(New)Long Term Capital Gain Tax Rate FY 2020-21(AY 2021-22)

LTCG Tax Rate for FY 2020-21

For better graphical data presentation you may visit the below link:

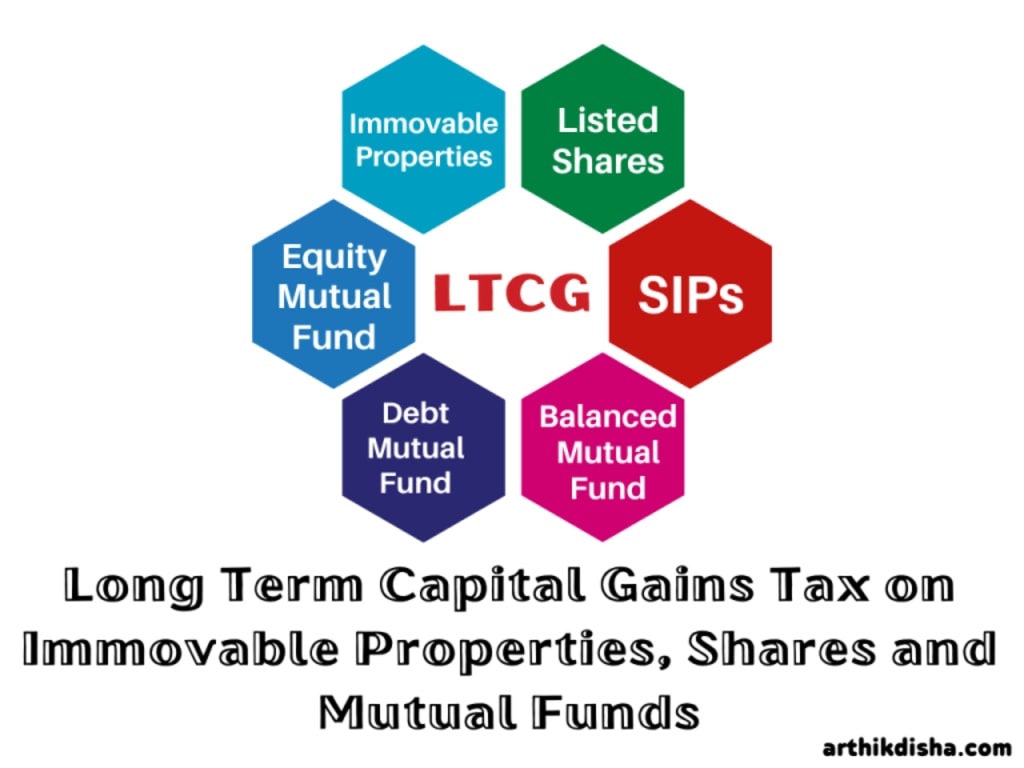

Long Term Capital Gain Tax:

Before knowing the Long Term Capital Gain Tax Rate for FY 2020-21 and AY 2021-22, first, we need to know the types of capital assets we are dealing with and the period of holding of the assets with you.

Long Term Capital Gain Tax on Immovable property:

Immovable property: Any capital gains arising out of the sale or transfer of immovable properties held for more than 36 months, will be considered as the Long Term Capital Gains.

From FY 2017-18 and the AY 2018-19, this period of holding for Long Term Capital Gains has been reduced from 36 months to 24 months in case of immovable properties such as land or building or both.

Long Term Capital Gains Tax on Shares/Mutual Funds:

Listed Shares/ Units of Equity Mutual Funds: Any gains arising out of sale or transfer of listed shares, units of equity-oriented Mutual Funds,equity-oriented balanced Mutual Funds will be considered as the Long Term Capital Gains, only if it is held for more than 12 months.

Unlisted Shares: From FY 2016-17 and AY 2017-18, the period of holding has been reduced to 24 months in case of unlisted shares of a company.

Debt Mutual Funds/Balanced Funds/Hybrid Funds: Any capital gains arising from Debt funds, Balanced funds, Hybrid debt mutual funds(all debt oriented) will be considered as Long Term Capital Gains only if they are held for more than 36 months.

Therefore capital gains primarily depend on the nature of assets and the period of holding. The categorisation between the Short Term Capital Gains(STCG) and Long Term Capital Gains(LTCG) is very much crucial as this determines the Capital Gains Tax rate.

Long Term Capital Gain Tax Rate for FY 2020-21 & AY 2021-22

Types of Asset Period of Holding for LTCG Tax Rate

Immovable Property– More than 24 months 20% with indexation

Land or Buildings

Listed Equity shares More than 12 months 10% over and above ₹1 L

Equity Mutual Funds More than 12 months 10% over and above ₹1 L

Balanced Mutual Funds (Equity-oriented) More than 12 months 10% over and above ₹1 Lakh

Debt Mutual Funds More than 36 months 20% with indexation

Balanced Mutual Funds More than 36 months 20% with indexation

(Debt-oriented)

Capital Gain Tax on Sale of Property

There are thousands of internet users who while calculating Capital Gain Tax on Sale of Property, search for the term how to save capital gain tax on sale of residential property. But they should first understand how capital gain arises on the sale of properties to be specifically immovable properties.

Long Term Capital Gain Tax Rate-ArthikDisha

Holding Period: Any capital gains arising out of the sale or transfer of immovable properties held for more than 24 months from the date of acquisition, will be considered as the Long Term Capital Gains(LTCG).

Long Term Capital Gain Tax Rate: For FY 2020-21 and AY 2021-22, the applicable LTCG tax rate is 20% with indexation plus 4% Cess.

So, if the property is sold before 24 months from the date of the holding it will be considered as the Short Term Capital Gain.

Computation of Capital Gain Tax on Sale of Property

The long term capital gain tax on sale of property is to be calculated as below:

Particulars Amount(₹)

Sale consideration from the capital asset XXXXXX

Less: Expenditure incurred for sale of assets such as brokerages, commission, advertisement exp. and etc. XXXXXX

Net Sale consideration XXXXXX

Less: Index cost of acquisition XXXXXX

Less: Index cost of improvement if any XXXXXX

Long Term Capital Gain on sale of property XXXXXX

Cost of indexation is calculated by the below formula

(Cost of acquisition X Cost inflation index of the year of transfer) / Cost inflation index of the year of acquisition

Cost Inflation Index (CII) from FY 2001-02 is as follows

Sl. No. Financial Year Cost Inflation Index(CII)

1 2001-02 100

2 2002-03 105

3 2003-04 109

4 2004-05 113

5 2005-06 117

6 2006-07 122

7 2007-08 129

8 2008-09 137

9 2009-10 148

10 2010-11 167

11 2011-12 184

12 2012-13 200

13 2013-14 220

14 2014-15 240

15 2015-16 254

16 2016-17 264

17 2017-18 272

18 2018-19 280

19 2019-20 289

20 2020-21 301

Now let’s take an example to understand clearly how long term capital gain arises on sale of property.

Example: Sri Anil Kumble bought a residential property on 09.11.2008 for ₹22 Lakhs. Sri Kumble incurred ₹1.25 Lakh as cost of painting and some wooden works in May 2009.

He sold this house in August 2020 for ₹54 Lakh. Further, he has paid ₹95,000 as brokerage or commission charges. Now, what will be the Long Term capital gain tax for the FY 2020-21.

Computation of Capital Gains Tax on sale of property:

Particulars Amount(₹)

Sale consideration from the capital asset 54,00,000

Less: Expenditure incurred for sale of assets such as brokerages, commission, advertisement exp. and etc. 95,000

Net Sale consideration 53,05,000

Less: Index cost of acquisition (22 L X 301)/137 48,33,000

Less: Index cost of improvement if any (1.25 L X 301)/137 2,74,600

Long Term Capital Gain on sale of property(LTCG) 1,97,400

Long Term Capital Gain Tax to be paid 41,059.00

(197400X20%)X1.04

Long Term Capital Gains Tax on Shares

One should keep in mind that Long Term Capital Gain Tax on Shares used to be fully tax exempted earlier U/S 10(38) of the Income Tax Act. But w.e.f FY 2018-19 and AY 2019-20, long term capital gains have been made taxable over and above ₹1 Lakh in a financial year U/S 112A of the Income Tax Act.

This Long Term Capital Gains Tax on Shares might probably discourage the investors. Only time will say the actual scenario. Because it used to be fully tax exempted from FY 2004-05.

Before knowing the rate of long term capital gain tax on Shares, you must know about the grand-fathered day in detail.

Section 112A w.e.f 01.04.2018: In the finance budget 2018, we have come to know about the grand-fathered day which is 31.01.2018. This means any shares acquired on or before 31.01.2018, the cost of acquisition would have to be calculated based on the following method.

The cost of acquisitions of a listed equity share acquired by the taxpayer before 01.02.2018, shall be deemed to be the higher of the following:

a) The actual cost of acquisition of such asset; or

b) Lower of the following:

(i) Fair market value of such shares as on 31.01.2018; or

(ii) Actual sales consideration on its transfer.

Example: Mr. Tendulkar is a salaried person. In August 2017 he purchased 200 shares of MRF Ltd. @ ₹1,500 per share from Bombay Stock Exchange. These shares were sold through BSE in October 2019 @ ₹3,600 per share. The highest price of MRF Ltd. shares quoted on the stock exchange on 31.01.2018(Grand-fathered day) was ₹2,200 per share. What will be the nature of capital gains in this case and how much capital gains tax he should pay?

Computation of Long Term Capital Gains Tax on Shares:

Nature of Capital Gains: Since the shares of MRF Ltd. was sold after holding them for more than 12 months, the gains so arise here are Long Term Capital Gains(LTCG).

Applicability of Section 112A: Since shares have been transacted through the recognised stock exchange and are liable to Security Transaction Tax(STT), section 112A is applicable in this case.

Solution: Cost of acquisition of MRF Ltd. shares will be higher of the following two:

a). Cost of acquisition (200X1500) ₹3,00,000

b) lower of the following two:

Highest price quoted on Grand-fathered day i.e. 31.01.2018 (200X2200) ₹4,40,000;

Sale consideration (200X3600) ₹7,20,000.

So, the cost of acquisition is ₹4,40,000. (440000 and 300000 whichever is higher)

Particulars Amount(₹) Amount(₹)

a). Cost of acquisition (200X1500) ₹3,00,000

b). Lower of the following two

I. Highest price quoted on Grand-fathered day i.e. 31.01.2018 (200X2200) 4,40,000

II.Sale consideration(200X3600) 7,20,000

Lower of above two 4,40,000

So, cost of acquisition- higher of a). and b). 4,40,000

Sale consideration 7,20,000

Less: Cost of acquisition 4,40,000

Long Term Capital Gain on Shares(720000-440000) 2,80,000

LTCG Tax on shares to be paid 18,720

(280000-100000)X10%*1.04

Mutual Fund Capital Gains Tax/LTCG on Mutual Funds

While calculating Mutual Fund Capital Gains Tax, we first need to know what kind of mutual fund it is, and what is the holding period. The following table will help you in deciding the LTCG on Mutual Funds.

Types of Asset Short Term Long Term

Equity Mutual Funds Less than 12 months More than 12 months

Balanced Mutual Funds (Equity-oriented) Less than 12 months More than 12 months

Debt Mutual Funds Less than 36 months More than 36 months

Balanced Mutual Funds(Debt-oriented) Less than 36 months More than 36 months

Equity oriented balanced mutual funds mean where equity exposure is more than 65%. If for any mutual fund scheme the equity exposure is less than 65%, it is considered as the Debt mutual fund.

1. Equity Mutual Fund Capital Gains Tax

LTCG on Mutual Funds is charged to tax @10% if the gains exceed ₹1,00,000 in a financial year. However, the benefit of indexation is not allowed here.

But one should keep in mind that Tax saving mutual fund is a little bit different from the regular equity mutual fund. As there is a mandatory lock-in period of 3 years for tax saving mutual funds. One can sell it when the lock-in period of 3 years is completed. Also, the Tax saving mutual fund gains are taxed @10% like the regular ones.

2. Long Term Capital Gain Tax Rate on Debt Funds:

Long term capital gains on debt mutual funds are taxed @ 20% with indexation. Indexation is a method and using this method we can bring the value of the actual cost of acquisition to the value of the current date by taking into consideration the inflation factor.

Indexation allows inflating the purchase price of debt mutual funds to reduce the amount of capital gains.

3. Systematic Investment Plans(SIPs):

The systematic investment plan or SIP is not a product like equity or debt mutual fund. This is a method of investment wherein the investors get the opportunity to make regular investments of a small amount like weekly, monthly, quarterly, semi-annually or annually.

Since this is not a different product, the taxation on SIPs depends on the type of SIP and the period of holding. This means each and every investment is considered as a single and new one.

Therefore, if a SIP investment has completed the 12 months threshold limit, the capital gains arising from this is considered as the Long Term Capital Gains and charged to tax @10% if the gains exceed ₹1 Lakh in a year.

About the Creator

Arthik Disha

A Personal Finance Blogger. Passionate about finance.

Keep reading

More stories from Arthik Disha and writers in Trader and other communities.

Bank Frauds In India /Financial Frauds In India 2020

Bank Frauds in India/Financial Frauds in India Bank Frauds in India- It is quite imperative for all of us to know that the total economic activity of the world got tremendously disrupted due to the COVID 2019 pandemic and India is not an exception to this impact.

By Arthik Disha3 years ago in Trader

the best sofas on the market!

In the world of interior design, sofas occupy a central place, not only as functional furniture but also as essential decorative elements. They are the family gathering place, the symbol of comfort and conviviality in our living spaces. Today we witness the diversity and innovation in the world of sofas, with models that combine style, comfort and functionality in an exceptional way.Among the options available on the market, examples such as the "GrekPol Paris Corner sofa in corduroy fabric Poso with convertible function and storage space - Universal - Beige" offer an elegant combination of contemporary design and practicality, with a convertible function and integrated storage space, ideal for small spaces. Similarly, the "HOMCOM Sofa Convertible 3 Seater Scandinavian Design Tilt Adjustable Backrest 3 Levels Central Fold-Down Backrest 2 Glass Holders Solid Wood Linen Gray" seduces with its sleek Scandinavian design, adjustable backrest features and versatile character, adapted to different interior layouts. In addition, models such as the "SILAPE - Santi Convertible Corner Sofa - with Chest - in Leatherette and Fabric (Madryt 1100 + Berlin 01, Left Angle)" offer a modern and sophisticated aesthetic, combined with practical functionality thanks to its integrated storage space. These examples illustrate the diversity and innovation that characterize the sofa market today, while emphasizing the increasing importance given to the combination of comfort, style and functionality in the choice of furniture for our interiors. In this article, we will explore in more detail the different sofa options available, highlighting their distinctive features and benefits, in order to help consumers find the perfect sofa for their living space.

By Alicia Lhotellier4 days ago in Trader

Comments

There are no comments for this story

Be the first to respond and start the conversation.