What's a Robo-Advisor?

If you’re a young professional starting out in the investment world or are planning for retirement, a robo-advisor can help you to reach your financial goals.

Financial planning can be one of the most difficult strategies to perfect in our lives. Every day, people spend thousands of dollars on financial advisers and planners to ensure that their money is invested in a safe place. However, in today’s modern age, there is now online software that can handle all of this for you, and for a low cost.

Robo-advisors have been in use since 2008, following the Great Recession. The launch of Betterment changed the game for financial planning and investing long-term. Initially, its purpose was to rebalance assets through simple online interface.

Over the years, robo-advisors have developed into a greater, more user-friendly software. Now, in 2018, these online advisors have the ability to handle tax-loss harvesting, investment options and strategies, and retirement planning. In the United States alone, there are over 200 robo-advisors and counting who can assist you with day-to-day investing and financial planning, making your financial goals a reality.

How does it work?

Photo via Investor Junkie

A robo-advisor is an algorithm-driven online software that helps you manage investments and finances, replacing the need for a financial planner. They are a great tool to use for financial advising and portfolio management, and work with no human interaction.

When first registering with a robo-advisor, your first interaction will most likely be a questionnaire. Filling this out helps the interface asses your risk tolerance, financial goals, and investing preferences. Depending on your assets, you will receive a portfolio ranging anywhere from conservative to aggressive. You can choose to veto this portfolio or keep it. The types of accounts that a robo-advisor can manage are retirement accounts, taxable accounts, trust accounts, and even your 401k.

Robo-advisors invest your funds and continuously make changes to your portfolio, depending on your financial goals. In most cases, they will even perform tax-loss harvesting, essentially meaning that they automatically make trades that reduce tax bills.

What investments are used?

Photo via FITniancials

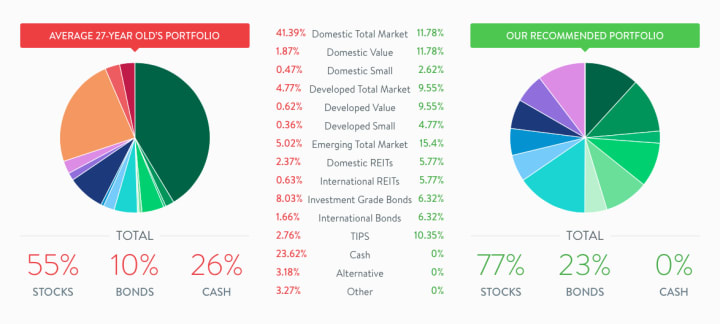

It is important to note that most robo-advisors use mutual funds to build a portfolio. They have an algorithm in which they follow an index fund (otherwise known as a passive investment approach) that is based on modern portfolio theory research.

To break it down, using an index fund focuses largely on your asset allocation to stocks or bonds. It then scopes in on underlying stock asset classes (large cap, small cap, international). Even further, it will then focus on bond asset classes (short, intermediate, long term). If this jargon is beyond you, then no need to worry because robo-advisors can guide you through it.

Benefits

Photo via personalincome.org

There are many reasons why you should use a robo-advisor. They are great for beginners who are just starting out in the investment world or those looking to start retirement planning because there is little to no room for failure. You can track your funds and choose an automatic process in which the robo-advisor does everything for you.

1. Avoid mistakes

One of the larger benefits of using a robo-advisor is that it is cost-efficient. Usually, investors make moves based off of emotion, resulting in a loss of money and poor outcomes. Since robots do not carry emotion, they make more logical decisions based on algorithms, avoiding costly investing mistakes and reducing stress.

2. User-friendly

Robo-advisors are also a low-cost alternative because they eliminate any human interaction. They are more accessible and available online 24/7. One quality that investors tend to admire about robo-advisors is its user-friendly software and efficiency. At the click of a button, you can execute a trade rather than waiting to meet with a financial advisor and filing paper work. It can be done within five minutes.

3. Anyone can use it safely

Most importantly, anyone can use robo-advisors. Students, retirees, young professionals, and anyone interested in stock and investing can use this software. In addition, it is extremely safe to use. Many people worry about putting too much of their information online, but it is a safe bet with robo-advisors. Any robo-advisor must register with the U.S. Securities and Exchange Commission and are therefore subject to the same laws and regulations as broker-dealers. They are insured and safe, what more do you need?

Cost

Photo via Pixabay

The only out-of-pocket pay that you need to be aware of is the robo-advisor management service fee and the expenses of the investments. Many companies charge between 0.25% and 0.89% as an annual management fee, which can be paid as a percentage of your assets. If you choose not to pay with your assets, then you have the option of paying a monthly fee that can be anywhere from $15-$200 per month.

Most of the time, when you use a financial advisor, you can spend hundreds of thousands of dollars in minimum assets. However, there are some robo-advisors who have an account minimum of zero, making it simple and affordable for anyone to use. For example, Betterment has no account minimum at all.

You also pay no taxes until you withdraw. Depending on how largely you withdraw, that will affect your taxation. The reasoning behind this is that robo accounts are funded with cash, you avoid interests, dividends, and capital gains. Before you commit, see if any robo-advisors offer a free trial period.

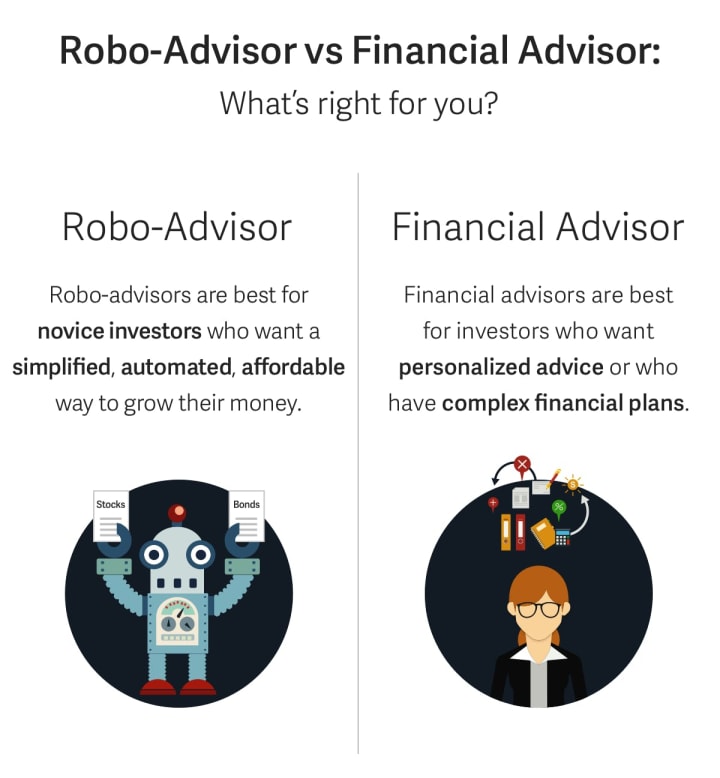

Why a robo-advisor and not a financial advisor?

Photo via Policygenius

The differences between a robo-advisor and a financial planner are significant. Other than the fact that robo-advisors are not human, they provide many software tools that can project growth in your accounts. The main difference between using a robo-advisor and human advisor is that you will not receive planning advice such as how to save, how much to save, and how to allocate investments in other accounts.

Hiring a robo-advisor is a great alternative for those who wish not to use a financial advisor, or for someone who is tired of investing themselves. It is a useful took for beginners and can help you to achieve your financial goals. They are low cost and it can teach you how to invest, while also avoiding failure.

Some robo-advisors even offer live assistance, for an additional cost, which is all done over the web. No need to set up meeting, make calls, or file paper work. Robo-advisors are the future and they can assist you with all of your investment needs. Companies such as Charles Schwab, Personal Capital, and Wealth Front are all companies that offer robo-advisors. If you haven’t already, I would highly suggest giving it a try.

About the Creator

Patty Ramsen

Just another 20 something trying to break the glass ceiling one blazer at a time. Get your own coffee...

Keep reading

More stories from Patty Ramsen and writers in Trader and other communities.

Long Term Investment Options and Strategies

Determining which long term investment options and strategies are right for you can feel completely overwhelming. With markets rallying fiercely at one moment and in a state of utter freefall the next, knowing where to put your money can seem like an impossible task. Fortunately, the sheer number of different types of investments means that you can tailor a strategy that works perfectly for you.

By Patty Ramsen6 years ago in Trader

"Stride in Style: Discover the ALDO Men's Albeck Oxford"

In the realm of men's footwear, finding the perfect balance between style, comfort, and versatility can often feel like an elusive quest. Yet, amidst the sea of options, there emerges a beacon of excellence that embodies these qualities seamless: the ALDO Men's Albeck Oxford. As a distinguished member of ALDO's esteemed lineup, the Albeck Oxford stands as a testament to the brand's commitment to crafting footwear that not only exudes sophistication but also delivers unparalleled comfort and durability.

By Kim Long Nguyệt Ngữ4 days ago in Trader

2023 Fashion Designer Shoes Men Casual Platform Sneakes Lace Up Trainers Student Sneakes Mens Vulcanized Shoes Zapatillas Hombre

In the ever-evolving world of fashion, footwear has become more than just a functional accessory; it's a statement of style, personality, and individuality. One of the most intriguing trends to emerge in recent years is the fusion of casual comfort with elevated design, epitomized by the rise of platform sneakers for men. These shoes seamlessly blend streetwear flair with high-fashion sensibilities, creating a versatile option that can effortlessly transition from day to night, casual to formal.

By Wedson Vegasa day ago in Trader

Comments

There are no comments for this story

Be the first to respond and start the conversation.