“Can Bitcoin Be Treated as a Fiat Currency?”

Is it equal to current "coins" or not?

This paper will seek to analyze whether Bitcoin, as a digital decentralized cryptocurrency, can be considered a form of money from a traditional economic perspective, and whether it may serve as an alternative to other fiat currencies. The article will split into two sections – the first will provide an explanation of the Bitcoin system, namely, its functions and origins; the second will provide analysis as to the extent to which it relates to the traditional functions of money. The paper will conclude with a summary of the author’s normative assessment of bitcoin as a form of money, and the risks its implementation as fiat currency pose.

In this first section I will present an explanation of the contemporary system of bitcoin, as well as a brief history of its origins.

Bitcoin is currently a digital asset, more and more commonly used as a medium of exchange, which uses crypto security to protect information and to control the formation of new pieces. The main feature of such a medium of exchange is that it functions sans centralized control or any form of supervision – unlike contemporary fiat currencies (such as the dollar). The system is peer-to-peer; the exchange of information between exchange participants contains the monetary value between the users. Transactions are certified by an internal network and are later integrated into a distributed ledger – a blockchain. This is an uninterruptedly expanding list of records, named blocks, which are connected and secured using cryptography. After one has obtained bitcoin, one will find that they feature similar features to fiat printed money: they have financial value, and can thus be used as a store of value, or be traded for goods and services. As with a wallet for printed money, bitcoins may be stored in a digital vault or private database that may be accessed only by the person who created it; this ‘bitcoin wallet’ may be accessed from a variety of electronic devices. It may be stored either online or offline, so as to minimize the risk of being “digitally robbed.”

As regards to the currency's origins, an online entity known as Satoshi Nakamoto is commonly known as the ‘godfather’ of the Bitcoin. It is still unknown whether this entity is composed of an individual, or a group, nor has any information come to light regarding their physical identity - they have, however, been indiscrete about their aims. In 2008, a paper published titled “Bitcoin: A Peer-to-Peer Electronic Cash System”, written by Satoshi, presented a postulated “commerce of the Internet” fully based on a system of financial entities operating through a trusted third party to process electronic transactions. They proposed, however, that the need for trust between the two transacting parties should be eliminated within this system – in favor of the provision of proof. Hence the implication that without the necessity of trust, often enforced by a supervising third party, there could be the elimination of that third party in the transaction. The real identities of the transacting parties may be kept anonymous, thus ensuring privacy – the transaction, however, would be public. Anyone may see that a transfer of bitcoin has been completed from one account to another, but the holder of the ‘wallets’ remain anonymous – this transparency would act as an incentive against deceptive deals, given that an unreliable account would be immediately seen and acknowledged as such, despite its holder remaining unknown. Such an approach is, in fact, similar to the workings of the stock exchange: the time and volume of transactions are published, but not the names of the owners of the accounts. And by 9th of January 2009, bitcoin had been born.

In this second section I will present an overview on the traditional functions of money, and whether Bitcoin provides those functions. An effective currency classically possesses three characteristics: a medium of exchange, a unit of account, and a store of value.

The first factor this paper will address concerns money’s function as a medium of exchange to settle transactions. Prior to the introduction of money, payments were traditionally done through the barter system – an exchange of goods between parties. The difficulty with such a system is the assigning of equivalent values for goods and services so that both sides are satisfied - a double coincidence of wants must occur. The chance of such a situation is, of course, miniscule. Currencies greatly diminish this issue as an agreed upon medium of exchange for all payments – most importantly, agreed upon in terms of its value.

In 2014, when the popularity of Bitcoin was beginning to grow rapidly , it was at that time still not widely used. Overstock was a single online retailer where people could buy goods - the majority of firms within it that were accepting bitcoin were software and hardware firms, providing products connected to bitcoin applications and online platforms for exchange and cryptocurrency speculation.

It has since expanded to many more branches – Overstock now allows buyers in more than 100 countries to purchase a wide range of products, from jewelry to electronics. Microsoft now provides the option for US customers to pay with Bitcoin within the Windows, Windows Phone and Xbox platforms. Dell, in collaboration with Coinbase, has allowed the use of cryptocurrencies in the purchasing of their products - currently Dell holds 4th place in the world as one of the largest bitcoin-accepting businesses. Expedia, AirBaltic, Amazon, even Lamborghini, and more are now accepting bitcoins. Yet another method by which bitcoin may be used as a medium of exchange is to convert it into gift cards, which may be accepted in several physical stores within the UK, France, Germany, and other European countries. Some utility companies now allow payment for utilities with bitcoins. "As Bitcoin usage and trading volumes increase, so does demand for reliable supporting infrastructure." The first UK Bitcoin ATM was installed in 2014, with the option of withdrawing cash through the specialized machine from your online wallet or to be transferred to your key, a kind of bit-coin debit card, before it. Insofar as the effectiveness of a currency as a medium of exchange is measured as a function of the convenience with which it may be used (which itself is a function of several variables, including its acceptance by both consumers and producers), and the extent to which it is already accepted as a means for payment, bitcoin has since made great bounds to fit the bill.

The second factor I wish to cover is the use of bitcoin as a store of value for products and services. One criticism of the currency's function as a store of value is that Bitcoin values, often being very high as compared to other fiat currencies, often requires sellers to state prices for the majority of goods within 5 or 6 decimal places. From a purely mathematical point of view, everything is correct and straightforward, but for the average customer, such small decimal numbers can be very confusing. For example, a cup of tea may cost 0.000167BTC, chicken soup may be priced at 0.000054 BTC, and sour cream at 0,000456 BTC. These may be expressed as 1, 67x10^-4 BTC, 5.4x10^-5 BTC and 4.56x10^-4 BTC, respectively. The issue for both buyers and sellers is exacerbated given that the majority of accounting software allow only for 2 decimal places in their calculations. However, as the value of the bitcoin grew and use of it around the world increased, a new derivative unit of account was proposed – that of the Satoshi, equating to one hundred millionth of a bitcoin per unit. Currently, 1 US cent is convertible to approximately 171 satoshi. This addition has simplified the value assigning process, leading to more efficient trade.

In regards to support for this function, Bitcoin has received government support from Germany in 2013, on the grounds that should it serve as a unit of account it would be taxable; however the author believes that this basis of argument has little integrity in the face of the anonymity of information inherent in the use of bitcoin, which would not allow the government to accurately or even legally tax users. Another opinion is provided by Daniel Krawisz, famous for authoring many essays about bitcoin at the Satoshi Institute: “The objection that Bitcoin is not a good unit of account actually hides a circular argument that invalidates it. Bitcoin’s utility as a unit of account depends on what you already believe about Bitcoin. If you are skeptical of Bitcoin, then it makes no sense to use Bitcoin as a unit of account. If you believe that Bitcoin will become the world currency, then it makes no sense to use anything else. You want to end up with as many bitcoins as possible, so it makes sense to price any investments or ventures in Bitcoin. That’s how you know if you are winning or losing against your benchmark. Thus, to say that Bitcoin will fail because it is a bad unit of account is to say nothing more than that it will fail because it will fail.” Another paper Krawisz published in 2016 related thusly: “An observation I made today upon investigating something interesting happening in current events is that the price of ethers as listed on ethereumwisdom.com is listed first in Bitcoin, second in U.S. dollars. This is interesting, and a little ironic (in the sense of a player in a drama who does something without understanding its full significance) because it means Bitcoin is seen as the primary unit of account for the people investing in ethers. Guess Bitcoin must not be such a terrible unit of account if that's what people are using it for.” As such, this article proposes that the primary criteria for the bitcoin to fulfill its role as a unit of account is simply that it must be widely accepted as a unit of account – echoing the circular argument put forth by Krawisz. Developing upon this, this will rely heavily on the extent of expansion of the current and relatively small community of bitcoin users - at the moment, made up of approximately 35 million wallet holders. “If people don’t use it, it will go to trash, like anything that isn’t used in this world… If people use it, then it has a future.” One somewhat radical proposition put forth to support this wider use of bitcoin as a unit of account is “for a nation with a dysfunctional currency to endorse it,” with which the author of this article completely agrees. If the cryptocurrency is implemented at national level, in such a way to allow for the citizens of a country to purchase conveniently goods and services, it would prove an indisputable argument that Bitcoin does indeed fulfill its first two functions as a form of money. It is hence difficult to determine at what point bitcoin may be fully regarded as a unit of account – problems still posed by its inconvenience within the system of the price mechanism, as well as its unacceptance by governments, all provide obstacles to its fulfilling of such a role.

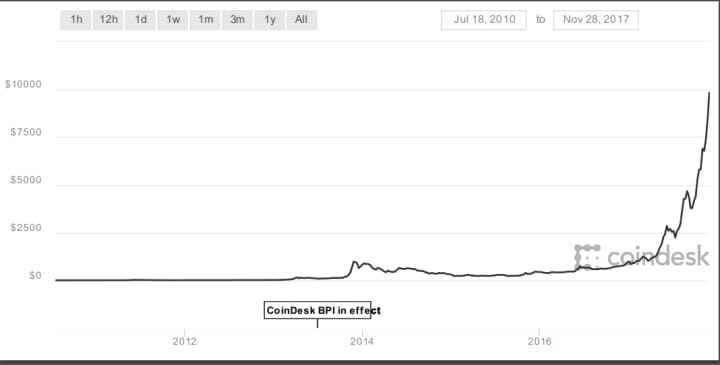

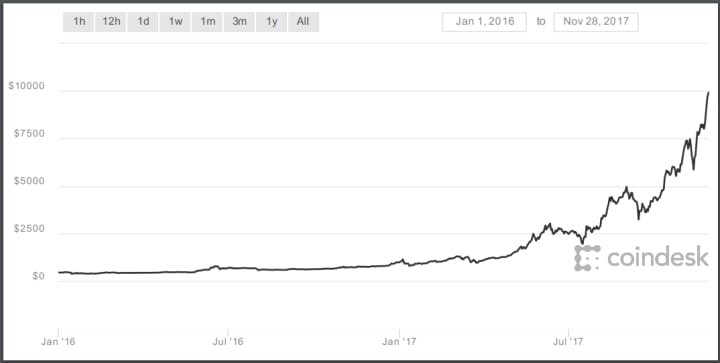

The third function of money concerns its use as a store of value. For a currency to be an effective store of value, its value as a currency must hold stable over the foreseeable future. When a currency is bought, the person buying it expects to use it in the future and receive the same real value the currency held at the time of purchase. The main issue a person holding bitcoins faces is handling the risks of bitcoin’s volatility. Figure 1 shows the price change of Bitcoin in terms of the dollar from 2009-2017. Within 8 years, its value rose by nearly 10000 dollars. In 2014, the volatility of Bitcoin was so severe that within only a minute its value could change by an average 5-7%. To take a more recent example, as of the 1st of January 2016, 1 Bitcoin was worth 447 dollars – by the 30th of December of the same year, it was valued at $960. (Figure 2). This presents a 114% rise in bitcoin value within only one year. The point that I am trying to make is that bitcoin has been a highly volatile currency since its inception; though we will see whether that volatility has changed in recent years in the analysis provided below.

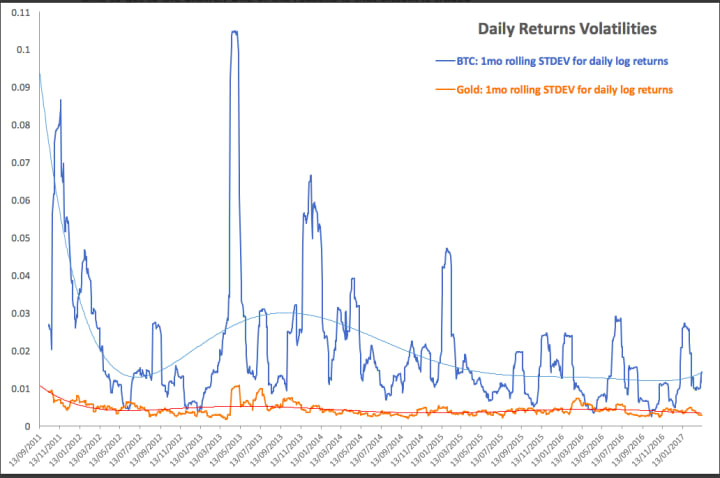

It is common practice for investors to invest in gold to hedge against the inflation of liquid currencies. I will use explanatory analysis to compare the volatility of bitcoin to the volatility of gold, and to compare the volatility of bitcoin to changes in M2. Table 4 provides plotted daily returns volatility of gold and bitcoin - it is clearly seen that bitcoin operates at far greater levels of volatility compared to gold. From 2013 to 2015, the average daily change to the value of bitcoin equated to 3.3% while the average daily change in value of gold equated to a mere 0.47%; currently bitcoin’s average daily change is held at 1.40%, with gold being a lower 0.41%. Over the last two years, the volatility of Bitcoin has decreased by a multiple of 3, bring its stability somewhat closer to that of gold’s, which has not experienced the same scale of changes during the same period, or even within the 2012-2017 period. Table 5 presents annual percentage change in M2 from 1982 to 2016. The decrease in money supply from June to August 2012 is shown to be uncorrelated with the volatility of bitcoin in the identical period of time; there is a similar lack of correlation within the October – December 2013 period. This indicates that when there is an increase in money supply of the dollar, there is no corresponding appreciation of Bitcoin, unlike gold. As such, Bitcoin cannot be held as an asset for hedging against inflation – Bitcoin resides within its own economic sphere. Macroeconomic events that affect the majority of global currencies widely used follow similar patterns, but bitcoin behavior is not at all affected. My analysis presents that Bitcoin is not an effective instrument in managing inflationary risks. In this regard, bitcoin cannot function as a store of value in the sense that it cannot ensure the maintenance of a certain value of money in the face of inflation. As such, by these criteria, bitcoin has not in recent history provided the reliability necessary to render it an effective store of value.

To conclude, as per the studies presented in this article, the main roadblock in bitcoin’s fulfillment of all three criteria of fiat money is its volatility– ensuring its unreliability as a medium of exchange, store of value, and unit of account. In this peculiar sense, bitcoin is one of the purest forms of speculative investment. In addition, so long as this volatility remains, Bitcoin risks falling into a trap of a long-term fundamental economic problem related to its supply ceiling of 21 million coins – namely, that of deflation. Should bitcoin transform into a widely accepted fiat currency, with the inability for its quantity to increase, there is significant risk of putting deflationary pressures on economies who put it into use. The example of Japan during the 90s has shown that it can be extremely difficult to move out of deflation if it becomes the norm, with falling wages and rising unemployment being a constant. As such, bitcoin in its current state may be regarded largely as an investment asset or special type of asset class - it has the potential to function as fiat money in the future, but only after issues of volatility and money supply are addressed conclusively.

Bibliography

CoinDesk. (2017). What can you buy with bitcoins?. [online] Available at: https://www.coindesk.com/information/what-can-you-buy-with-bitcoins/ [Accessed 8 Nov. 2017].

Adams, S. (2017). The Rise of Bitcoin ATM machines in the UK - Wirex Blog GB. [online] Wirex Blog GB. Available at: https://wirexapp.com/en-gb/rise-bitcoin-atm-machines-uk/ [Accessed 5 Nov. 2017].

Ten places where you can spend your bitcoins in the UK. [online] Telegraph.co.uk. Available at: http://www.telegraph.co.uk/technology/news/10558191/Ten-places-where-you-can-spend-your-bitcoins-in-the-UK.html [Accessed 3 Nov. 2017].

Satoshi (unit) - Bitcoin Wiki. [online] Available at: https://en.bitcoin.it/wiki/Satoshi_(unit) [Accessed 2 Nov. 2017].

Arthur, C. (2017). Bitcoin now 'unit of account' in Germany. [online] the Guardian. Available at: https://www.theguardian.com/technology/2013/aug/19/bitcoin-unit-of-account-germany [Accessed 5 Nov. 2017].

Christopher Burniske, A. (2017). Investigating Bitcoin: A Unit of Account – Series 4 | 5. [online] ARK Investment Management. Available at: https://ark-invest.com/research/investigating-bitcoin [Accessed 5 Nov. 2017].

RT на русском. (2017). Биткоины по соседству: в России предлагают запретить устанавливать майнинг-фермы в квартирах. [online] Available at: https://russian.rt.com/russia/article/426200-zapret-bitkoin-maining [Accessed 13 Nov. 2017]

Blockchain Blog. (2017). Bitcoin transaction fees: what are they & why should you care? - Blockchain Blog. [online] Available at: https://blog.blockchain.com/2016/12/15/bitcoin-transaction-fees-what-are-they-why-should-you-care/ [Accessed 7 Nov. 2017].

Trading 212. Free Stock Trading - Trading 212. [online] Available at: https://www.trading212.com/en [Accessed 28 Nov. 2017].

Voorhees, E. (201). The True Cost of Bitcoin Transactions - Money and State. [online] Money and State. Available at: http://moneyandstate.com/the-true-cost-of-bitcoin-transactions/ [Accessed 26 Nov. 2017].

Bitcoin - An Asset Or Currency?. [online] Available at: https://inc42.com/resources/bitcoin-currency-asset/ [Accessed 14 Nov. 2017].

New Private Monies: A Bit-Part Player. [online] Available at: https://iea.org.uk/wp-content/uploads/2016/07/New%20Private%20Monies%20-%20Kevin%20Dowd.pdf [Accessed 16 Nov. 2017].

.Bonneau .J , Miller. A . Research Perspectives and Challenges for Bitcoin and Cryptocurrencies.. [online] Available at: http://www.jbonneau.com/doc/BMCNKF15-IEEESP-bitcoin.pdf [Accessed 16 Nov. 2017].

Moore.W and Stephen. J. Should cryptocurrencies be included in the portfolio of international reserves held by the central Bank of Barbados?. [online] Available at: http://www.centralbank.org.bb/Portals/0/Files/Working_Papers/2015/Should%20Cryptocurrencies%20be%20included%20in%20the%20Portfolio%20of%20International%20Reserves%20held%20by%20the%20Central%20Bank%20of%20Barbados.pdf [Accessed 16 Nov. 2017].

Viglione, R. (2015). Does Governance Have a Role in Pricing? Cross-Country Evidence from Bitcoin Markets. [online] Available at: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2666243 [Accessed 7 Nov. 2017].

Committee on Payments and Market Infrastructures : Digital currencies. (2017). Cite a Website - Cite This For Me. [online] Available at: https://www.bis.org/cpmi/publ/d137.pdf [Accessed 21 Nov. 2017].

Hukiten.T (2014). Bitcoin as a monetary system: Examining attention and attendance. [online] Available at: http://epub.lib.aalto.fi/fi/ethesis/pdf/13626/hse_ethesis_13626.pdf [Accessed 27 Nov. 2017].

Peart, J. (2014). Undergraduate Dissertation ~ Taking Bitcoin to the Moon. [online] Academia.edu. Available at: https://www.academia.edu/7584884/Undergraduate_Dissertation_Taking_Bitcoin_to_the_Moon [Accessed 21 Nov. 2017].

Money.cnn.com. (2017). Dot.coms lose $1.755 trillion in market value - Nov. 9, 2000. [online] Available at: http://money.cnn.com/2000/11/09/technology/overview/ [Accessed 7 Nov. 2017].

Graphs

Figure 1

The figure shows the value of the Bitocoin in dollars from 18 July 2010 to 28 November 2017, from Coindesk (https://www.coindesk.com/price/)

Figure 1

The figure shows the value of the Bitocoin in dollars from 18 July 2010 to 28 November 2017, from Coindesk (https://www.coindesk.com/price/)

Figure 2

The figure shows the value of the Bitocoin in dollars from 1 January2016 to 28 November 2017, from Coindesk (https://www.coindesk.com/price/)

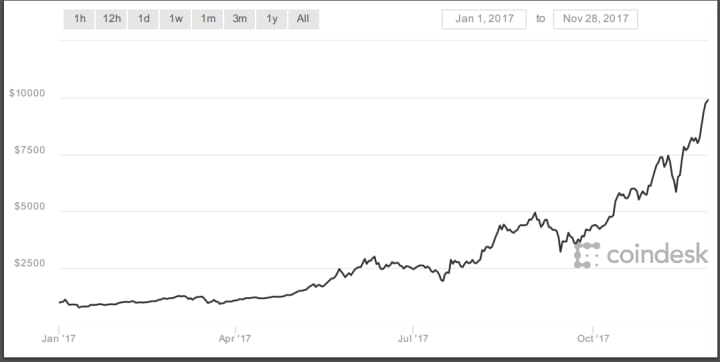

Figure 3

The figure shows the value of the Bitocoin in dollars from 1 January 2017 to 28 November 2017, from Coindesk (https://www.coindesk.com/price/)

Figure 4

The figure shows the daily returns volatility for gold and bitcoin ,for the period 13 September 2011- 13 January 2017(https://seekingalpha.com/article/4055077-bitcoin-vs-gold-volatilities-correlation)

Fiigure 5

Table shows the percentage change from year ago units, M2 Money Stock (https://fred.stlouisfed.org/series/M2)

About the Creator

Keep reading

More stories from writers in The Chain and other communities.

The Rise of NFT Projects Making Waves in 2024: Spotlight on Leading Projects

In the fast-paced digital landscape of 2024, NFTs have emerged as a groundbreaking phenomenon, revolutionizing the way we perceive and interact with digital assets. From art to entertainment, NFTs have captured the imagination of creators, investors, and enthusiasts alike. Let's delve into the captivating world of NFTs, exploring their rapid rise and the leading projects driving this transformative wave.

By Jennifer Atkinsonabout an hour ago in The Chain

Why Industries should adopt blockchain technology?

Blockchain Blockchain is transforming the way we work in the digital space with the development and launch of new-age blockchain-powered digital platforms. Blockchain is a distributed decentralized ledger bringing changes to the traditional way of working by incorporating smart contracts and removing the central authority. This makes the process work under a decentralized system which brings better security and a transparent system gaining the trust of the users. As the young generation is moving towards blockchain-based platforms it has become a necessary fact of adopting blockchain into your business.

By Lucas Andrew2 days ago in The Chain

Whispering Woods Challenge Winners

Congratulations to Morgan Christy Rickards for their winning Whispering Woods story, Guardian at the Gate. Morgan has been a Vocal creator since February 2021, and this is their first time placing in Challenge — well done, starting with a win! Guardian at the Gate draws evocatively from Welsh tales of the Cantre'r Gwaelod, a lost sunken kingdom between the forest and the sea. Heledd’s dangerous adventure pulls her towards the water but her spirit is anchored in the woods: Morgan’s writing is atmospheric and exciting.

By Vocal Curation Team7 days ago in Resources

Comments

There are no comments for this story

Be the first to respond and start the conversation.