Last time we talked all about the IRA, AKA the "Eye-Ra." The good news is that most of the limits and terminology still applies to the Roth IRA, but I wanted to cover a few of the small differences.

The Roth IRA was proposed by William Roth II in 1997, so it hasn't been around forever. The whole idea of a Roth is to have money that you've already paid taxes on grow without taxes so you can take it out tax-free.

I'll say that again… a Roth IRA works in the opposite manner that a traditional IRA works when it comes to taxes. Basically, a person is hedging their bets that taxes will change in the future.

Traditional thinking is to reduce your taxable income now and pay less taxes by contributing to a 401(k) or a traditional IRA. One would assume that you need less to live on during retirement if your home is paid up and your children have moved out. Right?

That’s the hope at least for those who solely contribute to pre-tax retirement accounts. One could assume that if you live on less than you needed during your working years, then taxes shouldn't be a huge issue. However, it's already tough for most Americans to live on less than we make now, so the thought of living on less than that is where a Roth could help.

Here are a few ideas to consider with a Roth IRA:

1. If you're saving and investing into a Roth IRA, you can put away $6,000 per tax year AFTER taxes. So you've earned income, paid or accounted for taxes, and then you save and invest from the remainder. If someone is over 50 they can do an extra $1,000 per year.

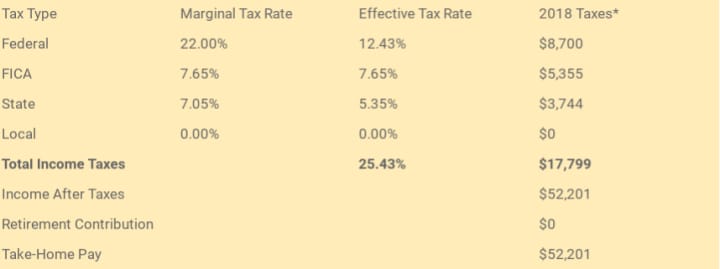

The number isn't any different than the traditional IRA, but if you're a single taxpayer making $70,000 that puts you in the 22 percent federal bracket. I ran the example as if a single person lives in MN. After adjusting for the effective vs. marginal tax rate you'd take home about $52,201. Then put in the $6,000 out of the $52,201.

2. There are income phase outs for those wanting to contribute to a Roth IRA. If you make over $122,000 per year as a single person, you can contribute less and less down to $0 once you make $137,000 per year. These numbers did go up by about $2,000 since 2018.

A married couple filing jointly could make up to $193,000, but their options for a Roth phase out at $203,000 per year.

Why is that important? The federal government doesn't want high income earners to dump tons of money into Roth IRAs and then live tax free later. So they decided to cap both the amount and the income that you can earn for Roth IRA contributions. One interesting fact is that you still are penalized 10 percent on any withdrawals above the principal before age 59.5.

Certain jobs can make too much money to allow for personal Roth IRA contributions. That’s not a bad thing to earn over the amount, but something to think about if people are on the rise.

For example a resident doctor may earn $70,000 per year. When promoted to a permanent position his or her income could rise up to $150,000, thus taking out their chances to contribute to a Roth going forward.

3. There are some creative planning options for tax free savings with a Roth. One thing that is allowed is called a Roth conversion. No matter your income, you could convert a non-deductible IRA into a Roth.

You could pay taxes on the conversion, but then moving forward the principal would grow tax free and could be withdrawn tax free at retirement.

The other option that many employers are now providing is a Roth 401(k) option. Regardless of income, because it's an employer sponsored plan an employee could contribute up to $18,000 per year!

If the employer matches a certain percentage, then the match goes into the pre-tax bucket. So those who are able to do a Roth 401(k) have two types of accounts if and when they leave their employer.

They say that two things are certain in life. Death and taxes. Check out all of your options when it comes to being effective with taxes!

About the Creator

Isaiah Goodman

Isaiah is a Certified Financial Education Professional TM and a dynamic speaker who loves to empower others. Isaiah has been married to his wife since 2012. At home they are joined by their four children and dog.

Keep reading

More stories from Isaiah Goodman and writers in Trader and other communities.

Becoming Celebrated

Imagine this, you graduate high school, go to college and pay off all four years of college by working a simple summer job. When you graduate you have enough money and credit to start a family, buy a home, car, and even a lake house. You work at the job for years, and they promise you a pension that will pay out a guaranteed amount during your retirement years. You retire, get a gold watch. And plan to travel the world on your pension and social security checks. The good old life right? Probably what some people think of when they talk about making America great again.

By Isaiah Goodman5 years ago in Trader

The Rollercoaster Ride of a Trader's Career

Unveiling the Drama and Humor Behind the Trading World Wanted: Adventurous souls with nerves of steel, a passion for numbers, and a flair for risk-taking. Does this sound like you? Welcome to the chaotic and exhilarating world of trading. Strap yourself in for a wild ride filled with highs and lows, thrills and spills, wins and losses. In this article, we'll delve into the heart-pounding journey of a trader's career, where drama and humor mingle in a dance of chaos and order. Hold on tight as we explore what it truly means to embark on a path where fortunes are made and lost in the blink of an eye.

By Max Gachet6 days ago in Trader

Comments

There are no comments for this story

Be the first to respond and start the conversation.