5 easy steps for Financial independence

The steps are before us, we must know which ones we choose

Financial independence can be defined as the state in which personal wealth generates enough passive income to cover the needs of an individual’s lifestyle, without him having to work actively.

As can be seen from the definition, the key terms are personal wealth and passive income. Your financial goals, if you want financial independence, should be related to increasing your wealth in the first place and investing in passive income assets in the second place.

Basic principle: Increase net assets (net wealth) every year;

The Mistake Most Make: Increasing Net Liabilities Year by Year — Accumulating Debt and Depriving Goods (Cars, Holiday Homes, Consumer Loans)

The steps below represent the strategy behind our goal, financial independence, and the backbone of our entire money management system. It is important to start with a good strategy so that you do not take the wrong path and do not waste precious time and effort.

Remember, the road to financial independence is a marathon, not a sprint.

Here are the 5 strategic steps:

1. Earn more active income

Basic principle: Maximize active income by acting congruently on the 3 elements of the active income equation.

Mistake Most People Make: They fail to maximize their asset income and are content with relatively constant or possibly year-on-year indexed inflation.

Your active earnings = The value you bring to people X The number of people you serve X Your ability to sell your goods and services

It acts on the increase of the 3 elements of the equation:

- The value you bring to people is your ability to solve problems or improve the lives of others. The more others need or want more than you can offer, the more value you can bring them. It is important to remember that the value you bring is determined by others, by the price they are willing to pay for your services. Thus, the service you offer must be wanted and sought after. Once the field in which you work is chosen well, you can bring more value through practice/experience, study, courses, accreditations, etc. It is important to be better and better in your field. Sharpen the saw continuously.

- The number of people you serve represents the environment in which you provide your services. For example, if you are employed, you will earn much more working for a large company with hundreds of employees than doing the same work for a company with 10 employees. Also, if you are an entrepreneur, you will earn much more if you expand nationally, compared to if your business operates only locally, in a small town of 50,000 inhabitants.

- Ability to sell — the price of your services, the way you manage to negotiate the salary, prices, rates, etc. You can be as good at what you do and serve as many people as you can, if you can’t sell your services at a fair price, then you won’t increase your income. I guarantee that no one will come to you to tell you what a good professional you are and what impact you have on millions of people and to put more money in your pocket. No, that’s your job, you have to ask for better pay.

2. Decreases / maintains expenses at the current level

Basic principle: Expenditure to be below the possibilities

The mistake most people make is spending money

Some people are experts in increasing income but lose all the advantages created by excessive spending. If you make a million euros and spend a million euros then you are poorly attached to the earth.

On the other hand, there is a current that is starting to catch on in our country as well, that of a frugal life, excessive care for every penny, and of abstaining from many of the pleasures of life. I am not a fan of this current, I am in control of expenses but not excessive. I think we should use our attention and energy to make more money than to save a lion and a lion.

So I do not support excessive frugality but I support balance and for me, a balanced approach is one in which you live below the possibilities, that is, you spend less than you earn. For more efficient management of expenses, I recommend you use a personal budget.

Expenses are divided into:

- Savings. I suggest you start with at least 10%;

- Mandatory fixed expenses (rent, utilities, subscriptions); They are reduced as much as possible without affecting the standard of living

- Mandatory variable expenses (food, clothes, household items, fuel, etc.); Waste is eliminated. They are seen as investing — you need them to work

- Expenses are born of desires, not of necessities (free time, vacations, vices, amusements, small pleasures, clothes over what would normally be necessary, etc.); It can be greatly reduced here. The more balanced a person is, the less he will spend on vices, strong sensations, small daily pleasures, excess clothes, etc.

- Investments in one’s person; In general, education but also healthier eating, sports, and everything else makes you more productive. Here you can also include donations.

My advice is to try to maintain your current spending level at each increase or at least increase it by at most 50% of your income increase. In this way, you will be able to progressively increase the level of saving, without feeling that your standard of living is affected. And so we move on to point 3.

3. Save more

Basic principle: It doesn’t matter how much you earn but how much you save

The mistake most people make is paying attention to their income

This is the amount that matters, because it adds to your net assets. The amount saved by you is the equivalent of the profit obtained by a company. If you do not save it means that you are not profitable and you are bankrupt, regardless of your turnover (how much you earn).

The goal is that as your income grows, your expenses will remain relatively constant, or grow at a much slower pace so that your savings will grow as a percentage of your total income from 10% to 20–30–40–50- 60%, etc. Wealthy people set aside over 80% of their income and spend the remaining 10–20%. And they live like kings with the 10–20%.

If you applied step 1 to increase revenue and step 2 to limit spending, step 3 comes naturally.

Saving is a habit and should be kept active for the rest of your life.

I recommend you to save in the cascade, moving to the next fund, as soon as you have filled the previous one:

- Emergency fund: an amount of money equivalent to 6 X basic monthly expenses — the foundation of your wealth that you do not touch. This money is intended only for emergencies (loss of income, serious health problems, etc.) and not for weddings, baptisms, holidays, or new furniture. If it is consumed, its replenishment becomes priority no. 1.

- Fund for large acquisitions: this fund is specially created for certain large but necessary acquisitions such as the advance for the house or the purchase of a car. As long as the house you buy and the car are below your means (meaning you would afford something much more expensive if you wanted) then you do not risk getting stuck at this level.

- Fund for financial independence: this is the fund for investments and the one that will constitute the bulk of your wealth when you achieve financial independence.

4. Invest in assets that generate passive income or will be valued

Basic principle: Investing savings in assets that generate passive income or will be valued.

The mistake that can easily get your claim denied is to fail.

Asset — Tangible or intangible asset that generates passive income or will be valued as value (houses, land, shares, bonds, intellectual property rights)

Passive income — income for which you work only once to create/acquire it and which subsequently generates income without requiring your intervention (or only a limited intervention);

Once some money has been raised in the Financial Independence Fund, we can think of investing it to generate passive income. We know that we are ready mentally, emotionally, and financially to start investing when we meet the conditions here.

Examples of assets that generate passive income:

- Apartments and houses for rent;

- Agricultural land that can be rented;

- Dividend-paying shares;

- Bank deposits;

- Bonds;

- Intellectual property rights; books, music, software, etc.

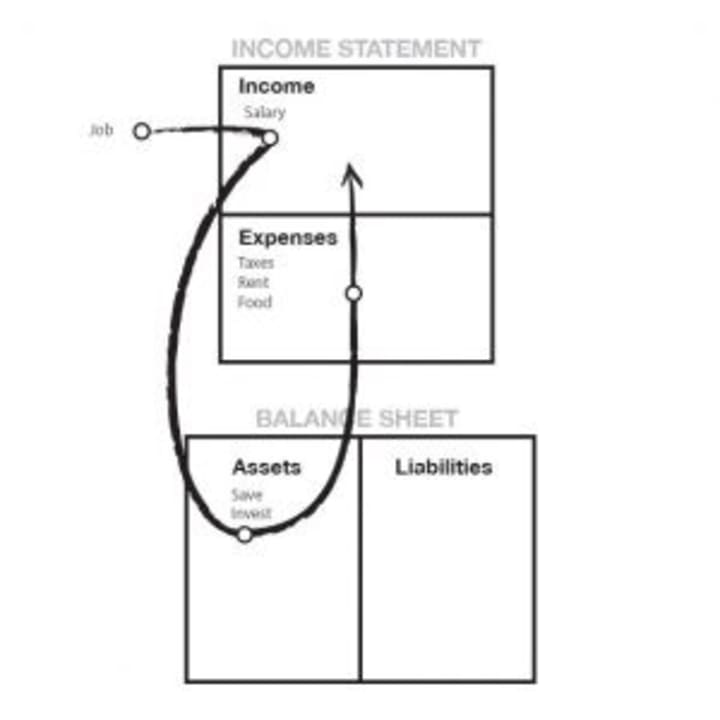

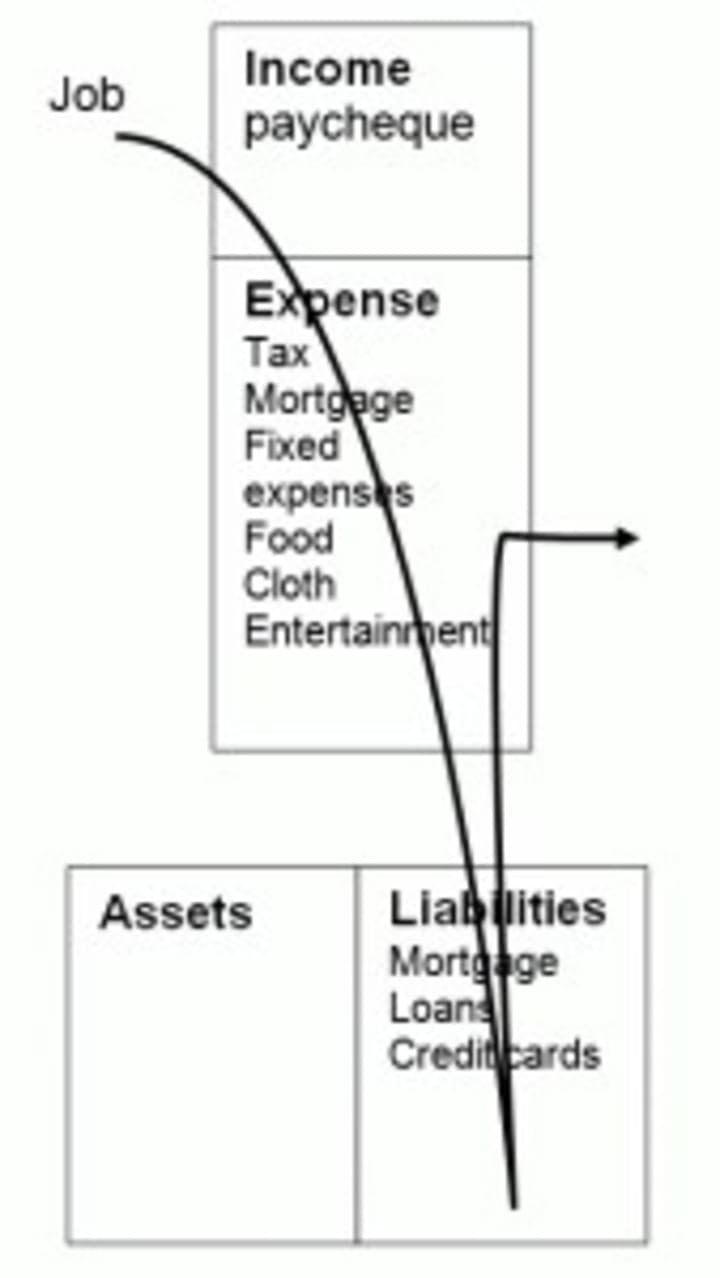

Scheme of wealth and lack thereof:

The virtuous circle: Income -> Savings -> Assets -> Passive Income

The vicious circle: Income -> Expenses -> Liabilities -> Expenses

The virtuous circle

The vicious circle

This step is the hardest and requires the greatest effort of education, discipline, and patience. Investments also involve risks, so you can lose. On the other hand, if you don’t invest, you lose from the beginning, because the bank interest rate will cover the inflation at most and maybe not even that much.

For English speakers, I also recommend the following article in which Sam, the author of the blog, teaches us the strategic basics of creating Passive Income Framework.

The mistake that can easily get your claim denied is to fail. True investors take calculated and asymmetrical risks for the reward. In other words, when investing, it is ensured that the potential and probability of gain are greater than the potential and probability of loss.

The most efficient investments for an individual investor on the road to financial independence are passive, constant investments, month by month. This strategy maximizes your chances of success in the long run and requires the lowest level of knowledge and time spent. You can find the basics in Tony Robbins’ book Money: Master the game.

5. Reinvest the earnings from the Financial Independence Fund

Basic principle: Reinvest all passive income to benefit from the power of compound interest.

The Mistake Most Make: They use passive income as an additional source of income to cover current expenses before they become financially independent.

The profits from your investments are reinvested in the same Fund for financial independence, along with the monthly amounts saved from your active income. Thus, your savings + your passive income will be constantly reinvested, month by month, to obtain an increasing passive income.

In this way, you take full advantage of the power of compound interest, through which you get interested in interest.

By following steps 1 to 5 consistently, you will surely end up in a situation where at some point your passive income will exceed your active income.

If the passive income exceeds the basic monthly expenses then you have reached financial independence.

Conclusion

The 5 steps are circular, you always have to go back to step 1 to increase income, then step 2 to control expenses, save, invest, reinvest profit, and then again and again until you reach the desired goal.

The strategy is very important and must be outlined and mastered from the beginning. The implementation of the strategy requires clear, coherent, concrete, and constant actions spread over several years. These are the tactical elements of the strategy, and how we achieve each of the 5 points.

It is important to remember that the strategic approach is the only safe approach that leads to financial independence. Stop looking for quick and chaotic ways to get rich, all you have to do is waste your time, money, and energy in vain.

There will be articles in which I will present techniques and concrete ways for each of the 5 steps in achieving financial independence.

Until then, increase your money!

Read too:

About the Creator

Keep reading

More stories from Cosmin Child and writers in Journal and other communities.

10 Principles for Stock Market Investments

Howdy, Lately, I have been asked more and more often if this is a good time to invest in the stock market. My classic answer to this question is that the best time was: yesterday (when there was a crisis and everyone was desperate).

By Cosmin Child2 years ago in Journal

Comments

There are no comments for this story

Be the first to respond and start the conversation.