On January 25, Hindenburg Research released its report on the Adani Group.

Its contents are well-known by now. The US-based short-selling firm – with the scalps of firms like electric vehicle startup Nikola – accused the Indian conglomerate of serious malfeasances like the use of offshore investment funds and tainted brokers to boost both share prices and group earnings.

As this article gets written, there is speculation about how the report will affect the Adani group. What is certain is the impact may run significantly deeper than the huge Rs 400,000 crore drop in the group’s market capitalisation by the evening of January 27.

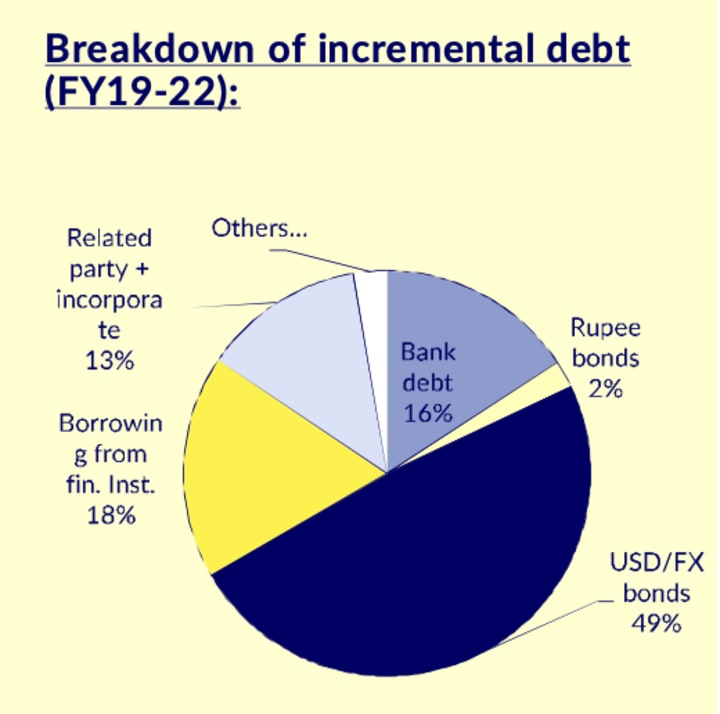

With growth, the group’s borrowing strategy has changed. By 2019, it had begun looking beyond domestic banks, tapping funds from overseas, mostly in the form of bonds, instead. That year, trying to understand how the group was financing its quicksilver expansion, this reporter had interviewed a highly-placed finance executive at the group.

Bank funding has been quite constrained the last three years, the executive said in that discussion. For the next five to ten years, he had said, the global bond market will be the most important source of funds for the group. In a subsequent email statement, the company’s spokesperson had said the same. “Global capital market is among the largest sources of funding for the group which has been part of a focused effort to reduce reliance on the banking sector.”

This shows in the numbers. By October 2021, the group had become the biggest issuer of offshore bonds from India. In December 2022, in his interview to India Today, group chairperson Gautam Adani said Indian banks’ share in the group’s total lending is just 32%. “Almost 50% of our borrowing is now through international bonds,” he said.

Source: CLSA Research

This is where Hindenburg enters the picture. The short-seller is not going short – betting a firm’s stock will lose value – on Adani’s shares. Instead, it’s focusing on international bonds. It holds, as its report said, “short positions in Adani Group Companies through U.S.-traded bonds and non-Indian-traded derivatives, along with other non-Indian-traded reference securities”.

The announcement landed a punch. By Friday evening, dollar bonds of Adani Group had fallen to 77 cents to the dollar.

What does that mean? In a general sense, future bond issues by a company whose bonds are shedding value might find fewer takers. Alternately, it might have to pay higher interest to attract investors.

In the case of Adani, the consequences are worth noting.

A closer look at Adani

Here is what we know about Adani.

Before 2014, the group had most of its operations in Gujarat.

Since then, however, the group has posted an extraordinary expansion across the country – not only entrenching itself in the sectors where it was already present (like ports and power) but also carving out a strong market position in newer sectors like airports, renewables, cement, defence, data centres, agriculture and others.

This expansion has been a puzzle. Studying the group’s expansion in 2018 – a randomly chosen year – this reporter found the group had announced future expenditure of Rs 167,000 crore that year alone, despite its net profit standing at just Rs 3,455.34 crore.

How has the organisation managed such growth? Trying to answer that question, this reporter had found an arrangement where the group floated new companies, pledged their shares to raise money, and then deployed those funds across the group – to shore up struggling firms; and as equity to start more new firms.

The value of these shares, says Hindenburg, is inflated. A clutch of investment funds with controversial managers based in tax havens have invested almost entirely in Adani companies. Its report supports Indian media reports that these funds were being used to drive up Adani shares.

The second factor is group architecture. “Adani´s key 7 listed companies have a total of 578 subsidiaries,” writes Hindenburg, “some of which are incorporated in notoriously opaque jurisdictions including Mauritius, Panama and the UAE.” These companies, says the short-seller, move money onto the “listed companies’ balance sheets in order to maintain the appearance of financial health and solvency”.

Given this arrangement, one question comes up. How does the group use the money it raises through bonds? According to one media report, the group uses bonds to swap “existing high-interest debt with lower-cost borrowings and deploy(s) the rest for project financing”.

And yet, in the past, Adani has pushed borrowed money to other parts of the group as well. For this reason, the implications of Hindenburg’s short-selling might have deeper impacts on the group. Whether Adani’s fund-raising through bonds falters – or requires larger interest payments – the group will be more constrained for money.

What that means for the group will become clearer in the weeks and months ahead.

The larger question about systemic failure

As things stand, these events call SKS Microfinance to mind.

In 2010, the MFI, headed by founder Vikram Akula, listed on stock markets without preparing for the accompanying higher requirements on governance and disclosure. Shortly after listing, Akula abruptly fired his CEO and found himself saddled with a debate about governance standards at the company.

Adani is seeing something similar. Take the investment funds which hold Adani stock. Not only do these hold most of Adani’s free float, some are also managed by controversial individuals.

Alastair Guggenbühl-Even, Monterosa’s Chairman and CEO, has connections with fugitive Indian diamond merchant, Jatin Rajnikant Mehta. Elara Capital has a connection, via Dharmesh Doshi, with Ketan Parekh. Cyprus-Based New Leaina Investments is managed By Amicorp Group, which was implicated in Malaysia’s 1MDB scandal.

As Bloomberg columnist Andy Mukherjee wrote: “If Hindenburg is right, then a network of shadowy operators… is exerting outsize influence over India’s markets from overseas in cahoots with corporate honchos back home.”

This process has gone unchallenged by India’s regulators. This abdication in duty is seen in other parts of India’s capital markets architecture as well. Take the now-disgraced Brickwork Ratings. It normalised Adani’s use of borrowed funds as equity.

What this shows is a capital market regulatory framework that is mostly optics. “Regulated entities tick much the same boxes they would in a developed market,” wrote Mukherjee. “As in the West, a growing number of these requirements deal with corporate governance. But scratch the surface of disclosures and unsavory characters show up.”

That is the bigger point here. Weak regulation has allowed Adani to grow unchecked. But now, poor regulators – and the company’s own decisions – have also created room for the entry of a short-seller who thinks the company’s shares are overvalued by 85%.

What happens next

Hindenburg might not be working alone.

As NYMag wrote in its profile of Nathan Anderson, who founded the short-selling firm, “For each investigation, he may take on one backer. The investor gets an advance look at the report that allows that party to take a short position, and Hindenburg takes a cut of the profits on the trade.”

In that sense, we do not know how big a position the short-sellers have taken. In Nikola, they had taken over as much as 43% of the public float. Two years later, the company’s shares were 71% down – with short sellers betting they could fall yet lower.

In the case of Adani, one variable now is the FPO. If it goes through, it will improve the group’s debt-equity numbers – and give lenders greater comfort. Much also depends on when existing bonds come up for redemption. At that time, the group will have to refinance them.

The group has to regain the global bond market’s confidence or look for alternatives. More domestic borrowings is one possibility but, as The Morning Context reported, there is not much interest among domestic institutions. The group could also consider tapping sovereign funds. It isn’t clear, however, if those can entirely replace the global bond market.

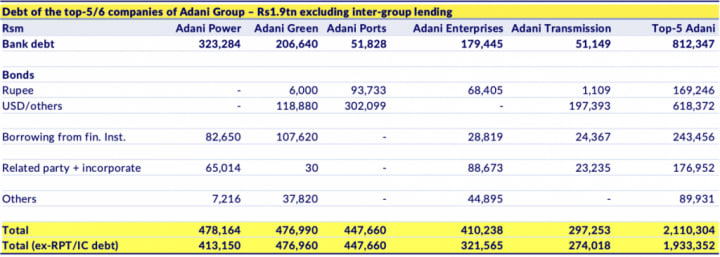

If bond prices fall steeply, the group could also consider re-acquiring them but that is unlikely. Adani group’s total gross debt last year stood at Rs 2.2 lakh crore. With half of this coming from overseas bonds, that is Rs 1.1 lakh crore. Not an easy sum to raise while running the group as well.

Inspired by TheWire Article,

About the Creator

Satz

Tragedic Interesting Stories

Sabotage

Lately I’ve been in a funk where everything can be going right. You know I’m in a happy place talking to who knows, I’m at peace and feel like everything is just going great you know. But once I start seeing that everything is going great for some reason I need to sabotage it. I need to sabotage my happiness and what I have going on in my life so no one else is able to do it for me. Does that make sense? Am I the only one who gets this way?

By Merjaunie Lena10 days ago in Journal

Shining Souls Trust: Illuminating Paths to Education Equality in India

In a diverse society like India, access to quality education is an essential foundation for bridging socio-economic gaps and promoting equitable opportunities. One organization that stands out in this pursuit is the Shining Souls Trust, the best NGO in India, located in the heart of Delhi.

By Shining Souls Trust | Best NGO in India7 days ago in Journal

The Business of Nature

Dew drops reflected the light of the sun. The inhabitants of Whispering Woods woke up to the golden droplets of water on the leaves of the flora. The oaks particularly enjoyed the light and the maples did, too. Happiness enveloped all who lived there, even the rocks that cried out in the night delighted in the morning.

By Skyler Saundersa day ago in Fiction

Comments

There are no comments for this story

Be the first to respond and start the conversation.