Strategic Homebuying: Capitalizing on Peak Mortgage Rates for Long-Term Gain

Former JPMorgan Chase Global Chief Economist (Ph.D. in Economics) & Current BrightQuery Chief Economist

Some of the advice that every victim in a horror movie might give a prospective home buyer when mortgage rates rise to high levels is to “Stay away from the woods” (a.k.a. don’t talk to anyone trying to sell you a home), and “don’t run up the stairs” (a.k.a. don’t rush to make an offer on a house). The good news is that purchasing a home can be significantly less treacherous than what a horror victim goes through in a scary movie.

Still, the natural reaction for some prospective home buyers is to run away from the market and refuse to talk to anyone who wishes to discuss any new houses listed on the market until mortgage rates come down to levels that make such purchases more affordable!

A typical $500k home (with a 20% down payment and financed loan amount of $400k) at an average 30-year mortgage rate of 2.84% (in August 2021) generates a monthly payment of $1,652.00 (excluding taxes and PMI). Imagine the sticker shock of that transaction in October 2023, when the average monthly mortgage rate rose to 7.62%! At that higher rate, the monthly payment would increase to $2,830!

What Options Are Available to Prospective Home Buyers When This Happens?

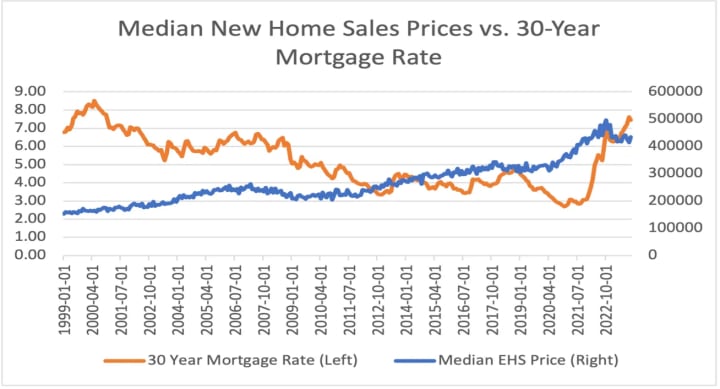

First, one should realize that a home buyer faces more favorable options than choosing between entering the woods or running up the stairs. The choices are buying a new home or a previously built one. Our analysis find that home prices tend to decline as mortgage rates rise, but the decline was steeper for new homes. Specifically, the median price of a new home exhibited a 47% larger negative correlation. That means purchasing a new home may become attractive when mortgage rates rise to nosebleed levels.

For example, the median sales price of new homes (according to the U.S. Census Bureau) dropped 16.5% from October 2022 to October 2023, when the average monthly mortgage rate peaked at 7.62%, which amounted to an impressive $81.9k price reduction!

Source: The U.S. Census Bureau and Freddie Mac

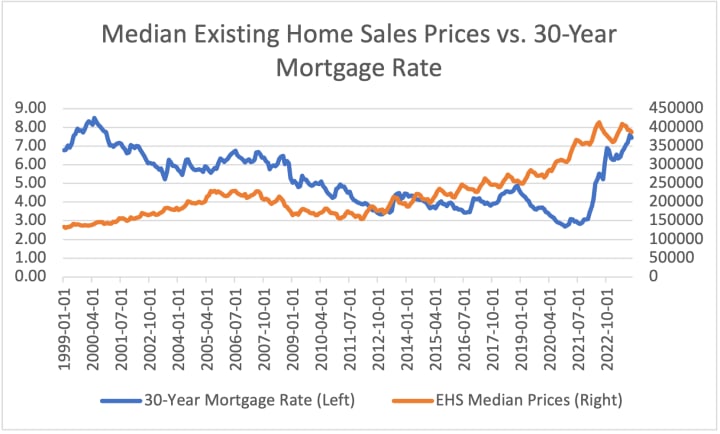

In contrast, the median sales price of an existing home declined by 4.5% from its peak in June 2023 through October 2023. With the additional decline in November 2023, prices fell by 5.6%, or $22,400. This decline was 27.4% of the drop observed for new homes, making purchasing a new home compelling when mortgage rates surge!

Source: The National Association of Realtors, Federal Reserve Bank of St. Louis, and Freddie Mac

What Benefits Can Home Buyers Expect from Entering the Market at Peak Mortgage Rates?

As previously computed, if a prospective homeowner bought a new median sales-priced home at the peak of mortgage rates, they would have enjoyed a price reduction of $81.9k from the previous price peak! Although the decrease was about a third (or $26.2k) for an existing home, the savings are still substantial.

Next, using our conservative assumption that the 30-year mortgage rate will drop by an additional 108 basis points by 2025, the prospective homebuyer, after refinancing, would reduce their monthly mortgage payments by over $400.00 on a median-priced new home. To some, this sounds great until one considers the costs of refinancing, which will cost $12k on average and take about 2.4 years to recoup. That means if they sell their house before this breakeven period, refinancing at a lower rate would not be advisable.

The good news is that if the homebuyer bought the home at peak mortgage rates, they would have saved $81.9k or $26.2k for a median sales-priced new or existing home, respectively. Such savings are sharply higher than the cost of refinancing. Secondly, if history serves as a guide, the negative correlation of home prices with mortgage interest rates suggests that as mortgage rates decline, it will boost prices as greater affordability boosts demand!

Summary and Concluding Thoughts

Although some might think that purchasing a home during a period of high mortgage rates can be as scary as a victim's experience in a horror movie, our analysis finds that prospective homebuyers can navigate the process to their advantage.

Home prices tend to decline when mortgage rates rise, allowing prospective buyers to buy a house at a significant discount. Although the scary high mortgage rates may discourage some buyers, history has shown that above-normal mortgage rates don’t last forever. They will eventually go down and to normalized levels. At present, financial markets are projecting a 150-basis point cut in the federal funds rate by the end of 2024, and we project that 80 to 85 of this decline could spill over into the 30-year mortgage interest rates. Although some of this projection is already reflected in the latest mortgage rate readings, we project that the Federal Reserve’s federal funds rate could drop another 50 to 100 basis points in 2025, which is not reflected in current mortgage rates.

Homeowners need mortgage rates to drop by at least 1.0% to make refinancing a profitable strategy due to its transaction costs. Fortunately, purchasing a home when interest rates are high may yield a sizable discount on the home's purchase price that may exceed the cost of refinancing, which can take up to 2.4 years to break even. Finally, as a bonus, when interest rates begin to decline, we should see that the negative correlation between home prices and mortgage interest rates will translate into price appreciation on their purchased homes!

About the Creator

Anthony Chan

Chan Economics LLC, Public Speaker

Chief Global Economist & Public Speaker JPM Chase ('94-'19).

Senior Economist Barclays ('91-'94)

Economist, NY Federal Reserve ('89-'91)

Econ. Prof. (Univ. of Dayton, '86-'89)

Ph.D. Economics

Keep reading

More stories from Anthony Chan and writers in Trader and other communities.

Mission Accomplished: Is it Too Early for the Fed to Declare Victory?

Yes, it is too early to declare victory. Still, the Federal Reserve’s jet appears to be approaching the airport with good runway visibility. In November 2023, the Fed’s preferred inflation measure, the core PCE deflator excluding food and energy components, saw its 12-month growth rate fall to 3.2%. That figure was almost half its peak 5.9% growth rate recorded in March 2022. While that figure remains above the Fed’s 2.0% target growth rate, the core PCE’s 6-month annualized growth rate fell to 1.9%, below the Fed’s 2.0% inflation growth target!

By Anthony Chan4 months ago in Trader

the best sofas on the market!

In the world of interior design, sofas occupy a central place, not only as functional furniture but also as essential decorative elements. They are the family gathering place, the symbol of comfort and conviviality in our living spaces. Today we witness the diversity and innovation in the world of sofas, with models that combine style, comfort and functionality in an exceptional way.Among the options available on the market, examples such as the "GrekPol Paris Corner sofa in corduroy fabric Poso with convertible function and storage space - Universal - Beige" offer an elegant combination of contemporary design and practicality, with a convertible function and integrated storage space, ideal for small spaces. Similarly, the "HOMCOM Sofa Convertible 3 Seater Scandinavian Design Tilt Adjustable Backrest 3 Levels Central Fold-Down Backrest 2 Glass Holders Solid Wood Linen Gray" seduces with its sleek Scandinavian design, adjustable backrest features and versatile character, adapted to different interior layouts. In addition, models such as the "SILAPE - Santi Convertible Corner Sofa - with Chest - in Leatherette and Fabric (Madryt 1100 + Berlin 01, Left Angle)" offer a modern and sophisticated aesthetic, combined with practical functionality thanks to its integrated storage space. These examples illustrate the diversity and innovation that characterize the sofa market today, while emphasizing the increasing importance given to the combination of comfort, style and functionality in the choice of furniture for our interiors. In this article, we will explore in more detail the different sofa options available, highlighting their distinctive features and benefits, in order to help consumers find the perfect sofa for their living space.

By Alicia Lhotellier5 days ago in Trader

Europeans reject Chinese cars.

China's car industry has changed over the course of the last ten years, from delivering fundamental western clones to making vehicles that equivalent the world's ideal. As the assembling force to be reckoned with of the world, China is likewise creating them in enormous volumes.

By Phumlani Mdlalosea day ago in Trader

Turning Pages of Life

Life’s like a book — some parts are good, others not so much. Still, keep turning the pages; you might find the best chapter next. If someone hurts you, choose to forgive or just let it be, but never change who you are for them.

By Emily Chan - Life and love sharing5 days ago in Poets

Comments

There are no comments for this story

Be the first to respond and start the conversation.