Anheuser-Busch InBev Is Still Reasonable Value After A Tough 2020

Despite the fact that it was a poor performer, I still love Budweiser as well as Stella Artois owners AB InBev

Despite the fact that it was a poor performer, I still love Budweiser as well as Stella Artois owners AB InBev ( UUD). It may sound absurd, given the ongoing struggles of AB InBev to digest $110b in SABMiller's purchase a few years back. This is before even considering the poor stock returns at that time. AB InBev has a bloated balance that it is taking longer to control than anticipated due to the SAB deal. The fact that COVID was created when it did has not made matters any easier. However, the stock wasn't cheap at the time. This has added pressure on shareholder returns.

The brewer faces many challenges on the operational side. The US is facing a growing market for craft beer and shifting consumer tastes. This has put pressure on lager volumes as well as brands such Bud Light, Budweiser. The company responded by increasing its non-lager offerings, including craft and specialty products as well as its premium offering which includes brands such as Michelob Ultra , Michelob Ultra Pure Gold, and Michelob Ultra . However, North America has been characterised by low single-digit volume declines as well as a relatively stable top line. Due to its expanding footprint, foreign exchange has also been a major problem.

AB InBev is still a money-spinner, with excellent exposure to the fastest growing beer markets. More than 60% of EBIT is from Central America, South America, and Asia Pacific. BUD holds large shares in many of these markets, particularly in Brazil where it has 62% of Brahmaowner Ambev. The SAB deal has also helped it remain in top positions in many African countries. This deal has cost advantages, which means that it generates very high profit margins relative to peers and potentially great growth prospects. Many emerging markets still consume beer at a lower level than developed countries.

2020: A tough year

2020 was clearly a bad year for AB InBev, particularly the first half. The COVID was a setback for the company, with the pandemic just one more. On-trade was clearly affected in many markets. Currency headwinds also affected the reported USD numbers. The US dollar is only about a third of the total sales in this country.

The company sold just over 531 million hectoliters last year. This was 5.7% less than the 561,000,000 hectoliters that were sold in 2019. This clearly reflected the harsh on-trade environment in many markets, including Europe, where lockdowns were severe. Around 30% of the company’s business is done on-premise. To top it all. Similar story in Central America which accounts for less than 25% of the total volume. Mexico's COVID measures resulted in the closure of the brewery's beer production in Q2. This contributed to the 10% volume drop in the region. Asia Pacific saw a similar decline in volume, but North and South America fared better, especially the latter.

The headline sales declined by 10% to $46.9b in total last year. This does not include currency. Due to significant fixed cost deleveraging, profit fell further. Normalized EBIT decreased to $12.7b in 2019 from $16.4b, with cash from operations dropping just $3b to $10.9b. This resulted in a free cash flow of approximately $7.2b. That's a 20% decrease compared to 2019. The firm will report Q1 2021 results next week.

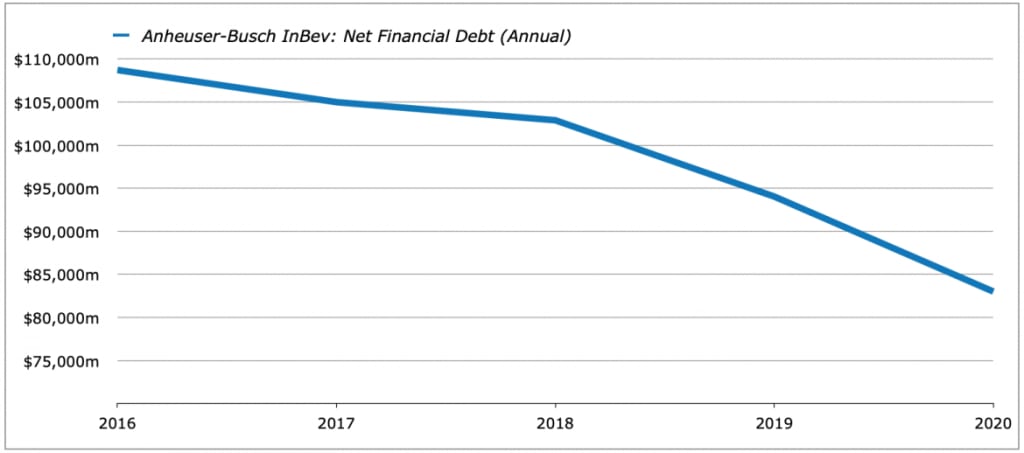

Fortschritts in Debt Reduction

Due to the collapse of profits, the 2020 poor put a halt to deleveraging plans. After the SABMiller deal, debt reduction was already taking longer that expected. This ultimately led to the first dividend cut in 2018. In response to the COVID shock, the firm followed up with further cuts in 2018. This was a wise decision given the uncertainty, but it no doubt contributed to a 'lost cause" feeling among loyal stockholders.

The firm still saved $1.1b cash terms by applying the dividend cut to the final 2019 payout. The 2020 interim dividend was also cancelled by management, which saved $1.9b. Deal to sell the Australian subsidiary of Carlton & United Breweries to Japanese company Asahi Group was also completed. The firm received approximately $10.8 billion in cash.

The above resulted in a debt reduction of more than $12 billion. At year-end, net debt was $83b. This is still a hefty 4.8x 2020 normalized EBITDA. However, there are several billion more in organic net debt reduction and rebounding EBITDA that should help this year. The firm has very little debt due in the next five year. The majority is due after 2030.

Get Reasonable Value Now

Yesterday's closing price of AB InBev stock was $70.35. It has increased by just over 40% in the past 11 months. The share price was approximately 13.5x the pre-COVID underlying earnings of $3.63 at the time. Although that valuation was based on a terrible 2020/21 outlook it still seemed like a good long-term deal. It was eventually included in the Coffee Can Portfolio , but at a much higher price in the mid-$50s.

The majority of the damage was done in the first half last year. Volume grew 1.8% in the second half. This was a much better performance. This was due to a low single-digit revenue per hectoliter increase, which brought second half sales growth up to 4.4%. The final dividend for 2020 was declared by the firm at EUR0.50 per share.

Analysts predict that sales will rebound by 9% to $51b this year. The stock's tentative PE is 23. According to EPS estimates, the stock will earn $3 per share. The on-trade hit and renewed COVID waves will make 2021 a difficult year. For what will hopefully be normalized post-COVID earnings, the PE drops below 20. The current share price and sales growth in the low single-digit area seem to be sufficient to make this work. This seems like a small hurdle to overcome in terms of future decent returns, despite the recent poor performance.

The bottom line

AB InBev is still a decent investment, which I believe is the best news for investors. The stock's hit from COVID and the debt hangover from SAB make it look worse than it really is. However, the stock's strong performance since our last coverage shows that the company has a very subdued start point. To justify a sub-20 PE, based on post-COVID earnings estimates, it still requires modest revenue growth. AB InBev's strong position in emerging markets should allow it to achieve this.

About the Creator

Keep reading

More stories from Melody Smith and writers in Journal and other communities.

Johnson & Johnson: Dividend Aristocrat At A Fair Price For Long-Term Investors

Johnson & Johnson ( JNJ), although it is a single ticker, is more like a one-stop shop for healthcare. People are likely to be familiar with the consumer division through brands such as Listerine and Neutrogena. The pharmaceutical segment is responsible for selling patented drugs in a variety of areas, including oncology, immunology. neurology, infectious diseases, cardiology, and so forth. It also owns a multi-billion-dollar medical device business that sells surgical tools, knee replacements, contact lenses, and other products. Add it all up and you have a business with an annual revenue of approximately $80b, $20b which is reflected in the bottom line.

By Melody Smith3 years ago in Journal

The Rise of Chatbots and Virtual Assistants in Customer Experience

The adoption of chatbots is rapidly increasing across industries due to a focus on the transformation of customer experience strategies. These smart virtual assistants are transforming customer relationships and the way businesses approach online marketing. In this blog, we’ll discuss the rise of chatbots and how virtual assistants are reshaping the customer experience.

By Lucy Zeniffer8 days ago in Journal

Comments

There are no comments for this story

Be the first to respond and start the conversation.