Old Vs New Tax Regime: Which is Better?

Comparing Old and New Tax Regimes: Making an Informed Choice

The Indian income tax system underwent a significant change in 2020–21 with the introduction of a new tax regime.

This new regime brought about reduced tax rates but also limited the number of tax-saving opportunities available to individual taxpayers. In order to support the implementation of this new system, the government has introduced several incentives in the 2023 Budget.

To determine which regime is better, it is important to consider the variations in tax rates and deductions between the two regimes.

Additionally, the impact of the new regime differs for taxpayers in different income brackets.

In this blog, we will explore these differences and provide practical examples to illustrate how the new regime can affect each tax slab.

New Tax Regime

Starting from April 1, 2020 (FY 2020–21), the Government of India implemented an optional new tax regime for individuals and Hindu undivided families (HUFs).

This new regime, introduced as Section 115 BAC in the Income Tax Act of 1961, established lower tax rates for taxpayers who opted not to claim certain deductions or exemptions.

In the Union Budget 2023, the new tax regime has been made the default option, requiring taxpayers to actively choose the old regime if they wish to use it.

However, by selecting the new system, taxpayers forego various exemptions and deductions such as HRA, LTA, 80C, 80D, and others. Consequently, the new tax structure faced some resistance from taxpayers.

To encourage wider acceptance of the new regime, the government introduced significant adjustments in the Budget 2023.

Increased Tax Rebate Limit

These adjustments include an increased tax rebate limit, where individuals earning up to Rs 7 lakh would not be liable to pay any tax under the new regime. Previously, this threshold was set at Rs 5 lakh.

Simplified Tax Slabs

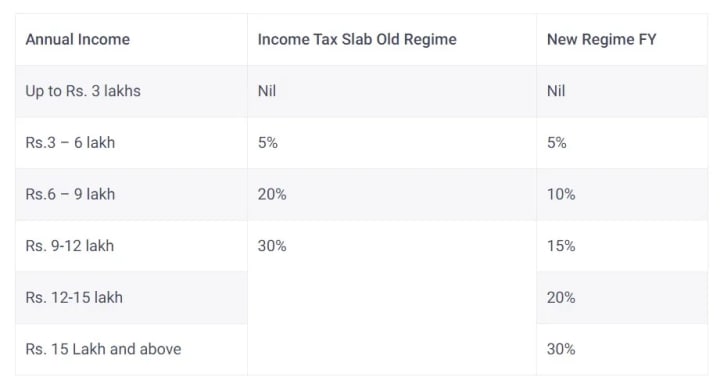

The tax exemption limit has been raised to 3 lakhs, and the new tax slabs are as follows. Here are the new vs old tax regime slab

Standard Deduction and Family Pension Deduction

Salary Income: Under the new tax regime, individuals can now avail the standard deduction of 50,000 on their salary income, which was previously available only in the old regime. This deduction, combined with the tax rebate, allows for a total tax-free income of 7.5 lakhs under the new regime.

Family Pension: Individuals receiving a family pension can claim a deduction of either ₹15,000 or 1/3rd of the pension amount, whichever is lower.

Surcharge for High-Net-Worth Individuals Cut: The surcharge rate for high-net-worth individuals with income exceeding five crores has been reduced from 37% to 25%. This adjustment results in a decrease in their effective tax rate from 42.74% to 39%.

High Leave Encashment Exemption: The exemption limit for non-government workers has been significantly increased, rising eightfold from 3 lakhs to 25 lakhs.

Old Tax Regime

The tax system that was in place prior to the introduction of the new regime is referred to as the old tax regime.

This system offers approximately 70 exclusions and deductions, including HRA and LTA, which can help lower your taxable income and reduce your tax liabilities.

One of the prominent deductions available under the old regime is Section 80C, which allows individuals to reduce their taxable income by up to Rs. 1.5 lakh.

Moreover, taxpayers have the flexibility to choose between the existing and new tax regimes based on their preferences and financial circumstances.

List of a Few Exemptions and Deductions in Old Tax Regime Slabs

Here is a list (not exhaustive) of exemptions and deductions available under the old tax regime:

- Leave Travel Allowance

- House Rent Allowance

- Standard deduction of Rs 50,000 for salaried individuals

- Deductions under Section 80TTA/80TTB for interest from savings account deposits

- Entertainment allowance deduction and professional tax (for government employees)

- Tax relief on interest paid on home loan for self-occupied or vacant property under Section 24

- Deduction of Rs 15,000 permitted from family pension under clause (ii a) of Section 57

- Tax-saving investment deductions under Chapter VI-A (such as 80C, 80D, 80E, 80CCC, 80CCD, 80DD, 80DDB, 80EE, 80EEA, 80EEB, 80G, 80GG, 80GGA, 80GGC, 80IA, 80-IAB, 80-IAC, 80-IB, 80-IBA, etc.)

- Deduction under sub-section (2) of Section 80CCD for employer’s contribution to NPS

- Deduction under Section 80JJAA for new employment

It is important to note that if the employee’s contribution to EPF and NPS exceeds Rs 7.5 lakh in a financial year, it may be subject to tax.

List of Significant Exemptions Enclosed in the New Tax Regime

- Retrenchment compensation,

- Income from Life Insurance,

- Agricultural Income,

- Standard reduction on rent,

- VRS proceeds up to Rs 5 lakhs,

- Leave encashment on retirement,

- Death cum retirement benefit,

- Money obtained as a scholarship for education, etc.

Difference Between Old Vs New Tax Regime: Which should a person choose?

Deciding between the old and new tax regimes can be challenging as there is no definitive answer as to which is better.

The selection of whether to switch to the new tax regime or remain in the old regime depends on various factors, such as the deductions and exemptions available in the previous tax system and the potential tax savings they offer.

Ultimately, it is crucial to evaluate your specific financial situation, consider the impact of deductions and exemptions under both regimes, and make an informed decision based on your individual tax planning needs and goals.

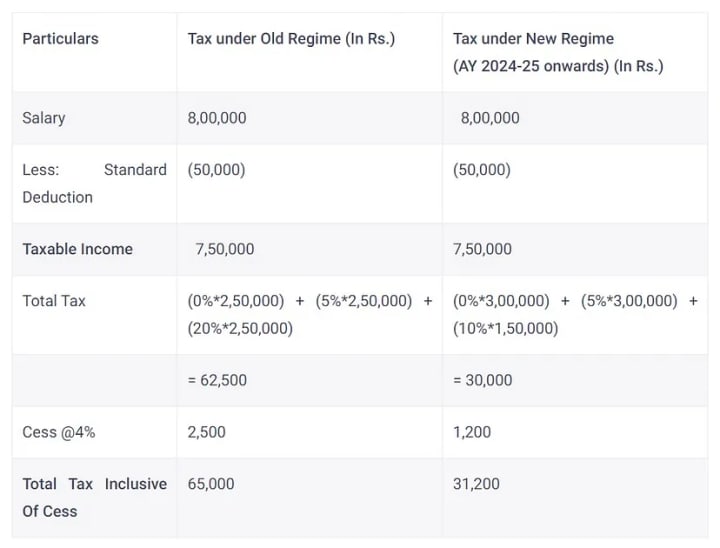

Old Vs New Regime Example

Suppose an individual has an income of Rs. 8,00,000. The following table shows the tax calculation under the new and old regimes:

Tax: Old Regime vs New Regime

When it comes to deciding between the old and new tax regimes, here are some estimates that can help:

The new regime is advantageous when total deductions are below 1.5 lakhs.

The old regime is beneficial when total deductions exceed 3.75 lakhs.

When total deductions fall between 1.5 lakhs and 3.75 lakhs, the choice depends on your income level.

Summing Up Old Tax Regime Vs New Tax Regime

In summary, the difference between the old and new tax regimes is a common concern. The new regime is suitable for individuals who prefer fewer deductions and wish to avoid the burden of extensive tax preparation.

This may include non-salaried taxpayers and older individuals without employment pensions.

On the other hand, senior citizens who rely on significant interest income can benefit from the old regime, as they are eligible for the INR 50,000 standard deduction and the newly introduced Section 80TTB.

Both the old and new tax regimes have their advantages and drawbacks. The old regime encourages saving habits, while the new regime benefits individuals with lower income and fewer investments, resulting in fewer deductions and exemptions.

The new tax system offers simplicity and reduced potential for tax evasion, as it requires fewer records.

However, since everyone has their unique set of deductions and exemptions, it is important to compare the two regimes to determine the best option for each individual.

Follow on Vocal Media ✍ : https://vocal.media/evelyn-taylor

About the Creator

Evelyn Taylor

A front-end enthusiast and dedicated development engineer, eager to expand knowledge on development techniques and collaborate with others to build exceptional software solutions.

Keep reading

More stories from Evelyn Taylor and writers in Journal and other communities.

Why MEAN Stack is Your Best Bet for Enterprise-Level Applications

"In the fast-evolving digital landscape, enterprises constantly seek technologies that can streamline development processes and enhance business efficiency," says Cache Merrill, Founder @ Zibtek, a MEAN Stack Development Company. The MEAN stack—MongoDB, Express.js, AngularJS, and Node.js—offers a compelling, modern approach to building robust and scalable applications. Its unified use of JavaScript across both the client and server sides simplifies development and speeds up deployment, making it an ideal choice for enterprise-level applications. Here's why the MEAN stack stands out as a preferred technology for enterprises.

By Cache Merrill2 days ago in Journal

Vale Perficientur

"My tears need a minute to find the edges of my face. If you'll please excuse me." The sarcasm stabbed into Juliana’s heart. Antonia glared at her from the pit of the Lyceum as her student fought to hold back tears that had nothing to do with the pain in her fingers. “You’re better than this, again.”

By Matthew Fromm4 days ago in Fiction

Comments

There are no comments for this story

Be the first to respond and start the conversation.