If You Want to Hedge Against the Surge in Residential Housing Prices

Own Some Gold

For most families, purchasing a home represents one of the most significant investments they will ever make during their lifetime! A recent estimate released by Financialsamuri.com (January 6, 2022) reveals that a typical homeowner family has 70% of their net worth invested in a primary residence. After experiencing countless bidding wars, and a surge in housing prices, some homeowners/prospective buyers have become worried that prices could collapse and leave them with a case of buyer’s remorse.

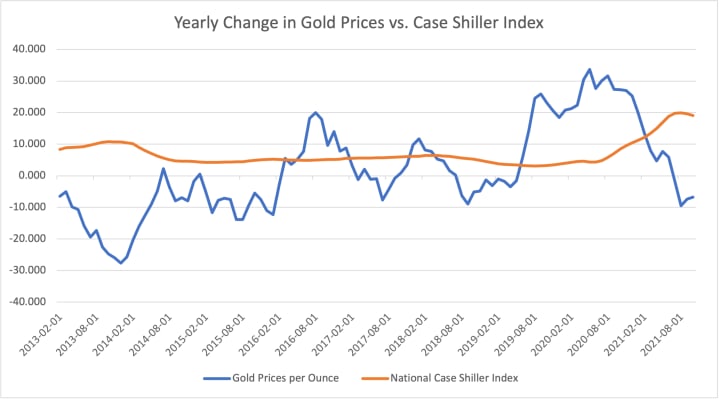

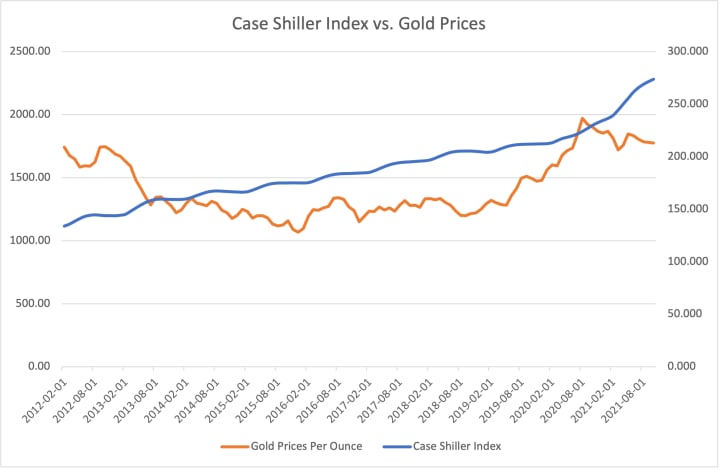

The U.S. National Case-Shiller Home Price Index (CS-HPI), long considered as one of the most accurate barometers of housing prices, rose by 10.4% on a year-over-year basis in December 2020 and an additional 19.0% as of October 2021 (latest data available) on a comparable basis.

The CS-HPI tracks the prices of the same housing unit over time to minimize the price distortions arising from any compositional changes in the types of housing units sold over time.

So what would happen if the U.S. residential housing prices suffered a black swan effect that caused a sharp decline in prices? A black swan outcome is typically an unpredictable event that leaves almost everyone dumbfounded.

How many analysts/investors correctly predicted (even a few months in advance) that the U.S. and other major economies would shut down in March 2020 and cause one of the worst recessions in U.S. history?

This example illustrates why it is always a good idea to hedge our financial exposures. The good news is that with excess demand and a continued shortage of housing inventory, a sudden plunge in housing prices is not our base case scenario. Nonetheless, even a perfectly healthy person raising a family often purchases life insurance to protect against black swan events.

How Can the Average Family Hedge Against Such Risks?

Wealth management portfolio managers are always on the hunt for uncorrelated assets to add to their portfolios to lower risk. That is why when they find assets exhibiting a negative correlation with their portfolio, they often move quickly to add those assets to their portfolios.

It is no secret that the historical correlation between the S&P 500 Equity Market Index and Investment grade bonds is about -.06%. This explains why many portfolio managers include fixed-income assets in their portfolios. It is not unusual to see that portfolio managers also allocate a small allocation to cash (consisting of low duration Money-Market or U.S. Treasury securities) given that these assets sported a -0.17% correlation with the S&P 500 index.

Using this same line of reasoning, it would make sense for homeowners/prospective homebuyers to consider looking for assets that sport a negative correlation with U.S. housing prices. After reviewing various assets classes, we find that gold prices feature this exciting characteristic. From the 1980s to the present, we find that the yearly changes in the CS-HPI and gold prices generated an outsized -.23% correlation!

That negative correlation outbids the negative correlations we observed between U.S. equity prices and fixed-income, and the correlation between U.S. equity prices and U.S. cash holdings within a wealth management portfolio!

If portfolio managers have always sought to include negatively correlated assets in their portfolios, why wouldn’t individuals holding U.S. housing assets not use this same strategy to protect themselves?

The good news is that the average person has a broad spectrum of choices when hedging their housing assets with gold exposure. They could do it by purchasing gold coins/currency, actual bullion, gold futures contracts, or gold mining stocks. These are just a few of the many options that holders of residential housing assets can pursue to hedge their residential housing exposure and avoid suffering from our next black swan in U.S. housing markets!

About the Creator

Anthony Chan

Chan Economics LLC, Public Speaker

Chief Global Economist & Public Speaker JPM Chase ('94-'19).

Senior Economist Barclays ('91-'94)

Economist, NY Federal Reserve ('89-'91)

Econ. Prof. (Univ. of Dayton, '86-'89)

Ph.D. Economics

Keep reading

More stories from Anthony Chan and writers in Trader and other communities.

How to become an Amazon Merch seller!!

In today's digital age, opportunities for creative entrepreneurs to showcase their talents and earn a living abound. One such platform that has gained significant popularity is Amazon Merch, an innovative program that allows individuals to design and sell their own merchandise directly on Amazon. From T-shirts and hoodies to pop sockets and mugs, Amazon Merch offers a wide range of products for creators to showcase their unique designs and reach a global audience.

By Willow Peddy5 days ago in Trader

Comments

There are no comments for this story

Be the first to respond and start the conversation.