How to Spend Without Guilt: Unique Lessons From The Book “The 30 Day Money Cleanse”

Budgeting need not feel restrictive

I have read countless personal money management books, and almost all advocate budgeting. They require distinguishing between needs and wants and letting go of the latter to be able to save. Classic advice. But is it easy to do?

How many times have you written your budget, cut costs, and listed down your expenses only to give up after a week or two? Then you promise to start all over again the following month. You did begin again with fresh energy repeating the same cycle. Correct?

I’ve been there so many times. It’s easier said than done. It’s like dieting. You make a meal plan and deprive yourself of the food you love. After counting days, your body rebels. You eat your heart out and regain your weight plus more.

Spending without guilt

Can we spend on items tagged as “wants” without guilt? How? These questions are answered by the book “The 30-Day Money Cleanse”.

The book provided steps that have to be done every week for 4 weeks. Like other financial books, it discussed the determination of “why,” elimination of limiting money beliefs, and setting money rules through a money journal.

It presented the classic money lessons but made use of the same in a different way. Below are the 3 unique concepts that I got:

1. Happiness Allocation

The book permits you to continue having your daily latte. You can have your expensive caffeine boost every day. Only if it makes you happy. That’s the rule.

The “30-Day Money Cleanse” considers personal circumstances and does not impose “one-size-fits-all” financial restrictions. You will be the one to decide on where you will spend your money based on your values. The book says you put your money where your heart is.

The steps:

List down all the expenses that you incur in a year. The author recommends putting an annual value to better appreciate the amount and plan your money allocation. Also, to cover the expenses that do not come regularly.

By presenting your expenses annually, your $5.00 daily Starbucks would translate to around $1500.00 in a year. With that figure, you can decide if the aroma of your coffee, the ambiance, and the feeling of slowly sipping from your cup is worth it. 2

Then, determine the opportunity cost of this daily habit.

The opportunity cost is what we give up because we decide to maintain our spending. For example, your opportunity cost for the Starbucks coffee habit sees an additional $1500.00 in your stock market investments.

With every spending, put the opportunity cost. Then ask yourself if you are OK with it.

“If yes, then, by all means, put that coffee budget and spend it without guilt”

When you are faced with the opportunity cost, you can then decide to:

Eliminate the expense — bring your own coffee or stop having coffee

Reduce the expense — can you have coffee only 3 times a week?

Find cheaper alternatives — can you substitute the coffee from cheaper coffee shops?

The second and third alternatives can balance your love of coffee and your desire to save for investment. You can actually get both.

“The point of money is to have and experience things in life that we want. It’s nothing more than a tool! Why not treat it that way and look at each expense in terms of the things that make as the happiest”

— Ashley Feinstein Gerstley, The 30-Day Money Cleanse

In doing the happiness allocation, remember that you only have a definite income that is represented by a single pie. You can divide it into unequal chunks based on the happiness parameter.

Once the pie is fully allocated, you can spend the money on what makes you happy without the guilt. You have considered all budget items, and money has been allocated to be spent.

2. Frugal Joys

Frugal joys are free or inexpensive things that really make us happy. It’s different for each one of us. There is an activity in the book on how to determine your frugal joys. As I did the exercise in the book, it made me realize that it was exactly how we saved $6240.00 in a year by recreating our dining out experience at home.

The steps:

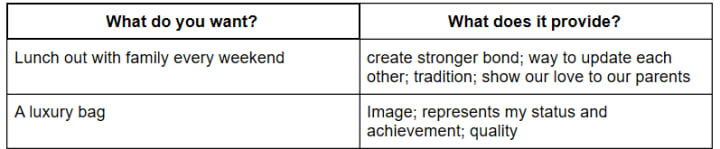

List down things that you usually spend money on. Then also list down the value, purpose, or experience that you want to get. This is how my list looks like:

Now, let the processing begin.

Do I really want the lunch out or I wanted to see my parents and spend time with them?

Do I really want the bag or I long for the image that it will give?

If we let the concept sink in, we don’t actually want the spend items. We are only doing it to achieve the reasons for doing or the “why” in the second column. I want to show my love to my parents. That’s why I’m willing to spend weekly for us to dine out.

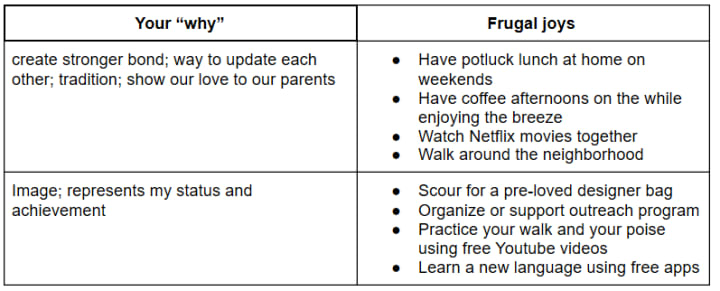

Now, are there free or cheaper activities that I can still bond and show my love for my parents? Yes. And that’s the concept of frugal joys. The book then asks to list down frugal joys activities that will still achieve my “why,” and this is what I made:

Identifying frugal joys requires brainstorming and planning, but it's worth the savings it can give.

The first set of frugal joys work for me as shown in this story: Our Dining Table Made Us Save $6240.00 And Earned Us 52 Memorable Sundays In A Year

3. Money Parties

Money parties are time allotted to review your finances and financial plans. Assess what works. The author recommends money parties to be done every 2 weeks. You can have the party with your family or friends with whom you shared your financial goals. Share your progress and celebrate your small successes. You can have food and drinks after.

Final Thoughts:

The book is unique as it did not impose any financial advice. It didn’t require cutting off credit cards or snowballing of debts first. It considered values and happiness, which makes sense.

How we handle finances is a personal preference based on who we are, where we are, and what circumstances we are in. What works with one does not work with all. Different strokes for different folks.

So friends, go and make your happiness-based budget. A budget that is truly yours.

---

Reference: Gerstley (2019). The 30-Day Money Cleanse. Illinois: Sourcebooks, Inc.

---

This article is for informational and entertainment purposes only. It should not be considered Financial or Legal Advice. Not all information will be accurate. Consult a financial professional before making any major financial decisions.

---

Originally published by the Author on Medium.com

About the Creator

Keep reading

More stories from Olivia Marlene and writers in Lifehack and other communities.

5 Priceless Gift Ideas for Your Boss This Christmas

Christmas gift-giving can be a source of stress for someone who doesn't have a knack for the tradition. It becomes even more complicated to decide what gift to give your boss. What else can you give when you are well aware that your boss has all the material things? Your small token may wind up competing for space in a plethora of gifts sent to him or her this year.

By Olivia Marlene3 years ago in Lifehack

Comments

There are no comments for this story

Be the first to respond and start the conversation.