A 100-Year Backtest That Beats The Market By Far

A simple ratio used by the best investor in history to beat the market

It is very easy to test an investment strategy by looking in the rear-view mirror or backtesting. Generally, these backtest are done with very high overfitting, this means that the parameters chosen at the time of selecting the stocks and the time of holding them in the portfolio are so specific that obviously, that trend will not give the same returns over time. In addition, most of these models are made on a specific period of history, as they would not have worked in any other period of time of the economic cycle.

But, what would you say if it is possible to backtest a single parameter that clearly beats the index for over 100 years?

Mark Spitznagel, one of the best investors, if not the best, has managed to find such a parameter and has used it to bring an average annual return or CAGR of over 70%. If you want to know more about him and the principles of his investment philosophy, you can read the following article.

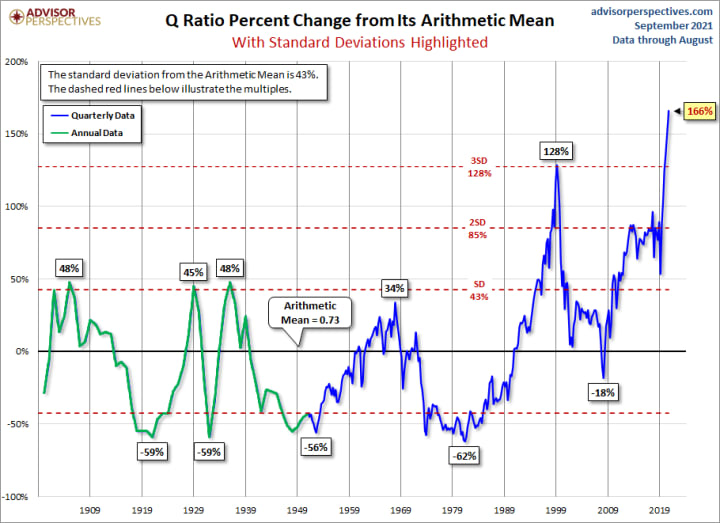

To achieve these returns Spitznagel has always relied on a parameter called Tobin’s Q Ratio. This parameter is calculated as the Enterprise Value (equity plus debt) to the aggregate corporate assets or invested capital (or, with no debt, aggregate equity over assets). This means that when we have a high value for this parameter, it means that the market is overvalued, while when this ratio is low, it means that the market is undervalued. Looking at the value of this ratio for more than 100 years, we have that:

As you can see this ratio clearly tends to revert to the average, which is around 0.73. Currently, the market is at 1.94, which is the highest value in history. It has been able to reach this value due to the capital injections by central banks (mainly the FED), which has meant that for a little over a year now 40% of the dollars in circulation have been printed. This has caused stock prices to rise radically. This event is not sustainable over time without generating (hyper)inflation or rising interest rates.

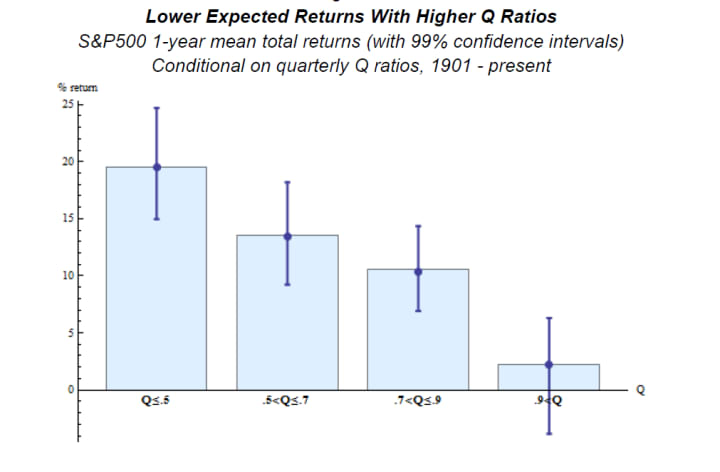

Historically, it has been shown that investing in a market situation that has a low Tobin Q ratio and selling during periods of high Tobin Q ratio has had positive returns and far outperformed the index. In fact, the returns of stocks with a high Tobin Q ratio tend to have worse returns 99% of the time, as shown below:

Fat Tails and Tobin’s Q Ratio

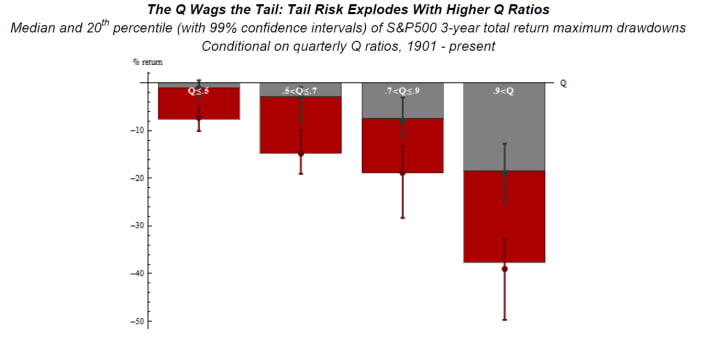

In order to clarify our doubts, the Universal fund has made a study to corroborate this. They have chosen 3-year total return drawdowns (at monthly closes). Clearly, extreme market drawdowns occur with 99% confidence during high Q situations.

At current valuations (Q ≈ 1.94) — and if this 110-year relationship continues — there is an expected (median) drawdown of 20% and a 20% chance of a larger than 40% correction in the S&P500 within the next few years.

The markets are trading at historically high multiples and we may never see them at these multiples again. As we show in this article, it is necessary to be right only once to be able to retire and therefore we expose our portfolio on a weekly basis so that all investors can benefit from possible stock market crashes that we do not know when they will arrive, but it seems clear that they will materialize. If you want to know more about our investment philosophy and strategy, do not hesitate to subscribe to our newsletter.

This article is for informational purposes only, it should not be considered Financial or Legal Advice. Not all information will be accurate. Consult a financial professional before making any major financial decisions.

About the Creator

Carlos Pascual

Writing Helps Me Keep Learning Of Wild Chance | Fat Tails | Long-Term Dependence | Concentration | Discontinuity.

Writer at www.asymmetricfinance.co

Enjoyed the story? Support the Creator.

Subscribe for free to receive all their stories in your feed. You could also pledge your support or give them a one-off tip, letting them know you appreciate their work.

Keep reading

More stories from Carlos Pascual and writers in Trader and other communities.

The Trader's Path

I started ‘trading’ in the late winter/early spring of 2021. At the time, I had a decent amount of extra income, and after coming across some YouTube videos on trading, I figured what I’m sure most people do, “this doesn’t look that hard.” I quickly made around 20K during the bull run from 29K to 60K trading on Bybit and thought I was a God. I was quickly humbled after getting liquidated on an isolated trade and saw my 20K net profit get cut in half. It was then that my real trading journey began. In March 2021, I joined Chart Champions (under a different name) and stayed in the group for about 1.5 years. To the credit of CC, I truly did learn a lot about trading (shout out to Igor and Trader R). I eventually left around the summer of 2022 as I felt I had outgrown the core principles they were teaching. From that summer to the beginning of 2023, I engaged in a cycle of up and down trading where I eventually lost the full 20K plus my initial investment. To compound this even further, I had two different spot accounts go way underwater, putting my total losses (about half unrealized/still holding) around $60K. Losing the entire 20K, along with my initial investment, and watching my spot accounts plummet was one of the most depressing periods of my life. The overwhelming sense of isolation was intensified by having no one to share this pain with. For those who truly understand the intricacies of technical analysis, it’s not something easily explained to the average person. I shut down my computer and didn’t look at a chart again until this past spring of 2024.

By The Faceless Trader2 days ago in Trader

Comments

There are no comments for this story

Be the first to respond and start the conversation.