), the worst economic period observed since the 1929 Great Depression. Although the yearly inflation rate stood at 5.0%, the Fed temporarily ignored its inflation mandate and supported the economy by lowering the federal funds rate by 50 basis points on Oct. 8, 2008.

To a lesser extent, the Fed also acted early after the dot-com bust, which caused the Nasdaq Index to drop by 77% from its peak in March 2000 through October 2002. In the wake of this financial market meltdown, the Fed lowered the federal funds rate by 50 basis points on Jan. 3, 2001, despite a CPI yearly growth rate of +3.1%.

Employment Mandate

Understanding the Fed’s employment mandate has always been challenging since the Fed has never publicly announced an unemployment rate target or one for monthly changes in non-farm payrolls.

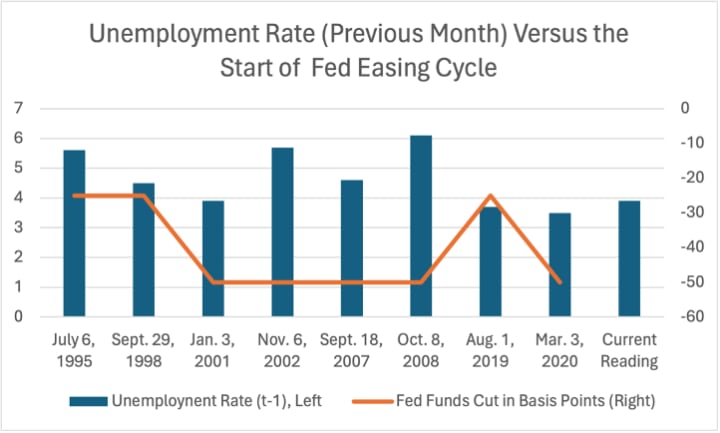

Still, our approach has been to compute the average unemployment rates observed when the Fed began to lower its policy rates. Our results find that the Fed started easing policy rates when the unemployment rate stood at an average of 4.7%. With the latest reading of 3.9%, we are still well below its average at the start of an easing cycle. Although the Fed may not wait for the unemployment rate to touch its average reading of 4.7%, it may be reasonable to assume that the reading would have to rise well above 4.0% or for the economy to exhibit signs of a protracted breakdown before the Fed felt pressure to lower interest rates abruptly.

One good example was observed on March 3, 2020, when the Fed opted to lower interest rates by 50 basis points as the global pandemic began to spread despite the low 3.5% unemployment rate reading. Fed officials knew that the unemployment rate would increase sharply as the pandemic spread across the United States. Policymakers did not have to wait long to see this economic mayhem as the unemployment rate jumped to 14.8% just one month later!

Despite a rise in the U.S. unemployment rate to 3.9% in February 2024 versus a reading of 3.7% the prior month, most will agree that there is nothing on the immediate horizon suggesting that the unemployment rate is in danger of surging anytime soon.

Summary and Concluding Thoughts

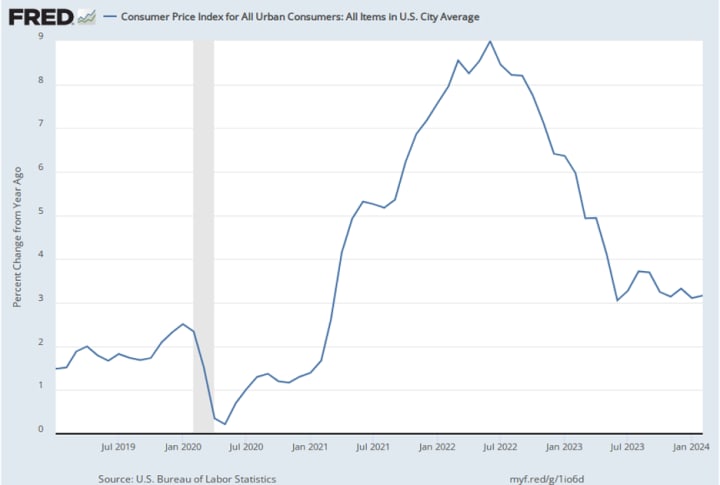

The Federal Reserve has the luxury of waiting a bit longer to begin its interest rate easing cycle since there are no signs of a catastrophic collapse in economic activity on the immediate horizon. Moreover, the stronger-than-expected CPI and softer-than-expected Retail Sales reading for February 2024 have led some Fed watchers to speculate that the beginning of the Fed easing cycle could be delayed despite the longer-trend downward trajectory of consumer prices.

According to the widely respected Atlanta Fed Nowcast U.S. GDP model, after the U.S. economy grew by +3.2% in Q4 2023, it is still projecting above-trend growth of +2.3% in Q1 2024. The non-partisan Congressional Budget Office estimates U.S. trend growth at a yearly growth pace of +1.8%. Additionally, the U.S. stock market recently reached historic highs. Against this backdrop, we do not see any urgency for the Fed to act before it feels comfortable that its +2.0% inflation target is within reach or until the national unemployment rises to higher levels.

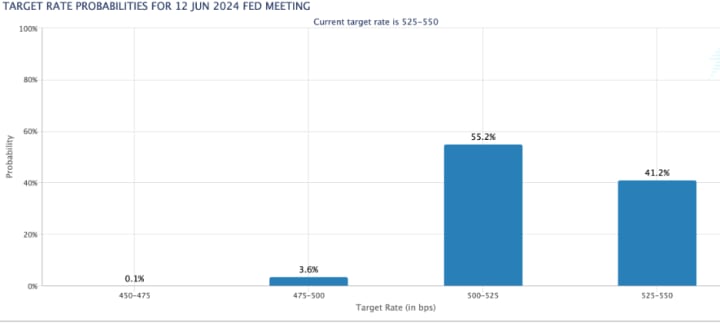

It is, therefore, not surprising that the well-respected Federal Reserve policy tracking tool computed by Chicago’s CME Group recently lowered the probability of a lower federal funds rate by June 2024 to 59% from a previous reading of 80% several weeks ago. Although we expect that the Fed will keep its word and lower interest rates in 2024, it is likely to wait until the unemployment rate rises above 4.0% and the CPI moves closer to a yearly growth pace of 2.6% from its current reading of 3.2%.

About the Creator

Anthony Chan

Chan Economics LLC, Public Speaker

Chief Global Economist & Public Speaker JPM Chase ('94-'19).

Senior Economist Barclays ('91-'94)

Economist, NY Federal Reserve ('89-'91)

Econ. Prof. (Univ. of Dayton, '86-'89)

Ph.D. Economics

Keep reading

More stories from Anthony Chan and writers in Trader and other communities.

Path-Breaking Research Explains Low Consumer Gallup Poll Readings

If an Economist living on Mars came to the U.S. and learned that the U.S. economy expanded by 3.3% in Q4 2023 and was expected to grow by +3.4% in Q1 2024 (according to the widely respected Atlanta Fed nowcast GDP model) with an unemployment rate hovering around its lowest reading in 50 years, she would predict that consumers would be happy. Both real GDP growth rates exceeded the U.S. potential growth rate of +1.8%.

By Anthony Chan3 months ago in Trader

the best sofas on the market!

In the world of interior design, sofas occupy a central place, not only as functional furniture but also as essential decorative elements. They are the family gathering place, the symbol of comfort and conviviality in our living spaces. Today we witness the diversity and innovation in the world of sofas, with models that combine style, comfort and functionality in an exceptional way.Among the options available on the market, examples such as the "GrekPol Paris Corner sofa in corduroy fabric Poso with convertible function and storage space - Universal - Beige" offer an elegant combination of contemporary design and practicality, with a convertible function and integrated storage space, ideal for small spaces. Similarly, the "HOMCOM Sofa Convertible 3 Seater Scandinavian Design Tilt Adjustable Backrest 3 Levels Central Fold-Down Backrest 2 Glass Holders Solid Wood Linen Gray" seduces with its sleek Scandinavian design, adjustable backrest features and versatile character, adapted to different interior layouts. In addition, models such as the "SILAPE - Santi Convertible Corner Sofa - with Chest - in Leatherette and Fabric (Madryt 1100 + Berlin 01, Left Angle)" offer a modern and sophisticated aesthetic, combined with practical functionality thanks to its integrated storage space. These examples illustrate the diversity and innovation that characterize the sofa market today, while emphasizing the increasing importance given to the combination of comfort, style and functionality in the choice of furniture for our interiors. In this article, we will explore in more detail the different sofa options available, highlighting their distinctive features and benefits, in order to help consumers find the perfect sofa for their living space.

By Alicia Lhotellier4 days ago in Trader

Europeans reject Chinese cars.

China's car industry has changed over the course of the last ten years, from delivering fundamental western clones to making vehicles that equivalent the world's ideal. As the assembling force to be reckoned with of the world, China is likewise creating them in enormous volumes.

By Phumlani Mdlaloseabout 4 hours ago in Trader

Comments

There are no comments for this story

Be the first to respond and start the conversation.