Stocks - This Time For Africa

How Africa could be the next Asia on the stock market.

Investors still shy away from investing in Africa. Rightly so? How many opportunities and risks the continent offers.

Africa - the next Asia?

There is potential in this continent. That's what it says again and again when Africa is mentioned, and has been for decades. And indeed, the continent is home to the fastest growing countries in the world, both demographically and economically. Rwanda, for example, has at least recovered economically after the devastating genocides of the 1990s and is considered a prime example of progress and stability. In 2019 the economy of the republic grew by almost 10%. Countries like Ethiopia, Kenya, Nigeria and Djibouti can look back on similar figures.

Africa's economy is growing rapidly, which also has to do with the fact that the population is very young. Nearly half of all Africans are currently under 20 years old, which means that the majority will be of working age in a few years. In Germany, for example, these times are long gone: Only 18% of society in this country is under 20 years old.

The fact that a young population can be the basis for an economic miracle was recently demonstrated by the world power Asia: from 1970 to 2010, the proportion of working people here was as high as in a few years in Africa.

Growth is not homogeneous

In no other continent, however, is the economic output distributed as unevenly as in Africa. While economies such as Nigeria, Kenya and Rwanda are in the digital fast lane and are attracting more and more foreign companies that want to participate in the tech boom of developing countries through direct investment, other regions have been stuck in economic crises for years. This applies to Sudan, Eritrea and Cameroon, for example. In terms of education, infrastructure and prosperity, the differences between the 54 countries are in some cases huge - which is why the continent cannot be regarded as a homogeneous region from an investor's perspective.

So far, the few international investors have focused their attention primarily on South Africa. The economy is the most developed of all African countries, offering a good infrastructure, a modern banking system and good conditions for start-ups. Despite its comparatively weak economic growth (1.1% in 2019), South Africa is considered a market of the future, especially in the field of renewable energies. Johannesburg in South Africa is also home to the continent's most sought-after stock exchange, the JSE.

Companies to have mainly dared to go to Africa

So far, it is mainly companies that believe in Africa as the next future market. In many countries the purchasing power is growing and a new sales market has developed: The demand for new living space, new technologies and a functioning infrastructure is growing steadily - according to forecasts, 2 billion people are finally expected to live on the African continent by 2050. Some 850 German companies have now discovered the market for themselves, including Bayer and Siemens, but also carmakers such as Daimler and Volkswagen, which have production facilities there. And in other European countries, such as France and the Netherlands, there are also individual companies that are venturing into Africa. Overall, however, there is still a great deal of reluctance - and that is hardly surprising, since issues such as the rule of law and transparency are still foreign words for many governments.

However, the advances of the Western world are nothing compared to the mega plans China is pursuing on the continent. As part of its "New Silk Road", the largest expansion project of the 21st century to date, China has now settled more than 10,000 companies in Africa and invested billions in new airports, hospitals, roads and schools. The extent to which the continent benefits from Chinese investments is a completely different question that has been the subject of controversial debate for years. One of the main points of criticism of the Western world: China's expansion policy is creating new dependencies - in some cases there is even talk of a new era of colonization. Without going into the details at this point, at least in the case of Africa it can be said that this is the case: The money is only borrowed, many African countries are drowning in debt, and Chinese workers in particular are employed in the companies.

There is another country that does not shy away from investing its money in Africa: Norway. The state fund there has invested heavily in the continent for almost ten years. Initially only in South Africa, later the investments were extended to the north: After Kenya and Nigeria, Ghana and Mauritius, Morocco, Egypt and Tunisia.

Africa on the stock exchange: almost all countries are Frontier Markets

The fact that Africa consists almost entirely of developing countries does not bother the Norwegian government. Only two countries (Egypt and South Africa) count as emerging market economies according to Morgan Stanley's classification and thus fall within the emerging markets. The remaining countries remain in the Frontier Markets and have not yet reached the status of emerging markets.

The focus is on commodities - but not entirely

Africa has more natural resources than any other country: In addition to cocoa, coffee and oil, most mineral resources such as diamonds, gold and platinum are stored here - all raw materials, by the way, without which the tech industry would be completely lost. In any case, it is hardly surprising that commodity stocks dominate the African stock markets - but not only. Many industrial stocks and, for some years now, an increasing number of tech companies such as the Kenyan mobile phone provider Safaricom are also listed there.

Indices, funds, ETFs: What can private investors invest in?

The African capital market is still difficult to access, especially for private investors. The biggest hurdle is the trading centers: Nearly 75 South African shares are also traded on German stock exchanges, including the Cape Town-based media group Naspers, the Johannesburg-based industrial company Sasol and the finance company Discovery.

Occasionally, the stocks have been able to shine with strong developments: Naspers, for example, posted a performance of plus 31% last year alone. The fact that shares can slip just as enormously goes without saying. And in a country plagued by political uncertainties or natural disasters, the risk is all the greater because economic conditions in the country can change from one day to the next.

The choice of Africa funds is much greater, but most of them are actively managed funds such as Bellevue BB African Opportunities and JPM Africa Equity.

Especially in niche markets, investors have the opportunity to invest through so-called index certificates. Just like ETFs (index funds), they replicate an index almost exactly, are inexpensive and quite easy to trade. However, there is a decisive difference: With an index certificate, the investor becomes much more of a lender, which means that the investor bears the full issuer risk. The capital in ETFs, on the other hand, counts as special assets, so the investor does not have to fear losing his money through the bankruptcy of the issuer.

However, the choice of ETFs on African indices is - let's say - sparse. So far, only two ETFs are tradable in this country:

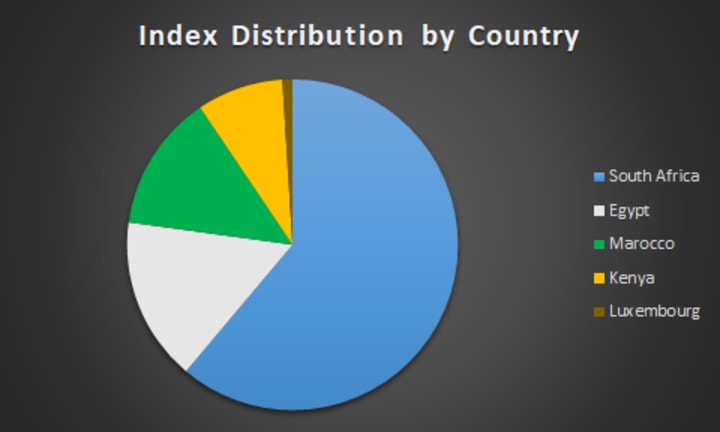

The Xtrackers MSCI EFM Africa Top 50

The ETF represents the continent's 50 largest companies and is still quite inexpensive with a total expense ratio of 0.65%. The index fund mainly includes financial and communication services (together almost 53%), and also focuses on South Africa. Nearly 62% of the investments flow there, the rest is spread over Egypt, Morocco, Kenya and Luxembourg (0.98%).

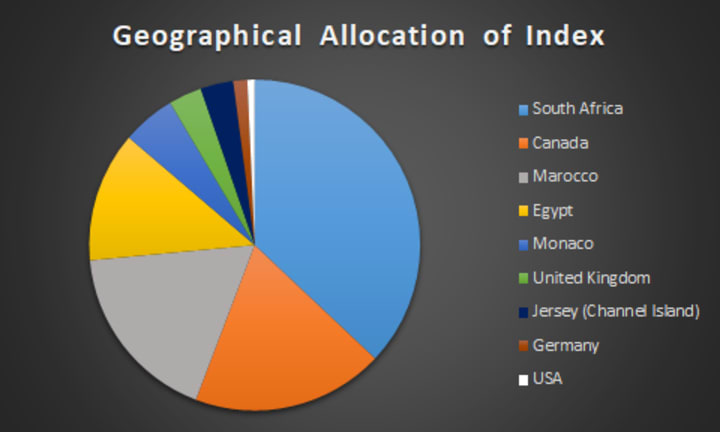

Pan Africa UCITS ETF

The other ETF eligible for savings plans is the Pan Africa UCITS ETF from Lyxor. This index fund tracks the ten largest companies from each of the three regions of Africa (North Africa, sub-Saharan Africa and South Africa), i.e. a total of 30 stocks.

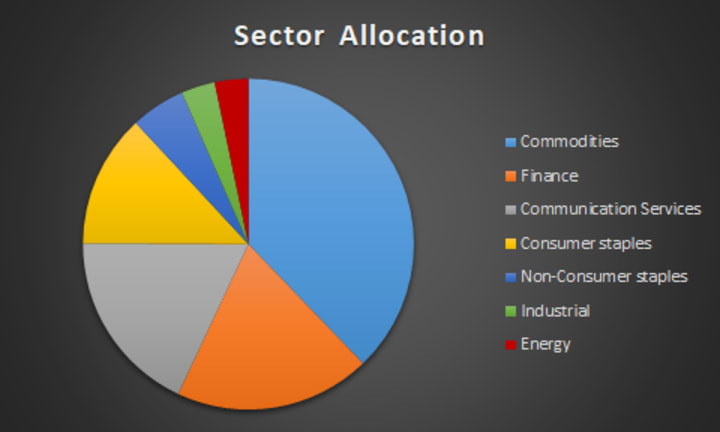

Apart from the fact that 30 values alone do not really mean a spread of risk, the values are also distributed quite one-sidedly: More than 40% of the total value is made up of raw materials and supplies, while finance and communication services together account for slightly more than 50%. The ETF also invests primarily in South Africa, and to a small extent even in Europe and the USA.

Both funds are very small: Xtracker's MSCI EFM Africa Top 50 contains just EUR 24 million, while Lyxor's Pan Africa is worth around EUR 34 million. The fluctuations may seem high at 30% and 29.4% in one year - but the DAX, for example, fluctuates by almost 33% in one year and the MSCI World by 27%.

Return on Investment

In terms of returns, both index funds have - let's say - performed modestly.

The MSCI Top 50 ETF was able to post strong gains at times, but has lost almost 12% in value on average over the past five years. In the last six months, the index has recovered somewhat from the initial setbacks caused by the corona pandemic, but is still far from its pre-crisis level.

Anyone who invested in the Lyxor Pan Africa UCITS ETF - Acc five years ago could at least make a profit, albeit not a great one: The index rose by almost 22% on average, and in some years (2016) even by 35%. However, compared with the price developments of world indices such as the FTSE All World or the MSCI World, which have been able to achieve returns of 50% or more in five years, the balance is quite sobering.

Risks

While developed industrial nations like Germany can look back on quite stable economic growth, on the African continent everything can change very quickly and the economy can plunge into recession within a few weeks. In many cases, this is triggered by political unrest: South Africa, for example, was able to shine with economic growth of around 4% until the 00s - then things went downhill. Corruption, strikes and production losses have cooled down growth considerably to this day. Until shortly before the outbreak of the corona pandemic, annual growth was only about 1%. The economic fluctuations are also immense in Libya in the north. Civil war has been raging there since 2011 and the economic development is correspondingly uncertain. In some years the economy collapsed by up to 60%, in others it increased by more than 26%. Such fluctuations also affect the stock market - profits can be high, but losses can be equally devastating.

Other African countries have also been experiencing civil war for years, for example in northern Mali, southern Sudan and Nigeria. In addition, legal certainty is still a foreign word in most African countries, which discourages many investors. Many governments do without transparency, so investors can hardly rely on the fact that contracts they have concluded are binding or that they will not fall victim to corrupt machinations or distortions of competition.

Corruption and rule of law

Speaking of transparency: As far as corruption in the country is concerned, the continent is worse off than any other: Somalia, Southern Sudan, Sudan, Guinea-Bissau and Equatorial Guinea occupy the last of the 180 places in the Transparency International ranking. In other African countries (Rwanda, Namibia, Botswana and the Seychelles), structures have improved in recent years. The good news is that Europe (and Germany) is increasingly interested in opening the African market for German investors and improving the framework conditions for investment. The "Compact with Africa" initiated by the German government, for example, should contribute to this. A treaty with several African countries that provides for reform programs and support measures.

High dependence on commodity prices

The fact that many funds and ETFs are dominated by commodities as a sector has two disadvantages: not only are investments so little spread across different sectors - there is always the risk that the prices of one or more commodities will collapse. For example, just as low oil prices are currently putting many African countries in trouble, cocoa, coffee or gold prices are repeatedly seen to fluctuate sharply, which can ultimately drag down entire indices.

Currency risks

As with all investments abroad, there is always a currency risk when buying African shares, i.e. if the foreign currency loses value before a share is sold, the investor will end up making less return than expected.

Conclusion: It is worth considering

Foreign investors do not have it easy on the African capital market. Especially because they have hardly any access to it. However, those who want to take advantage of the few opportunities should always bear in mind that most countries are developing countries whose stock markets are anything but liquid. The fluctuations can be extreme and without expert knowledge or contacts in the country it will hardly be possible to assess the risks of individual securities.

Nevertheless, there is potential in the continent that could perhaps actually develop into something like the next Asia. The population is young and motivated and in many places technically up to date. If you want to reduce the high risk, you can use African stocks or ETFs as an excellent supplement to cushion any fluctuations. After all, the frontier and emerging markets often move against the indices of the industrialized nations.

Only very few of the many up-and-coming tech companies from Africa are listed on stock exchanges, let alone in German trading centers. If at some point it should happen that even the brave startup founders of today make it to the international trading centers, then this would be welcome not only from an investor's perspective. It would also otherwise be good news for the continent, which has been trying for decades to free itself from its dependencies.

About the Creator

Keep reading

More stories from Benji Antos and writers in Trader and other communities.

Why Network-Marketing won't be the future

By now, most people are familiar with the term "Network Marketing", or at least have heard of it. Offering the possibility to "create your own business", Network-Marketing, or Multi-Level-Marketing (MLM), has made a name for itself as one of the biggest Money-Generators of the current century. But how long will this system be relevant? Will it surpass everything else in the next years? Or will it just disappear and never come back?

By Benji Antos4 years ago in Journal

Why does Network Marketing AKA Multi-Level Marketing (MLM) has such a negative reputation ?

Network marketing, also known as multi-level marketing (MLM), has indeed garnered a negative reputation over the years. Let’s explore some reasons behind this perception:

By Allwyn Roman Waghelaa day ago in Trader

Reaching Out

I promise her. I'd do anything for her. She's my mom. Even as Lanie and Deanna are flying home, Mom is scrappy fighting dying. She lays too still in that too-big bed with all the toasty white hospital blankets, in the south tower, at the broad end of a long slow-turning corner that delivers me again to her private room with the view she can't see through, with the beeping that tells us nothing new, and all these ice chips she can't swallow, and a flood of well-intentioned nurses who cannot do a damned thing all the same.

By Christy Munson5 days ago in Fiction

Comments

There are no comments for this story

Be the first to respond and start the conversation.