26 Costliest Credit Card Mistakes To Avoid Debt Trap & Attain Peace of Mind

Personal Finance

Dear Readers,

As we know Credit Cards are treated as luxury lifestyle, but at the same no one just think a second thereafter, it is actually a liability (takes money out of your pocket). It is boon for those who uses it effectively and who are financial disciplined and bane for those who carelessly uses it and end up in debt trap that accrues month on month having a huge amount and this results in loss of peace of mind while clearing the same and you other financial or life goals will also get affected, right!

Hence, in this context, for the benefit of the community, I am herewith sharing an useful information that actually I had created earlier in the form of Digital Product that provides an awareness about the wise strategies to be adopted while using Credit Cards and what costliest mistakes can be avoided while ensuring your money is not lost in the process. I have herewith released as FREE to help the community/readers and this is based on my 8+ years of experience in usage of credit cards and even the mistakes I had learnt thereafter, which I want others not to do so to protect one’s money/wealth.

These below suggested best practices on usage of Credit Cards also act as money savings strategies/guidelines/techniques and myself as a personal user of Credit Cards since 2012, hereby suggest you to adopt these practices to your best possible extent and help yourself after following the same in achieving Money Savings while also using Credit Cards and avoid falling into Debt Trap/Loan Trap and gain peace of mind and also on a long-term, it helps you in attaining your financial goals and might be a part factor too in achieving your Financial Freedom.

This was earlier written by me from the context of Indian Credit Card Users, however since Credit Cards are served almost in all the countries, some or majority of the points may have been experienced by yourself and also may or may not be applicable as per the country specific and card specific features. In general, you can cross check with your practices and validate wherever applicable these points in your country/region. This doesn’t mean, you cannot use credit cards, but use them responsibly and carefully, that's a concern here! which gives you peace of mind, that's what we all require right!.

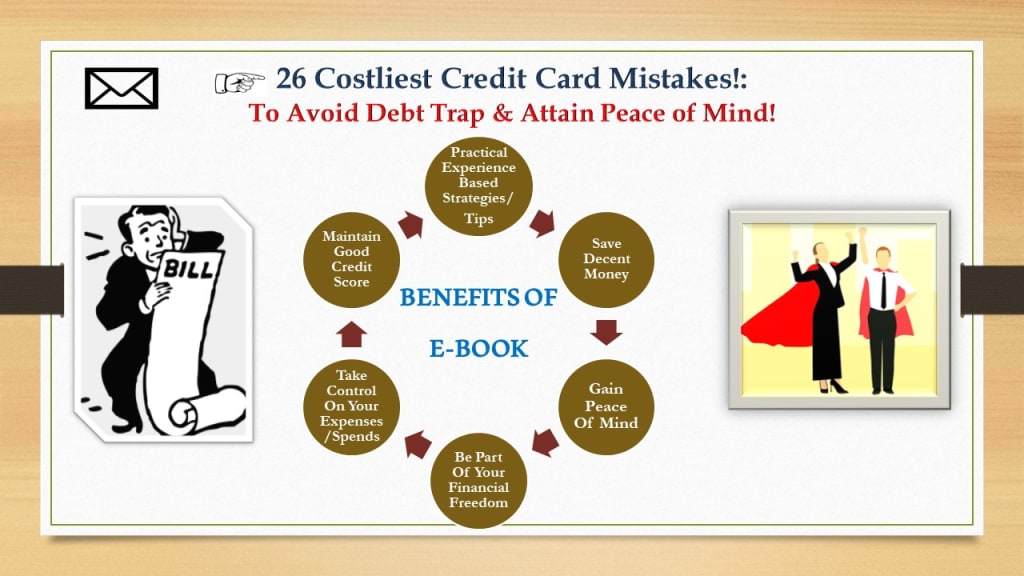

Benefits in being financially disciplined user of Credit Cards are as follows:

- Helps you to save your hard earned money.

- Avoids falling into Credit Card Debt Trap.

- Acts as Financial Literacy.

- Helps to gain control on your expenses/spends.

- Partly contributes to your financial freedom.

- Creates peace of mind from financial worries.

- Develops financial discipline and builds good credit score.

- Helps to widen your money saving skills than thought earlier.

- Avoids unnecessary calls from credit card institutions/banks.

- Helps to own your financial responsibilities/situation.

There we go..,in detail in the below strategies:

1. Never pay minimum amount as per the credit card statement bill, as this will lead you to fall into debt trap due to accumulating interest and this burden gradually increases in the later months.

2. Best method: To pay credit card amount in full.

3. Avoid fresh transactions on the credit card when you have not paid your credit card bill in full amount in the previous month(s) bill, as this will attract interest/additional charges etc., in the next bill and goes on with accumulating.

4. Since credit cards have highest interest (16–48% per Annum), delayed payment causes penalties in the form of addition of interest/financial charges/taxes/fees etc., as per respective banks terms and conditions, thereby experiencing huge burden or difficult to repay situations.

5. Always pay full credit card amount intime, this will help to build your GOOD Credit score.

6.Don’t practice credit card revolving i.e., don’t use credit card to pay another credit card due, this easily leads you in trap with burden of accumulated interest and reaching to situation of unable to pay/struggle.

7. Apply for Credit Card ONLY if you have repayment capacity, since you know your salary/income, commitments, needs, wants and regular expenses to yourself and to your family.

8. Avoid subscriptions on Credit Card on Entertainment Channels/Portals if you don’t have time to spend.

9. Convert high amount purchase/transactions into EMI mode either by online/contacting customer support of bank to simplify your payment, so that, its easy for you to pay the same in installments/parts and you don’t feel much burden. Of course, this attracts some interest charges/financial charges/taxes etc., than higher in case of non-payment, but with your financial payment discipline, you can come out of this at the earliest.

10. Once you are a regular user of credit card for years, try to negotiate with credit card issuing banks to waive-off Annual Membership Fees/Charges for the credit card being used by you.

11. Don’t use credit cards for the sake of discounts/offers announced in the market/online portal.

12.Check rate of interest offered before converting high amount transactions into EMI/pay-in-parts, as this helps in decision making process of your purchase.

13. Always ensure as thumb rule, total credit card limit utilization in general advised to be restricted to less than (<) 35–40% of limit sanctioned to your credit cards. Credit Card limit can be seen in your credit card bill statement. This helps you to track your expenses and also control your urge to future spending.

14. Don’t use/swipe credit card for the sake of reward points/cash back or to gain any other benefits as long as it is a need.

15. Limit number of credit cards (maximum 2–3). Avoiding is even better.

16. Don’t take higher credit card limit even if card issuing banks offer, else, this prompts you to spend more.

17. Have a habit of cross checking your credit card bill statements to understanding your expense/spend pattern and take control where ever needed and avoid unnecessary burden.

18. Don’t transfer amount from credit card to your Savings Bank account from any online portal, as this will attract 2–5% conversion charges and also lands you in debt/trap indirectly.

19. Don’t withdraw cash using credit card from ATM as it attracts additional charges.

20. Pre-pay credit card loan dues/outstanding only if you have surplus amount and ensure to ask the bank representative/customer support, are there any prepayment charges involved (example like 2–3% on the outstanding loan amount being paid or as amount decided to pay) and take a decision accordingly.

21.Don’t apply for too many credit cards at same time/period, as this might reduce your CIBIL Credit score and likely, there are chances of your credit card application rejection.

22. Don’t reveal your credit card passwords nor save any credit card details in any online platform to avoid cyber attacks/unauthorised transactions. Only you should know.

23. After closing the credit card, obtain NOC from the credit card issued institution/banks at the earliest. This helps you to avoid sudden shocks in future when someone asks you to pay an outstanding amount as there are chances of your account still active and there might be addition of any annual charges accumulating over the period.

24. Avoid credit card usage on foreign tours, except under emergency. Confirm additional charges with banks if any before you travel.

25. Think always, Credit Card is a Liability, not an Asset. (Assets add money into your pocket, Liability takes money out of your pocket).

26. Avoid taking loans on Credit Cards if offered by banks, provided under emergency only, further to based on your repayment capacity.

So, in overall, if you adopt these guidelines to your best possible extent, you might end up in decent money savings over the period or take control of your finances and you would be feeling proud when you feel, there is some transformation you had achieved.

Disclaimer: Results may vary person to person and hence, treat these practices/tips/strategies as stated for your guidance/educative purpose only. Wherever possible, consult your financial advisor/expert/banks/CA/refer blogs/your institutions in your country/region for more assistance and understanding as applicable.

If you feel the article content is helpful and if there are any other points if you feel I can add to this based on your experiences in your respective country, please mail your comments on my mail at: [email protected] or on my website www.selfmoneycare.com

Thanks for reading this article and appreciate your patience.

About the Creator

Madhu Kumar C

Self Employed/Internet Marketer/Affiliate Marketer/Blogger/Ex-Engineer.

Passionate about writing on Quora (0.24 Million Views).

Keep reading

More stories from Madhu Kumar C and writers in Trader and other communities.

the best sofas on the market!

In the world of interior design, sofas occupy a central place, not only as functional furniture but also as essential decorative elements. They are the family gathering place, the symbol of comfort and conviviality in our living spaces. Today we witness the diversity and innovation in the world of sofas, with models that combine style, comfort and functionality in an exceptional way.Among the options available on the market, examples such as the "GrekPol Paris Corner sofa in corduroy fabric Poso with convertible function and storage space - Universal - Beige" offer an elegant combination of contemporary design and practicality, with a convertible function and integrated storage space, ideal for small spaces. Similarly, the "HOMCOM Sofa Convertible 3 Seater Scandinavian Design Tilt Adjustable Backrest 3 Levels Central Fold-Down Backrest 2 Glass Holders Solid Wood Linen Gray" seduces with its sleek Scandinavian design, adjustable backrest features and versatile character, adapted to different interior layouts. In addition, models such as the "SILAPE - Santi Convertible Corner Sofa - with Chest - in Leatherette and Fabric (Madryt 1100 + Berlin 01, Left Angle)" offer a modern and sophisticated aesthetic, combined with practical functionality thanks to its integrated storage space. These examples illustrate the diversity and innovation that characterize the sofa market today, while emphasizing the increasing importance given to the combination of comfort, style and functionality in the choice of furniture for our interiors. In this article, we will explore in more detail the different sofa options available, highlighting their distinctive features and benefits, in order to help consumers find the perfect sofa for their living space.

By Alicia Lhotellier7 days ago in Trader

Europeans reject Chinese cars.

China's car industry has changed over the course of the last ten years, from delivering fundamental western clones to making vehicles that equivalent the world's ideal. As the assembling force to be reckoned with of the world, China is likewise creating them in enormous volumes.

By Phumlani Mdlalose4 days ago in Trader

Comments

There are no comments for this story

Be the first to respond and start the conversation.