How neobanks are defining the future of banking

The whole BFSI industry and the world have undergone a faster transformation in the last two years than in the previous decades combined, and most likely, will continue to do so in the future.

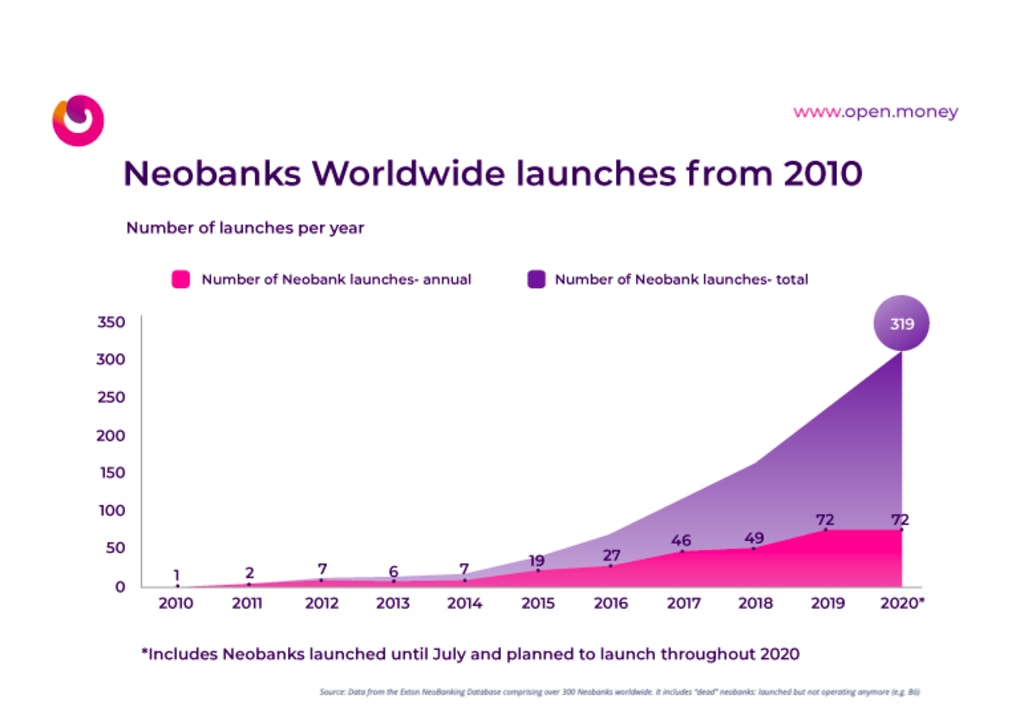

Neobanks have received significant attention but also massive investments from venture capital firms. Neobanks globally raised more than $12 Billion in 2021, despite the global economic slowdown due to Covid 19. Funding of this scale is not limited to geographical boundaries. The number of digital-only banks has risen from 250 in 2020 to 333 in 2021.

One cannot help but wonder what is in store for the future of neobanks. How are they going to evolve? But before that, we should understand what pushed neobanks to grow at such an astronomical rate and the global trends that will carve the future of neobanks.

The Rise of Neobanks

The whole BFSI industry and the world have undergone a faster transformation in the last two years than in the previous decades combined, and most likely, will continue to do so in the future. Covid 19 presented immense opportunities to the Finance/BFSI industry during the turmoil. The last two years of the pandemic undoubtedly forced people to stay indoors and asked banks and financial institutions to rethink their modus operandi.

Economic uncertainties, increased competition from digital-only banks, rapidly changing customer requirements, and fast-developing technology completely changed the banking ecosystem, forcing traditional banks to reprioritize their long-term vs. short-term goals. However, what underpins a conventional bank becomes part of the resistance to required transformations, such as – high operating costs, the burden of back-office operations, limiting banking processes, resistance to change old ideologies, and outdated systems.

Cause of disruption in banking Space - Open - Neobank

“Pandemic fallout has made the traditional retail banking environment even more demanding. For incumbents to remain relevant, now is the time to embed finance within customer lifestyle and embrace platform-based models — procrastination is no longer an option.” – John Berry, CEO of the European Financial Management Association (EFMA) in World Fintech Report 2021.

Neobanks – a new hope in turbulent times

The 2008 recession gave birth to a new brand of banks driven by technology. The year 2009 saw Aldermore, the first bank of this kind. These banks moved from brick and mortar to digital-only (fintech with a banking license and providing banking services over the internet) or challenger banks.

By 2010, a new crop of fintech came up; they called themselves the Neobanks. They focused mainly on the underserved population and provided banking through licenses from conventional banks.

Irrespective of all the developments, it was business as usual for traditional banks till things started going awry when the pandemic hit the world in 2019. They had to digitize their products and services in the shortest possible time. It led the conventional banks to launch or improve the services of their pre-existing digital-only subsidiaries.

When you look at the above situation, there are three ways to create a digital bank. They are:

Greenfield: A completely new entity with a new infrastructure and a banking license offering innovative products and services is called Challenger Banks.

Bluefield: A new entity using a mix of new and acquired infrastructure offering a blend of products and services. They are more likely to leverage the banking license of a traditional bank. They became the Neobanks.

Brownfield: A traditional bank subsidiary leveraging its resources to deliver products and services to its customers digitally. They became the digital subsidiary of conventional banks and are essentially digital spin-offs of traditional banks.

3 ways to setup Digital banking Unit - Open - Neobank

Neobanks are financial technology solution providers capable of providing a suite of banking solutions to a highly targeted niche. They offer banking services in partnership with an established traditional bank.CLICK TO TWEET

Thus, traditional banks had to dig deep to digitize their products and services quickly. While they tried to rise to the opportunity, there was a considerable gap in the market up for grabs for the third parties to enter this space.

For more information related to Open-Neobank,

About the Creator

Enjoyed the story? Support the Creator.

Subscribe for free to receive all their stories in your feed. You could also pledge your support or give them a one-off tip, letting them know you appreciate their work.

Keep reading

More stories from Anitha Raj and writers in Journal and other communities.

Everything you need to know about Open’s Corporate Cards

Corporate cards are now growing in popularity, thanks to the efficiency and flexibility they offer. Not to mention, using corporate cards makes life easier for everyone – be that of an employee, or an accountant or you, the business owner.

By Anitha Raj2 years ago in Journal

181 Keeping Watch

Each day she watched through her window. Watched? Perhaps an exaggeration: a monochromatic nuclear aftermath remaining of the world, blurring into a blindness--loss of contrast and depth of field. Achromatic aberrations displayed a waste-scape stratified in grays.

By Gerard DiLeo2 days ago in Fiction

Comments (1)

Informative content, thanks! Can I share your ideas in my article on neobank development? Here: https://www.cleveroad.com/blog/how-to-create-a-neobank/ With reference to you, of course!