How an economic warning was issued as signs of fraud emerged

Uncovering the Hidden Economic Warning Signals through Accounting Fraud Detection

The economy faces a dark omen as corporate America experiences an increase in earnings manipulation.

Recent research on accounting fraud has concluded that a particular technique, which had previously identified Enron's earnings manipulation years before their downfall in 2001, can effectively detect such fraudulent activities.

The M-Score, a tool used to identify manipulation in a company's financial statements, has gained attention due to its association with Enron and current concerns about the economy. However, unless you're an accounting student, you may not be familiar with it. The "M" in M-Score stands for manipulation.

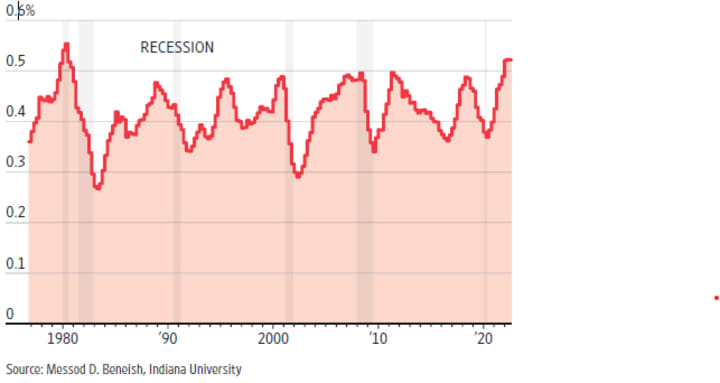

The M-Score, which has been utilized since the 1990s to detect warning signals in individual companies, has now been used by Messod D. Beneish, an accounting professor at Indiana University, and a team of researchers to generate an aggregate score for almost 2,000 companies. The historical data indicates an alarming trend: the likelihood of manipulation tends to increase significantly in the quarters preceding an economic downturn.

According to Dr. Beneish, the latest aggregate measure developed to detect manipulation in the economy represents the prevalence of false information. The research was published in December, and the latest data, collected in March and shared with The Wall Street Journal, reveals that the probability of fraud in major companies is at its highest level in more than four decades.

To calculate the M-Score, eight ratios found on a company's balance sheet, all of which are reported quarterly by public companies, are compared to the previous year's earnings statements.

One of the eight metrics used in calculating the M-Score is triggered when a company begins reporting a sudden increase in "receivables," which is the amount of money owed to the company but not yet paid. Another metric raises a red flag when a company reports higher values of assets that are not categorized as property, equipment, or plants, and cannot be sold. The third metric examines changes in accruals, which occur when an expense has been incurred but not yet paid. The fourth metric identifies changes in the amount of depreciation that companies take.

Companies have the ability to manipulate these metrics to create the appearance of profitability, even if actual sales figures do not improve.

It's important to note that there may be valid reasons for changes in these metrics. For instance, a customer could place a large order near the end of the quarter but not pay until the next quarter. Similarly, a drug company might have bought a new machine that increased the value of their assets. However, the M-Score indicates that accounting fraud is becoming more prevalent, which is a pattern that has often preceded a recession. This metric measures whether companies are manipulating their financial statements.

The M-Score gained notoriety when a group of students at Cornell University's business school, led by accounting professor Charles Lee, used Dr. Beneish's model to identify Enron as a potential earnings manipulator three years before its downfall. Although the report was posted online, it received scant attention until after Enron's collapse.

Wirecard AG, a German payment-processor, was also identified by the M-Score model for accounting fraud, which led to its high-profile collapse in 2020 and drew parallels with Enron.

According to Dr. Lee, a rise in any of the eight metrics on its own may not necessarily indicate a problem. However, an increase in the combined score of the metrics suggests a company that is experiencing a decline in its core businesses and is using aggressive accounting practices to compensate for this. Dr. Lee advises that investors should avoid such companies, even if their accounting practices are legitimate.

Accounting scores similar to the M-Score have been widely used since the late 1960s. For example, the Altman Z-score, developed by Edward Altman in 1968, predicts a company's risk of bankruptcy, while the Dechow F-Score, created by Patricia Dechow of the University of Southern California, aims to identify accounting misstatements.

While models like the M-Score may not always be conclusive evidence of wrongdoing, they can occasionally identify valid business operations, particularly in cases involving mergers and acquisitions. When companies merge, unusual changes can arise. However, these models are still a compelling reason to investigate further.

Dr. Lee explained that an M-Score alone cannot be used as conclusive evidence to prove fraud in a court of law. However, statistically, a company with a high M-Score matches the profile of a company that may be manipulating its financial statements.

When multiple companies start showing signs of incomplete sales, poor asset quality, or other negative indicators, it could suggest that there are underlying issues in the economy.

Currently, the economy shows signs of stress such as interest rates increase by the Federal Reserve, collapse of some well-known banks, sluggish manufacturing activity, and declining home prices. Nevertheless, it is reasonable to consider that the M-Score may provide additional insight beyond the conventional metrics used to evaluate economic activity.

According to Dr. Beneish and his co-authors, misinformation on balance sheets can have significant economic consequences, as it can influence a company's investment, hiring, and production decisions. They wrote about this in December, and their co-authors include David Farber of Indiana University-Purdue University in Indianapolis, Matthew Glendening, and Kenneth Shaw, both from the University of Missouri.

The idea behind the index is that it could be identifying early signs of distress when some companies attempt to mask it. This happens when economic conditions are starting to worsen, but firms are still showing impressive earnings. As a result, the stock market may appear to be doing well when in fact, company profits are increasingly being propped up by fraudulent methods.

The aggregate index developed by the scholars is too recent to have established a track record. Many predictors of recessions have been successful when based on historical data, but have failed when attempting to predict the future. In other words, they didn't work "out of sample," as statisticians put it. Thus, it remains uncertain how valuable the aggregate M-Score will turn out to be.

A high number of items on balance sheets that appear to be fraudulent may indicate a negative situation.

About the Creator

Bob Oliver

Bob is a versatile writer & communicator passionate about exploring diverse topics & perspectives. I have written for various media outlets. And I believes in using words to inspire positive change. #writing #communication #passion

Keep reading

More stories from Bob Oliver and writers in Education and other communities.

The development of the special festival

By and large, Christmas is the main occasion of the year. However that is generally a mishap, originating from a progression of far-fetched changes spreading over two centuries. A comparative arrangement of changes has impacted the improvement of other occasional occasions, similar to Hanukkah.

By Bob Oliver2 years ago in Families

Coffee Drink

Coffee, the dark elixir that fuels mornings, midday slumps, and late-night study sessions, holds a revered place in cultures worldwide. From the bustling streets of Italy to the serene coffee plantations of Colombia, its aroma and taste captivate millions daily. In this exploration, we delve into the rich history, cultivation, processing, brewing methods, health effects, and cultural significance of coffee.

By Mithun Gain6 days ago in Education

Comments

There are no comments for this story

Be the first to respond and start the conversation.