Koho: Nearly Two Years In

At least, I think it’s been nearly two years...

Writer's Note: I believe in full disclosure. Koho has sent me a gift before, but that will not influence this review. I will be pointing out the good, and also the spots where they can improve. Also, at the end of the article, I've provided a link in case you want to sign up for Koho. That link is my referral link, and I have provided more information on it at the bottom.

So, I haven’t really had the chance to talk that much about Koho. If you, reader, follow me on Twitter, you might notice conversations that I’ve had or mentions that I’ve had with them as well. But I’ve never really sat down and said, “Hey, here’s the down low on just who Koho are, and why you need them in your life...”

Well, now, let’s have that conversation.

To help with the flow of this review, I’m going to style it like an interview.

What is Koho?

Koho is a fintech company based out of Vancouver, British Columbia. They offer similar services to a bank, but they, themselves, are not a bank. When you first sign up with them, after you place your first deposit into your account, they will send you your reloadable Visa card to use.

Wait, after your first deposit? Why not as soon as you sign up?

I thought this too for a day or two, but then I realized why that would be. They don’t want to be sending out Visa cards, that which would cost them money to print and ship out, to people who simply aren’t going to use them, full-stop. So, that’s why it’s after your first deposit that they send you the card. Think of it like an email verification.

I guess that makes sense. So, are there restrictions on the card then? Or is it unlimited?

There are certain limits to the card, yes. However, much you have on there is your limit. So, if you only have $13 on there, then it’s not going to let you spend $913. There are also caps on how much you can spend per day and how many transactions per day that you have, but as Koho improves, these limits tend to raise. It’s unfortunate that there are limits and transaction caps, but I understand, especially around the time when they were just starting out. If something happened, and suddenly someone had a transaction for thousands of dollars because their card number was stolen, Koho would not have survived that. So, cap spending. For now.

If you were to take a look at Koho, how they were back around the time they had started, and how they are now, would you say that they have improved or would you say still need a lot of work?

In the beginning, Koho was good. Not great or perfect, but good. It allowed me a bit more flexibility and a little bit more freedom to do things that I wouldn’t be able to do, such as paying my bills ahead of time immediately, versus sending it via the bank and having it take three business days for it to process, blah blah blah. But they did need a ton of work. The Visa card that they sent when Koho first started out was a swipe card. Back in 2016, they sent a Visa card that was swipe only. No tap. Not even chip and PIN. So, I didn’t really use it all that much. Mainly to pay my phone bill immediately online, but for purchases, not as much. And then, I had a bit of an issue when their chip and PIN cards first came out, so that frustrated me a bit as well. But after those issues were resolved, and as Koho as grown in users and as a company, they have improved greatly. And they have even introduced 0.5 percent cash back on most purchases made on your card.

How do they compare to competitors? Do you know of any?

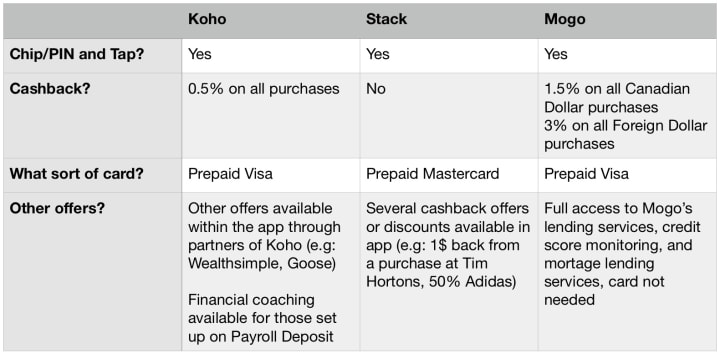

To my knowledge, there are two main competitors that are similar to Koho, and that would be Mogo and Stack. And each of the cards have their benefits and their downsides. So, below will be a small table of what each has, and doesn’t have. I will be touching down on a few things. Do they have Chip/PIN/Tap, do they offer cash back, what sort of a card do you receive, and what other offers do they each give?

Each of the cards has their own benefits, as you can see below. The only card that falls short would be Stack for cash back. Koho also is ahead because they offer preauthorized transactions on your account, so for example, if you had an account with Wealthsimple, you could connect your Koho account and use it to fund your TFSA, RRSP, or whatever account that you may have with them, and also it gives you the ability to set up a portion or the entirety of your paycheck to be loaded directly onto your Koho card. (Which also gives the ability to access their free financial coach!) Mogo and Stack do not offer this service yet.

So all in all, how would you rate Koho? Why would you recommend them over the others?

Honestly, I would rate Koho 9/10. They do have a few things to work on, such as a few front end glitches in app, and the very occasional long delay for a response in app as well, but other then that, every other time they are amazing. The app looks awesome, and the in app help is great as well. Honestly, they will make sure that whatever issue that you might have is fixed before they let you go, or if they cannot help you, they will connect you with the person from Koho that will be able to help you out. And as stated above in the table, they also offer financial coaching when you are signed up for Payroll Deposit on your account. The others don’t offer this service yet. Sure, Mogo might offer better cash back, but when you have the ability to be able to load a portion or the entirety of your paycheck onto your card, and you have an extremely knowledgable and qualified person to be able to ask how to not blow through all of your money at your fingertips... well, that gives me better piece of mind than the three percent cash back ever will.

So, if any of you guys are interested, feel free to click the link right here and sign up with them!

Full disclosure for the link: It is my referral code. Upon your first purchase, within 30 days of using the referral code, both you and I will receive a bonus $20 each, and if you set up a Payroll Direct Deposit of at least $500, no time limit, both you and I will receive a bonus $40 each. Didn’t want to be scummy and just slide in my link and not say anything. So I will always be fully transparent if there ever is a referral link or a code within a click through link.

Comparison Chart

About the Creator

Such A Geek

Not just one of us writing here, there's actually more! We will make sure to sign our names.

Keep reading

More stories from Such A Geek and writers in Trader and other communities.

The Peterson 'Paradox'

If you, like me, follow gender politics, we both may need a moment and some cannabis. If anything exemplifies, for me, the current situation in gender, it's the idea of a Thanksgiving dinner in a large family where everyone has different views and different opinions on how the turkey should be done and what choices everyone should have made, but the bottom line is that love and connection undergird the experience.

By Such A Geek5 years ago in The Swamp

ONE OF THE SAFEST MICROWAVE OVEN IN THE WORLD

In the bustling hub of today's kitchens, few appliances stand as indispensable as the microwave oven. From reheating leftovers to cooking quick meals, these modern marvels have revolutionized the way we approach food preparation and convenience in our daily lives. Among the myriad options available, the BLACK+DECKER EM031MB11 Digital Microwave Oven with Turntable Push-Button Door emerges as a standout choice, combining functionality, safety, and sleek design to meet the diverse needs of contemporary households.

By Kim Long Nguyệt Ngữa day ago in Trader

Comments

There are no comments for this story

Be the first to respond and start the conversation.