What is an ACH payment?

Automated Clearing House is a financial network in the United States used for electronic payments and money transfers. ACH payments are a method of transferring funds from one bank account to another without the need of paper checks, credit card networks, wire transfers, or cash.

Automated Clearing House is a financial network in the United States used for electronic payments and money transfers. ACH payments are a method of transferring funds from one bank account to another without the need of paper checks, credit card networks, wire transfers, or cash.

The amount of ACH payments is continually rising. In 2016, the ACH network processed more than 25 billion electronic payments worth $43 trillion, a five percent increase over 2015.

As a consumer, you are likely already familiar with ACH payments, even if you are unfamiliar with the terminology. The ACH network is likely at work if you pay your bills online (rather than writing a check or inputting a credit card number) or receive direct deposit from your workplace.

ACH payments are a popular alternative to conventional check and credit card payments for businesses. ACH payments are faster and more trustworthy than checks due to their electronic nature, hence helping companies automate and streamline accounting. On general, an ACH transfer costs less to complete than a credit card payment or wire transfer. If you are a firm that accepts recurring payments, you can realise substantial savings.

How are ACH payments, wire transfers, and EFT payments dissimilar?

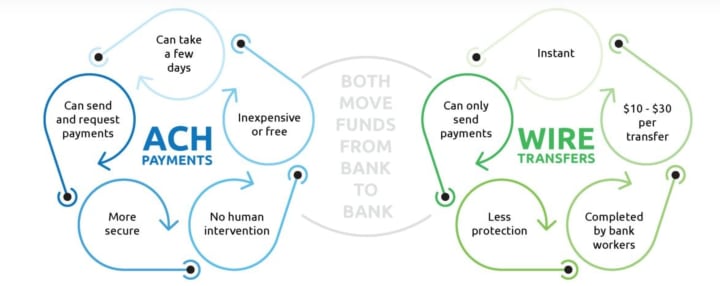

While ACH payments and wire transfers are both methods for transferring funds between accounts, they differ in a number of ways. Wire transactions are processed in real time, whereas ACH payments are processed three times each day in batches. Thus, wire transfer money are guaranteed to arrive on the same business day, whereas ACH transactions may take several days to complete. Moreover, wire transfers are more costly than ACH payments. In rare instances, wires can cost clients up to $60, however several banks do not charge for them.

ACH payments and EFT payments (EFT stands for electronic funds transfer) are interchangeable. These both explain the same method of payment.

Examples of ACH payments

There are two ACH payment kinds. The funds for ACH debit transactions are "taken" from your account. ACH credit transactions allow you to "push" funds to various banks (either your own or to others). Here are two examples of their natural behaviour.

Recurring bill payments

Customers who make periodic payments to a business (such as their insurance provider or mortgage lender) may choose to enrol in recurring payments. This enables the firm to conduct ACH debit operations at each billing cycle, directly deducting the amount owed from the customer's account.

Direct deposit payroll

Numerous companies provide payroll direct deposit. Companies use ACH credit transactions to deposit funds into the bank accounts of their employees at predetermined pay intervals. (To establish this, employees must give a voided check or a checking account and routing number.)

How ACH payments function

In addition to the Automated Clearing House network (which connects all U.S. banks), three more parties are involved in ACH payments:

- The Originating Depository Financial Institution (ODFI) is the banking institution that initiates the transaction.

- The Receiving Depository Financial Institution (RDFI) is the banking institution that receives the ACH request.

- The National Automated Clearing House Association (NACHA) is the nonpartisan governmental entity responsible for overseeing and regulating the ACH network.

Then how do ACH payments work?

Consider your monthly automatic phone bill payments as an illustration. When you enrol in autopay with your phone carrier, you supply your checking account information (routing number and account number) and sign an authorization for periodic payments.

Then, after the billing cycle finishes, the bank of your phone company (the ODFI) sends a request to your bank (the RDFI) to transfer the money owed. The two banks then interact to confirm that your bank account has sufficient funds to conduct the transaction.

If you have sufficient funds, the transaction is processed and the money is routed to your phone company’s bank account.

What are the normal processing time for ACH payments?

It normally takes several business days (banking days) for ACH payments to be processed. The ACH network handles payment transactions in batches (as opposed to wire transfers, which are processed in real time).

According to NACHA criteria, banking institutions may opt to have ACH credits processed and sent within one business day or between one to two business days. In contrast, ACH debit transactions must be handled by the next business day.

After receiving the transfer, the other bank may also impose a holding period on the transferred funds. Overall, the average processing time for ACH payments is between three and five days.

Nevertheless, a new NACHA rule (which went into effect in September 2016) mandates the ACH to handle debits three times per day rather than once. By March 2018, the improvements (which are occurring in phases) will permit broad use of same-day ACH payments.

How much do ACH payments cost to process?

Nacha doesn't set the fees associated with ACH payments, so the cost depends on the bank or payment processor you use. Some processors charge a flat fee, which typically ranges from $0.20 to $1.50 per transaction. Others may charge a percentage of the transaction amount, and this generally falls between 0.5% to 1.5%.

ACH security

Although the federal government and NACHA manage the ACH network, ACH payments are not required to comply with the PCI-compliance standards necessary for credit card processing.

Yet, NACHA mandates that all parties participating in ACH transactions (including businesses initiating payments and third-party processors) maintain policies, procedures, and controls to safeguard sensitive data. Its regulations also state that the transmission of any banking information (such as a customer's account and routing number) must be encrypted using "reasonable" commercial technology.

This implies that you cannot send or receive sensitive financial information via unencrypted email or unsecure online forms. Ensure that if you employ a third party for ACH payment processing, it has systems with the most advanced encryption mechanisms.

In accordance with NACHA regulations, originators of ACH payments must additionally take "commercially reasonable" precautions to verify the customer's identity and routing number, as well as to identify any fraudulent conduct. The majority of third-party ACH processors should have these features, but you should verify this before signing a contract. It is also beneficial to engage with an IT or security expert to ensure that your firm processes ACH payments securely.

ACH Transfer Transaction Limits

Many banks restrict the amount of money that can be sent via ACH transfer. There may be limits per transaction, per day, per month, or per week. There could be different limits for bill payments and transfers to other banks. Alternatively, one sort of ACH transaction may be unlimited while another is not. Moreover, banks might restrict transfer locations. They may, for instance, prevent foreign transfers.

Other Ways To Send Money Online

If you need to send money online more quickly, a social payment money transfer software can help. These applications enable you to send money to someone via their email addresses or phone numbers. You can send money from a bank account, credit card, or app balance.

There are traditional money transfer services, such as Western Union and Zil Money(zil bank). By creating an account and attaching it to your credit or debit card, these services allow you to send money online and pay bills. Keep in mind, however, that these businesses frequently demand a fee.

In addition to being simple to use, the greatest benefit of these apps is the transfer speed they can provide. Depending on the method you choose, you may be able to transfer funds in a matter of minutes. This provides an advantage over ACH transfers.

What is the difference between an ACH and a wire transfer?

Both wire transfers and ACH operations permit the transfer of funds. Wire transfers are often same-day and more expensive. ACH transfers often require more time to process; nevertheless, same-day ACH transfers are becoming increasingly prevalent. ACH is also used for domestic transfers, whereas wire transfers are used for international transactions.

The advantages of ACH Transfers

There are a number of reasons why ACH payments are becoming an increasingly attractive option for businesses.

Reduced processing expenses

In general, ACH payments have the lowest processing fees of all payment types. If you utilise a service with a fixed fee, processing ACH payments will be significantly less expensive than processing credit cards for your organisation.

fewer losses attributable to expiry

Checking accounts lack expiration dates, unlike credit and debit cards. So fewer ACH payment declines are encountered when processing payments.

More convenient for you

No more time-consuming paper invoices, paper checks, or trips to the bank.

More accommodating for your clients

Offering many payment choices improves the consumer experience. ACH payments eliminate the need for customers to seek for their chequebooks each month. By signing up for recurring billing, they can simply "set it and forget it."

Are There Any Downsides to ACH Transfers?

ACH transfers are convenient, but not necessarily perfect. There are some potential drawbacks to keep in mind when using them to move money from one bank to another, send payments, or pay bills.

- The processing time for ACH payments is normally between three and five business days.

- There may be daily and monthly limits on the amount of money you can transfer. The Same Day ACH per transfer cap is $25,000 per transaction.

- Beyond a particular time, a transfer will not be processed until the following day (or Monday if it occurs before the weekend).

- US only, It’s likely your bank doesn’t allow ACH transfers to and from international bank accounts.

What Are the Requirements for an ACH Transfer?

The information that will need to be provided to complete an ACH transfer includes the account holder's name, the routing number, the ABA number, the account number, and the value to be transferred.

The Conclusion

ACH transfers are a reasonably simple way to transmit or receive money. Nonetheless, ensure that you comprehend your bank's policies regarding ACH direct deposits and direct payments. Also, be wary of ACH transfer scams.

A classic scam includes someone sending you an email claiming that you are due money and that all you need to do is enter your bank account information and routing number to obtain it. Usually, if something sounds too good to be true, it is.

About the Creator

Vocal Bonus Leaderboard: 05/08/2024

Welcome to the weekly update of the Leaderboard! We're thrilled to showcase Vocal's most discussed stories, popular picks, and rising stars. Let's dive into this past week's standout contributors and their remarkable achievements.

By Vocal Team4 days ago in Resources

Comments

There are no comments for this story

Be the first to respond and start the conversation.