I’m sure we’ve heard stories of people owing 10s, 100s, and 1000s of dollars in loans.

On the table, we find love letters from banks.

Or worse, the house is splashed with red paint.

IOU (I Owe Yous), Hutang, or Debt is a common issue that affects many individuals and families around the world.

However, with the right strategies, it’s possible to manage and pay off debt successfully.

In this story, we will cover, what is debt, types of debt, importance of managing debt, various debt management strategies, and tips to stay debt free that can help you get out of debt and improve your financial situation.

What Is Debt?

Debt is a sum of money borrowed by an individual or entity that must be repaid over time with interest. Debt can be in various forms: credit cards, loans, or mortgages.

Types Of Debt

The book, Rich Dad Poor Dad, taught me a lot about debts.

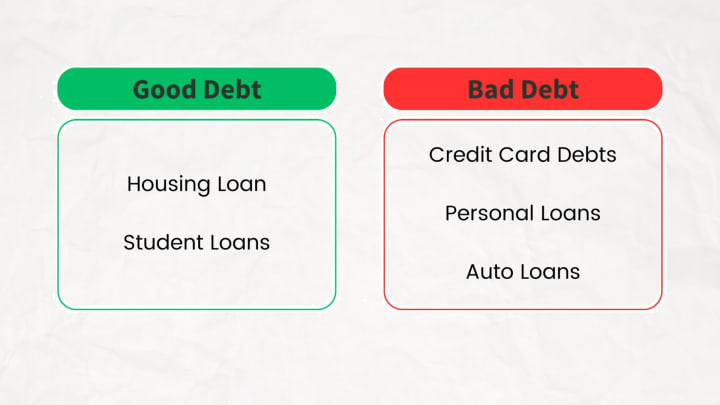

Debts can be morally categorized into Good Debt and Bad Debt.

Then, while there are good and bad debts. There are several types of debt.

- Credit card debt: Debt that is accumulated through the use of credit cards and other revolving lines of credit. Credit card interest rates in Malaysia can be relatively high, ranging from around 15% to 18% or even higher.

- Student loans: Loans that are taken out to pay for educational expenses, such as college and university tuition. Interest rates can range from 4% to 6% or more. An example of student loan in Malaysia is PTPTN.

- Mortgages or housing loans: Loans that are taken out to purchase a property. There are fixed rate and variable rate loans. So far, interest rates averaged about 4% +/-.

- Personal loans: Loans that are taken out for personal use. Normally people take out personal loans for home renovations or medical expenses. Personal loan interest rates can range from 4% to 10% or more.

- Auto loans or car loans or hire purchase loans in Malaysia: Loans that are taken out to purchase a vehicle. Interest rates can range from 3% to 5% or higher.

Examples of good debt are housing loans and student loans (some might disagree with this). Then examples of bad debts are credit card debts, personal loans, and auto loans.

The Importance Of Managing Debt

So managing debt is crucial for several reasons:

- Reducing financial stress and anxiety

- Improving credit scores

- Avoiding late fees and penalties

- Saving money on interest charges

- Achieving financial goals, such as buying a home or starting a business

Debt Management Strategies

Now that we know what is debt and the importance of managing it; here are six strategies to manage debt.

1. Create A Budget

It is an essential first step to manage your debt.

List all of your income and expenses, including debt payments.

By tracking your spending, you can identify areas where you can cut back and allocate more money toward debt repayment.

2. Set Financial Goals

This involves identifying your long-term financial objectives, such as paying off all debt or saving for a down payment on a home.

By setting specific goals, you can create a plan that will help you achieve them.

3. Prioritise Debt Repayment

This involves deciding which debts to pay off first.

There are two main approaches to debt repayment: the debt snowball approach and the debt avalanche approach.

The debt snowball approach involves paying off the smallest debt first and then using the extra money to pay off the next smallest debt.

The debt avalanche approach involves paying off the debt with the highest interest rate first and then moving on to the next highest interest rate debt.

4. Negotiate With Creditors

I know it can be scary and daunting to negotiate with creditors – ah longs.

Negotiating with creditors can be a useful strategy for managing debt. It involves contacting your creditors and asking for a lower interest rate or a payment plan that fits your budget. While not all creditors will be willing to negotiate, it’s worth trying as it can potentially save you money in the long run.

5. Consolidate Debt

This involves combining multiple debts into one loan with a lower interest rate. This can make debt repayment more manageable by reducing the number of payments and interest charges.

There are several options for consolidating debt, such as balance transfer credit cards, personal loans, or refinancing home loans. However, it’s important to carefully consider the terms and fees associated with debt consolidation before choosing this option.

6. Seek Professional Help

If you’re struggling with debt and feel overwhelmed, seeking professional help may be a good option. There are several resources available, such as credit counseling agencies or debt management companies, that can provide guidance and support in managing debt. However, it’s important to research these options carefully and choose a reputable organization.

In Malaysia, we’ve AKPK – Agensi Kaunseling and Pengurusan Kredit. In English, it is Credit Counseling and Debt Management Agency.

AKPK is a Malaysian government agency established to provide financial education, credit counseling, and debt management services to individuals facing financial difficulties.

Tips To Stay Debt-Free

Once you’ve successfully managed and paid off your debt, it’s important to develop habits that will help you stay debt-free in the future.

Here are some tips for staying debt-free:

- Continue to track your spending and create a budget

- Avoid unnecessary expenses and impulse purchases

- Save for emergencies and unexpected expenses

- Use credit cards responsibly and pay off balances in full each month

- Invest in education and financial literacy to make informed decisions about money

Conclusion

So, managing and paying off debt can be a challenging process, but with the right strategies, it’s possible to achieve financial freedom.

By creating a budget, setting financial goals, prioritizing debt repayment, negotiating with creditors, consolidating debt, and seeking professional help when necessary, you can successfully manage and pay off your debt.

Additionally, developing habits for staying debt-free can help you maintain a healthy financial situation in the future.

About the Creator

Ian Fan

Going by the handles @foodyfans and @ipropfans, Ian shares about real estate, investing, finance, travel, food, and personal growth.

Follow Ian Fan on YouTube, Instagram (food), Instagram (property), X, Facebook, Blog, and Medium.

The best refrigerators to buy dice now!

In our modern homes, refrigerators are more than just appliances. They have become the guardians of our food, ensuring its freshness and safety. Over the decades, these devices have undergone remarkable evolution, both in terms of functionality and design, to meet the changing needs of consumers and technological advances. Today, we are witnessing the emergence of innovative refrigerators, such as the «GEDTECH High Freezer Refrigerator - GE217DPSL Silver - capacity 217L - Class E [Energy Class E]» offering generous capacity and optimized energy efficiency, the “CHIQ CBM159LEBD Low Frost 157 Litre (109 + 48) Freezer Refrigerator, Low Noise, Fast Cooling, Small Footprint. [Energy Class D]”, which stands out for its low noise level and small footprint, as well as the «FRIGELUX Fridge freezer low RC168BE» combining simplicity and performance. These examples illustrate the diversity and innovation that characterizes the refrigerator market today, while highlighting the growing emphasis on energy efficiency and practicality. In this article, we will explore the evolution, different typologies, recent innovations and environmental issues of refrigerators, while taking a look at the future of this essential technology in our homes

By Alicia Lhotellier6 days ago in Trader

Integrated marketing

Integrated Marketing Dispatches( IMC) is a strategic approach that ensures all marketing dispatches are cohesive, harmonious, and work together to support a brand's communication across colorful channels. In moment's dynamic and connected business, where consumers are bombarded with information from multiple sources, IMC has come essential for companies to effectively reach their target followership and achieve their marketing objects. At its core, IMC involves the integration of colorful communication tools, similar as advertising, public relations, direct marketing, deals creation, and digital marketing, to deliver a unified communication to consumers. By coordinating these rudiments, companies can produce a flawless brand experience that resonates with consumers and drives engagement and fidelity. One of the crucial benefits of IMC is that it allows companies to maximize the impact of their marketing sweats by using the strengths of each communication tool. For illustration, while advertising helps make brand mindfulness on a large scale, public relations can enhance credibility and trust by securing positive media content. Meanwhile, direct marketing enables substantiated communication with individual guests, while digital marketing offers precise targeting and real- time engagement openings. also, IMC enables companies to maintain thickness in their messaging across different channels, which is pivotal for erecting brand identity and recognition. harmonious branding helps consumers develop a clear understanding of what a brand stands for and fosters trust and fidelity over time. Whether a consumer encounters a brand's communication on social media, TV, or in- store, they should admit a harmonious communication that reflects the brand's values and positioning. Another advantage of IMC is its capability to produce community among colorful marketing channels, performing in a accretive effect that amplifies the overall impact of the crusade. When different communication tools are strategically integrated, they support each other, creating a more important and memorable brand experience for consumers. For illustration, a company may launch a TV announcement crusade to make mindfulness, rounded by social media elevations to encourage engagement and drive business to the website. By coordinating these sweats, the company can induce lesser brand visibility and engagement than if each channel were used singly. In addition to enhancing brand mindfulness and engagement, IMC also facilitates better dimension and evaluation of marketing effectiveness. By integrating different communication tools, companies can track the performance of each channel and assess how they contribute to overall crusade objects. This allows marketers to optimize their strategies in real- time, allocating coffers to the most effective channels and refining messaging to more reverberate with their target followership. still, enforcing IMC effectively requires careful planning, collaboration, and collaboration across different departments and stakeholders within an association. It involves aligning marketing objects, messaging, and creative means across colorful channels while icing thickness in brand positioning and identity. This frequently requires breaking down silos between departments similar as marketing, advertising, public relations, and deals to foster collaboration and integration. also, with the rapid-fire elaboration of technology and the proliferation of new communication channels, the geography of IMC is constantly evolving. Companies must stay nimble and acclimatize their strategies to influence arising trends and technologies to stay applicable and competitive. From social media and influencer marketing to immersive gests and stoked reality, there are endless openings for brands to engage with consumers in innovative ways and produce memorable brand gests . In conclusion, Integrated Marketing Dispatches is a strategic approach that integrates colorful communication tools to deliver a cohesive and harmonious brand communication across multiple channels. By coordinating sweats across advertising, public relations, direct marketing, deals creation, and digital marketing, companies can maximize the impact of their marketing sweats, enhance brand mindfulness and engagement, and drive business results. still, successful perpetration requires careful planning, collaboration, and adaption to evolving consumer trends and technologies.

By vinoth kumar4 days ago in Trader

One of the Crazy Things Rich People Do That's Scary To Think About

They impress us, and sometimes they scare us, but the ultra-rich are always interesting. Some of their famous activities include buying yachts too big to move through channels, buying ridiculously priced cars that could feed the homeless of New York for weeks, and their expensive tastes in sex workers.

By Jason Ray Morton 4 days ago in FYI

Comments

There are no comments for this story

Be the first to respond and start the conversation.