Understanding U.S. M2 Money Supply

Debunking Doomsday Predictions and the Fed's Tightening Strategy

Recently, there has been a strong buzz surrounding the contraction of the M2 money supply year over year, raising concerns and fueling speculation about impending economic doom. During my in-person presentations, I have received questions regarding the implications of this decline. However, a closer examination reveals a more nuanced picture dispelling this alarmist rhetoric.

At present, the M2 money supply is indeed contracting by -1.1% annually. Yet many doomsday predictors invading the electronic feeds of our readers and audience members (at my recent client presentations) fail to acknowledge the broader context of examining the entire path of this closely-watched monetary aggregate!

Yearly Growth in M2-Money Supply

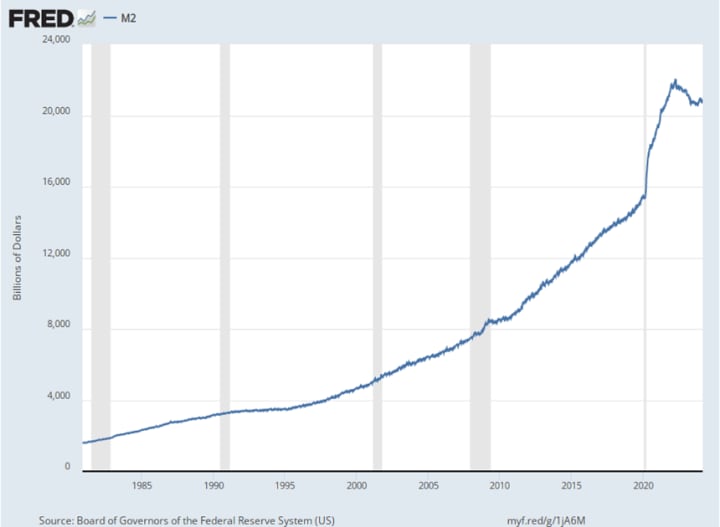

Within a broader context, the M2 money supply has surged by a staggering 35 percent from its pre-global pandemic levels. This significant increase underscores central banks' extraordinary measures to stabilize the U.S. economy and reduce some of its inflationary pressures. So far, they are making progress, as the yearly growth in the Consumer Price Index has dropped from a peak of 9.1% to 3.2%. This is a deep-rooted challenge, no doubt!

M2-Money Supply Levels

The Federal Reserve has pursued a quantitative tightening (QT) strategy to reduce its Treasury and mortgage-backed securities holdings. This deliberate unwinding of its balance sheet has already resulted in the removal of several trillion dollars at a monthly reduction pace of $90 billion. While this strategy contributes to M2's contraction, it's crucial to recognize that such measures are necessary to restore a semblance of normalcy to the financial system.

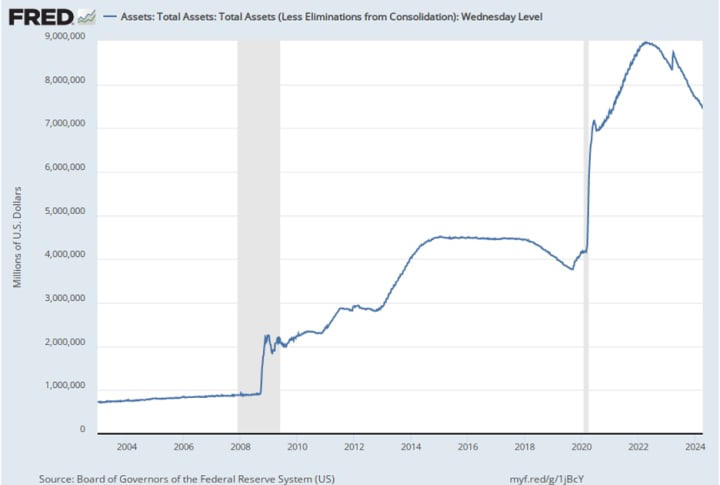

If anyone is still worried about the fall in liquidity, M2 or otherwise, think again! The Federal Reserve’s balance sheet rose from $4.1 trillion in Feb. 2020 to $9.0 trillion in April 2022. It is down to $7.4 trillion in its latest reading but still up an outsized 80.4% from its pre-pandemic levels! And let us not forget that the Fed has started discussing the possibility of slowing the pace of contracting (aka QT) its balance sheet despite the excess amount of M2 and balance sheet assets that it has amassed since the global pandemic hit the United States!

Federal Reserve Balance Sheet

Still, returning M2 growth to a sustainable level is a gradual process. According to conventional wisdom, M2 should expand at a rate commensurate with potential economic growth plus the inflation target growth, which equates to approximately 3.8% per year—a far cry from the excessive post-pandemic growth.

Indeed, the unprecedented surge in the M2 money supply has fueled concerns about inflationary pressures. Excessive liquidity in the financial system can raise demand, increase prices, and erode purchasing power. Thus, mitigating these inflationary risks requires bringing M2 growth back to a more moderate trajectory.

Nevertheless, it's essential to acknowledge the complex relationship between money growth and economic activity. The traditional correlation between M2 and GDP growth has sometimes failed to hold up perfectly. Myriad factors influence economic dynamics, and the mechanical relationship between money supply and economic output needs to be more precise.

Amidst the fluctuations and uncertainties, it's crucial to maintain perspective. While the recent dip into negative territory for M2 yearly growth is noteworthy, it does not warrant panic. Instead, it reminds us of the need for prudent monetary policy and vigilant economic management.

Moving forward, policymakers must navigate a delicate balance between stimulating economic recovery and safeguarding against inflationary pressures. The gradual normalization of M2 growth, coupled with targeted interventions where necessary, will be instrumental in achieving this equilibrium.

Moreover, the Federal Reserve's commitment to transparency and data-driven decision-making offers reassurance in uncertain times. While challenges remain, the central bank's steadfast approach to monetary policy instills confidence in the economy's resilience.

Summary and Concluding Thoughts

The year-over-year contraction of the M2 money supply has sparked concerns and debates. However, a closer examination reveals a more nuanced reality. The surge in the M2 money supply post-pandemic necessitates a measured approach to normalization guided by economic fundamentals and prudent policymaking. Rather than succumbing to alarmist narratives, it's imperative to maintain perspective and look at the entire path of M2-money supply, the Fed’s balance sheet, and the amount of QT the Fed uses to reduce liquidity from the levels observed before the global pandemic. Looking at liquidity using this holistic approach, we can see that the economy still has excessive liquidity that needs to be slowly extinguished to help the Federal Reserve attain its 2.0% inflation target!

About the Creator

Anthony Chan

Chan Economics LLC, Public Speaker

Chief Global Economist & Public Speaker JPM Chase ('94-'19).

Senior Economist Barclays ('91-'94)

Economist, NY Federal Reserve ('89-'91)

Econ. Prof. (Univ. of Dayton, '86-'89)

Ph.D. Economics

Keep reading

More stories from Anthony Chan and writers in FYI and other communities.

Is the U.S. Economy Experiencing Stagflation?

While some market observers have begun to warn about the risks of stagflation, others have started to ask if we are already there. At a recent in-person presentation I delivered on the West Coast, one participant asked me if I thought we were suffering from stagflation because more people were starting to worry that it was a real risk factor for the U.S. economy.

By Anthony Chan30 days ago in FYI

One of the Crazy Things Rich People Do That's Scary To Think About

They impress us, and sometimes they scare us, but the ultra-rich are always interesting. Some of their famous activities include buying yachts too big to move through channels, buying ridiculously priced cars that could feed the homeless of New York for weeks, and their expensive tastes in sex workers.

By Jason Ray Morton 3 days ago in FYI

A Glimpse into Tomorrow: The World After Fifty Years

In the vast expanse of time, fifty years may seem like a mere blink of an eye, yet within its grasp lie the seeds of transformation, waiting to bloom into the world of tomorrow. As we embark on a journey into the unknown, let us dare to imagine the possibilities, painting a canvas of hope and innovation as we glimpse into the world after fifty years.

By WILLIAM DIAGO RODRIGUES7 days ago in FYI

Turning Pages of Life

Life’s like a book — some parts are good, others not so much. Still, keep turning the pages; you might find the best chapter next. If someone hurts you, choose to forgive or just let it be, but never change who you are for them.

By Emily Chan - Life and love sharing4 days ago in Poets

Comments

There are no comments for this story

Be the first to respond and start the conversation.