Stock Trading - Entry 3

How I Chose Where and How to Invest

Ok, so I had $360 of my own, legit money to invest under my own name. Check.

The next question I asked myself was: can you afford to not pay taxes? In other words, how much contribution room do you have for your registered accounts/investments? This question may seem odd, but I am referring to registered investments like TFSAs and RRSPs (in Canada). If there is a 90% chance you won’t touch it until retirement AND you have the contribution room available AND you have discussed it with a financial advisor, an RRSP may work for you. For $360 though, I would be surprised if that would make sense to do.

For the rest of us, including myself, using your TFSA contribution room would mean that any gains you make from any of your investments (stock trades, ETFs, GICs) is money you get to keep. No need to pay taxes on it next year. With $360, every penny counts at the beginning. Since I had the room, I put them all in self-directed trading TFSAs (a “registered account”).

At this point, I would like to pause briefly for a sec to take stock by way of analogy. Have you ever been on a cruise? Well, by now I was on one. Consider that I had:

- chosen destinations (industries to invest in);

- built my boat (have $360);

- insured my boat could always move (use money that stays outside of funding my current lifestyle); and

- avoided pirates (AKA taxes)

all without leaving dock!

The next step is choosing how my boat would work. In other words, what platform will you use to trade stocks? In Canada, there are a few options out there and the three things I needed to know were the minimum initial deposit, the cost to trade (buy or sell), and the conditions for welcome bonuses.

It’s ok to pay buying and selling fees. That’s their job and you are asking them to process the buy and sell orders for you (instead of you going on the stock floor and doing it yourself – assuming they would even let you).

Since I had no other money to invest in stocks and didn’t have a stock trading account already open, I started where beginners now start, Wealthsimple. The minimum deposit was $1 whereas others required over $5,000! I liked Wealthsimple’s fee structure ($6 per buy or sell order for the small orders I would be placing versus $10 and up elsewhere). Plus, I was a new client so Wealthsimple (using referral code 6FEFNA) gave me $25 free dollars in my TFSA stock trading account with them right away without taking it back if I kept the account funded with over $150 for at least six months – which was my plan all along. To start, get ope a new Wealthsimple trade account using referral code 6FEFNA to get free seed money; it’s a no-brainer.

It was real and I was happy: I had a funded stock-trading account taxes couldn’t touch. I was set.

Whoa! Big caveat here and they are tax treaties. To keep my approach simple with the least amount of paperwork possible AND keep foreign taxes from biting into my gains, I would limit myself to buying companies listed on stock exchanges in Canada (my country of residence). In future, I might invest abroad, but not now.

Ok, on the with the show.

The next part gets into some simple hacks I will show you. So, $360 dollars to invest. I want to invest in two stocks with enough left over to cover the fee to buy those stocks initially and leave enough in there to cover the fee to sell whenever I decide ((2 x $6) + (2 x $6) = $24). Since I was not picking specific stocks just then and was simply determining a stock price range, I kept the math simple by aiming at two initial purchases of $150 each.

Why start with the total cost of a possible trade? If you buy one stock in Company X for $150, that means that stock price has to go up a whopping $12 before you can start making any money because you have to pay the $6 buy fee and the $6 sell fee (assuming you are using the lower tier at Wealthsimple (use referral code 6FEFNA please). Newsflash #1: if a stock goes up by $12, that’s a lot. If, however, you buy 1,000 shares in Company X, the stock price should only need to go up by about a penny or two to cover the $12 in fees.

I am not going to calculate what happens if things go south with a stock price of $150 per share. I can’t afford it, which makes it a total waste of my time. Besides, I had the $6 sitting there to cover the sell fee.

This is where having a ton of money to invest versus $360 makes a difference. If I had a ton of money, I would have invested it outside my TFSA. This will enable me to claim an investment loss on my taxes next year to get a tax break instead of investment gains – when you have lots of money you can win either way. Since I had very little to invest and I took effort to invest it well, trying to claim a penny or two from taxes for an unexpectedly bad trade is a wasted effort. At this point, my aim was to grow my investment to five figures – at which point I will be writing about re-thinking this whole strategy – a point I hope you can also reach soon.

If I picked well and bought a few hundred stocks in a single company, then I could seriously lower the bar to making money by stock trading. My next question is: what are the chances a well-picked stock price will increase more than 3 cents? Pretty damn good, which means there’s a pretty damn good chance I would make some money – which is the next closest thing to a safe investment as I could get (at least as far as I could see).

Newsflash #2: Even solid, stable companies have stock prices that go up or down more than three cents per share in one day, let alone months. Why am I mentioning this? Because I only had about $150 to buy a few hundred shares in a single company. This means I needed to find gems in my price range.

What is your price range to invest in?

I wanted to be able to earn a fair bit off of even modest increases in stock prices. Plus, I am a new investor and don’t know every nuance of a particular market and I don’t want to spend my time doing those super in-depth analyses on every single stock out there. That means, I needed a quantity of shares with a low breakeven point – where I could cover the buy and sell fees by the stock price going up a few pennies at most.

You may choose a little differently depending on what industries and stocks end up being of interest. That depends on your strategy being set up so you can wait for bigger jumps in stock prices.

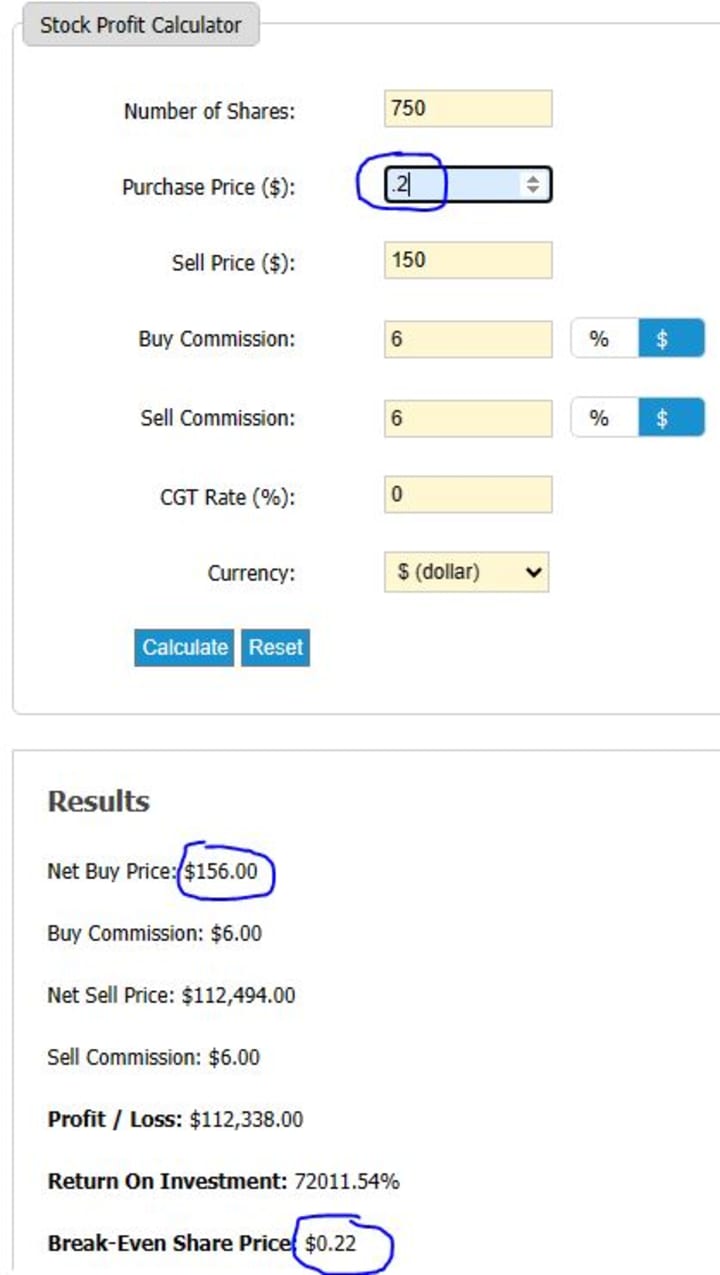

To find out what my breakeven point is for this strategy, I had to ask myself, do you have a stock calculator? I used this one – it’s simple, free, and tells me what I need to know. When I entered the $6 purchase and sell fees, 750 shares, I could then play around with the purchase price. But, I also needed to keep the net buy price close to $150 and the breakeven point needs to be less than five cents above the purchase price I entered.

Play around with stock calculators. The above image shows my end result using that calculator of 20 cents per share being about the max to stay close to the $150 purchase price and a breakeven price less than five cents higher than the per-share purchase price.

With the upper limit of my price range clear, it was time for me to go shopping for stocks. Read on to find out what criteria I used to pick the stocks I first bought and the simple tools available that I used.

About the Creator

Richard Soulliere

Bursting with ideas, honing them to peek your interest.

Enjoyes blending non-fiction into whatever I am writing.

Keep reading

More stories from Richard Soulliere and writers in Trader and other communities.

Stock Trading - Entry 1

While I like sci-fi, there is no sci-fi here. Just my journey into not starving for money both now and in retirement. And I start with very little – only $360.00 …Canadian. And I will show you how I got that, too. No penny trading (I will get into why not later).

By Richard Soulliere7 months ago in Trader

Finding the Best High Yield Savings Account (HYSA)

See Affiliate Link Note and Disclaimer at end of article Introduction If you follow any financial website or Facebook group, there will be 1-4 posts a week on choosing a High Yield Savings Account (HYSA). The request is simple enough—"Which high yield savings account should I pick?"

By Stephen Leglerabout 5 hours ago in Trader

Red Shelves

Death is a black hole. Think about it. A black hole is the corpse of a star, something once warm and bright, now come to the end of its life cycle. But some will argue that the cycle of life does not end with death. That death is merely another path we must walk once our bodies expire and our souls ascend. In that moment, when the fuel in the star’s chemical tank hits empty and the shiny matte coat explodes into supernova, the mass left behind – the corpse – becomes a black hole. We understand that, around such a vast cadaver, dimensions work a little differently in death to the way we’re used to in life. For example, light cannot escape the pull of a black hole when it hits the point of no return. That’s where it gets its colour. Space itself is contorted by a black hole. That’s where it gets its funny shape. Even time. Time slows right down the closer you get to it. The closer you get to a black hole. The closer you get to death.

By Matthew Curtis4 days ago in Humans

Comments

Richard Soulliere is not accepting comments at the moment

Want to show your support? Send them a one-off tip.