Molson Coors: Looking To Turn The Corner With Dividends Resuming In 2021

Regular readers will be aware that Molson Coors ( TAP) was plagued by problems long before COVID

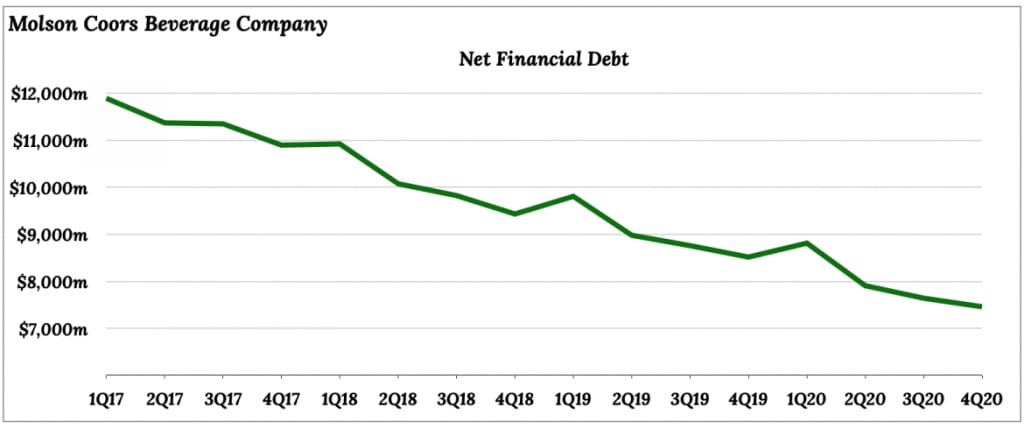

Regular readers will be aware that Molson Coors ( TAP) was plagued by problems long before COVID. These issues can be summarized in two main points. First, the company borrowed a lot to purchase the MillerCoors JV. At its peak, the company's net debt was approximately $11.5b. This is roughly equivalent to 4.5-5x annually EBITDA. This necessitated a period deleveraging to bring the balance sheet back in good shape. The good news was that Molson was generating over $1b per year in post-dividend cash flow. So while it may seem like a large amount of debt, the path to reducing it was very straightforward. Between 2016 and 2019, net debt fell by $3b.

The company's second problem is the secular decline in core product category sales. People don't drink beer as much as they used to. This is especially true for younger people. Molson and other mainstream lager brands have felt the pinch. Brewers have a lot to pay for fixed costs. The biggest advantages they enjoy often come from volume. This means that they also have a lot more operating leverage. In other words, a drop in volume would result in a greater loss of profit. The opposite is true, incidentally. You can see how money-spinner AmBev is, as it dominates certain South American markets such as Brazil.

Molson is still a decent business, despite the above. The company still holds the number 2 spot in the United States for iconic brands such as Miller or Coors. It also has some assets in Europe. The firm is a money-spinner that can produce large amounts of cash. This cash allows the firm to invest in its brands, get exposure to the best-performing parts of the beverage industry, and to pay off its debt.

Europe is Captured A Tough 2020

In Q1 last year Molson was featured here on the basis of its defensive position. Although its North American business is more heavily influenced by the off-trade, the USA didn't shut down in the same way as many other countries. Off-premise was able to generate some decent sales, as Miller Lite (the firm's largest brands) and Coors Light grew by 8.5% and 6%, respectively, in the United States. However, North American brand volume fell 5% to 61m Hectoliters. This was partially offset by the higher unit prices. In 2019, total North American sales were $8.2b, compared to $8.6b in 2019. North American EBITDA declined 2% to $1.97b.

( Source Molson Coors Q42020 Results Presentation

These were the most egregious numbers in Europe. While the firm was more exposed to the on trade there, many of these countries also imposed strict lockdowns. The Q4 numbers were worse than the whole year because of the winter shutdowns. European volume dropped 18% in 2020. Sales fell even more because of the lucrative on-trade. EBITDA for 2020 attributed to Europe fell by 60% to $126.5m.

All of this combined makes for a tough year in terms the headline numbers. Molson Coors is still able to generate a lot of cash, even though it was a difficult year. The total sales dropped nearly 9% to $9.7b. Free cash flow was over $1.1b. The underlying EPS was $3.92 per share, which is equivalent to an underlying profit of approximately $850m. In a few weeks, the firm will report Q1 2021 earnings.

Dividends To Resume In 2021

People will be familiar with the fact that Molson cut its dividend in the midst of uncertainty last year. The first quarter 2020 payment was paid out at $0.57 per share or $125m aggregated. This means that the dividend reductions have a net effect of reducing distributions by three quarters or about $370m cash.

Net debt fell by the same amount that 2020 free cash flow. The outflow from quarter one dividend was roughly offset by cash from the sale California brewery in Irwindale to Pabst. While this is a bit annoying for income investors, it did accelerate debt reduction efforts. According to management, dividends will resume in the second half this year.

Stock Is Still Cheap

At the time of writing, Molson Coors stock is trading at $52.95. This represents an approximate 40% increase over the August 2020 last time it was featured here. It has also nearly recovered all its COVID losses. It's not an unreasonable goal given the stock's strong performance, but it's what I will accept.

2021 seems to be a weak year. This situation is complicated by the fact that Europe was still experiencing difficulties with lockdowns during Q1. The revenue will still rise compared to a subdued 2020 base, and management is also planning for significant increases in marketing spending. This means another year with relatively flat profit numbers based on straight math. A quick glance at analyst estimates points to flat-ish earnings per share in the $3.90 range. Considering the dividend situation, this also means another year of decent excess cash and debt reduction.

At the risk that I sound like a broken record, I am optimistic about this name. Molson is not without its problems, with the single-digit volume declines in the core portfolio category being the most urgent. The stock trades at a price/earnings ratio just 13 so the current market prices more than reflects this. It is also focusing on positioning its beverage portfolio to better grow prospects, such as hard seltzer. The stock could deliver solid returns if Molson can stabilize its volume, maybe even 1-2% annually.

About the Creator

Keep reading

More stories from Melody Smith and writers in Trader and other communities.

VYMI: International Blue Chip Dividend ETF; Still Reasonable Long-Term Value

It's been less than a year since we first featured the Vanguard International High Dividend Yield Yield ETF here. This is essentially a sister fund to the domestic-focused VYM, the Vanguard High Dividend yield Yield ETF. Many readers will be familiar with it. The selection process is more complex than simply collecting the highest yielding stocks, despite the name. While stocks are ranked based on their 12-month forecast dividend yield, they are selected so that only half of the universe is based upon market value. Market-cap is also used to determine the weighting of each ticker.

By Melody Smith3 years ago in Trader

ONE OF THE SAFEST MICROWAVE OVEN IN THE WORLD

In the bustling hub of today's kitchens, few appliances stand as indispensable as the microwave oven. From reheating leftovers to cooking quick meals, these modern marvels have revolutionized the way we approach food preparation and convenience in our daily lives. Among the myriad options available, the BLACK+DECKER EM031MB11 Digital Microwave Oven with Turntable Push-Button Door emerges as a standout choice, combining functionality, safety, and sleek design to meet the diverse needs of contemporary households.

By Kim Long Nguyệt Ngữ6 days ago in Trader

The Business of Nature

Dew drops reflected the light of the sun. The inhabitants of Whispering Woods woke up to the golden droplets of water on the leaves of the flora. The oaks particularly enjoyed the light and the maples did, too. Happiness enveloped all who lived there, even the rocks that cried out in the night delighted in the morning.

By Skyler Saundersabout 20 hours ago in Fiction

Comments

There are no comments for this story

Be the first to respond and start the conversation.