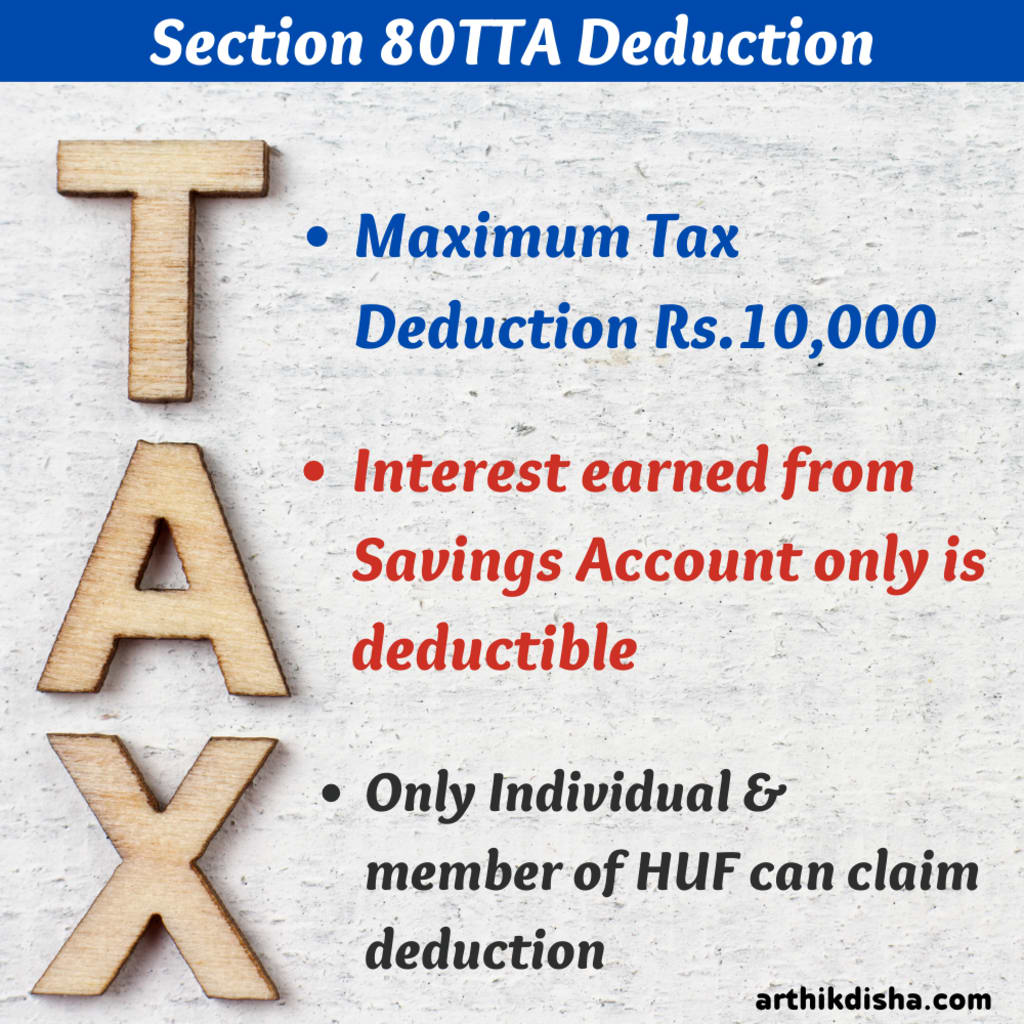

Section 80TTA Deduction-TDS on Interest

Section 80TTA Deduction

Section 80TTA Deduction-TDS on Interest

The provisions of Section 80TTA of the Income Tax Act may be read as under:-

Deduction i.r.o interest on deposits in the savings accounts as per the provisions of Section 80TTA.

Where the gross total income of an assessee (other than the assessee referred to in section 80TTB for Senior citizens), being an individual or a Hindu undivided family, includes any income by way of interest on deposits (not being time deposits) in a savings account with—

1. Banking Company: Interest earned from a banking company to which the Banking Regulation Act, 1949 (10 of 1949), applies (including any bank or banking institution referred to in section 51 of that Act);

2. Co-operative Society: Interest earned from a co-operative society engaged in carrying on the business of banking (including a co-operative land mortgage bank or a co-operative land development bank); or

3. Post Office: Interest earned from a Post Office as defined in clause (k) of section 2 of the Indian Post Office Act, 1898 (6 of 1898),

If the above conditions are satisfied the following deductions will be allowed as per Section 80TTA:

- a. in a case where the amount of such income does not exceed in the aggregate ₹10,000 the whole of such amount; and

- b. in any other case, ₹10,000.

Further where the income referred to in this section is derived from any deposit in a savings account held by, or on behalf of, a firm, an association of persons or a body of individuals,

No deduction shall be allowed under this section in respect of such income in computing the total income of any partner of the firm or any member of the association or any individual of the body.

Here “ Time Deposits ” means the deposits repayable on expiry of fixed periods i.e. Recurring Deposits and Fixed Deposits.

Applicability of deduction under section 80TTA?

Section 80TTA sets some parameters that decide deduction of tax on saving account interest up to an amount of ₹10,000 (Ten Thousand) only. So, it is very much clear that Section 80TTA allows saving of tax on interest income earned from “Savings Accounts” only.

Thus, Section 80TTA does not allow other interest income received from Banks, Financial institutions from other instruments such as Recurring Deposits, Fixed Deposits, Company Deposits are not eligible for getting the benefits of Section 80TTA deduction.

So, an individual or a member of HUF can claim deduction of tax on interest income up to ₹10,000/– received from the following:

- From a saving account maintained in a Bank;

- From savings account maintained in a Post office;

- From a saving account maintained with a Co-operative Society carrying out banking business.

Exceptions: But interest earned from Fixed Deposits, Recurring Deposits, Time Deposits maintained with Banks, Financial institutions, Co-operative Societies, Post office, are not eligible for tax deduction under this section.

Who can claim 80TTA Deduction?

As per the provisions of Section 80TTA only individual and members of Hindu Undivided Family can claim deductions of ₹10,000 for interests earned on deposits held in the savings accounts only.

Further, it should be kept in mind that 80TTA deduction is allowed for a maximum amount of ₹10,000 for interest income earned from all the savings account altogether maintained in the name of the assessee.

Is 80TTA applicable for non residents?

As per Section 80TTA, there are no restrictions on Non-residents to claim income tax exemption on interest income earned from Savings Account. However, the maximum amount of deduction is limited to ₹10,000 only combining all savings account together.

Can we claim both 80TTA and 80TTB?

The answer is simply No. As Section 80TTB is applicable for Senior Citizens only. As per Section 80TTB, a senior citizen is allowed to claim deduction Under Section 80TTB up to a maximum amount of ₹50,000 in a year, for interest income( from R.Ds, F.Ds, Time Deposits) received from A Bank, Financial institution, Co-operative Banks but not from a Company’s F.D.

So, in simple words, the Income Tax Act does not allow one to enjoy deduction both under Section 80TTA and 80TTB respectively. Senior citizens claiming deduction U/S 80TTB can not enjoy the benefits given under section 80TTA.

How is 80TTA deduction calculated?

80TTA deduction is allowed a maximum of ₹10,000 in a year for interest earned from deposits held in the savings account. This includes all savings account maintained by the assessee.

Amount of 80TTA deduction calculated as under:

Particulars of interest income for F.Y 2020-21 Amount(₹)

Interest earned on savings account from Banks 6,000

Interest from Post office savings account 5,000

Interest from F.D 5,000

Interest from Time Deposits (R.D) held with Co-operative Bank 3,000

Total interest income earned as above 19,000

The maximum amount allowed as 80TTA deduction is limited to ₹10,000

Interest Income Deduction as per Section 80TTA and 80TTB respectively

Particulars of income earned in F.Y 2020-21 Tax Payers

(Below 60 Years) Senior Citizens (Above 60 Years)

Income from the Savings Bank Account ₹ 11,000 ₹ 11,000

Income from Fixed Deposits, Recurring Deposits, and Senior citizen savings schemes ₹ 2,50,000 ₹ 2,50,000

Other Income ₹ 2,00,000 ₹ 2,00,000

Gross Total Income ₹ 4,61,000 ₹ 4,61,000

Deduction under Section 80TTA ₹ 10,000 Not Eligible

Deduction under Section 80TTB Not Eligible ₹ 50,000

Net Taxable Income ₹ 4,51,000 ₹ 4,11,000

Tax on Net Income(Rebate u/s 87A ₹12,500/-is not considered for calculation purpose) ₹ 10,050 ₹ 5,550

Add: Cess@4% ₹ 402 ₹ 222

Total Tax payable including Cess ₹ 10,452 ₹ 5,772

Maximum Deduction for Interest Income 10,000 (Section 80TTA) 50,000 (Section 80TTB)

So, from the above calculation, you can check that 80TTA deduction is allowed for a maximum of ₹10,000, subject to interest received from savings accounts only kept with Banks, Financial Institutions, Co-operative societies engaged in the business of banking.

Interest earned from RDs, FDs have not been taken into consideration while calculating the maximum permissible limit of 80TTA deduction.

But Section 80TTB allows taking deduction benefit for all interest income except Company FD.

Is 80TTA applicable on FD interest?

No. Not at all. Section 80 TTA of the Income Tax Act clearly stipulates that interest income earned from deposits held in the savings account only is eligible for income tax deduction U/S 80TTA.

Therefore, interest income earned from FD is taxable for assessee below 60 years of age. Hence, 80TTA deduction is not applicable on FD interest.

Can senior citizen claim both 80TTA and 80TTB?

It would not be a prudent decision for a senior citizen to claim deduction U/S 80TTA only for ₹10,000 as he can claim a bigger deduction U/S 80TTB up to ₹50,000 in a year.

Section 80TTB has been designed exclusively for senior citizens so that they can take the maximum benefits allowed for all kind of interest income received after their retirement at the age of 60 years.

Section 80TTB is far more superior in terms of interest income received from FD, RD, Time Deposits, whereas 80TTA is limited to only interest from the savings account.

So, the Income Tax Act does not permit a senior citizen to claim both deductions simultaneously. He can claim only a single deduction for tax on interest income.

Is 80TTA deduction 40,000?(TDS on Interest)

Finance Budget 2019 had increased the TDS on interest limit from the existing limit of ₹10,000 to ₹40,000 and for the senior citizens the limit has been enhanced to ₹50,000.

But there is a misconception among the taxpayers that the 80TTA deduction has been enhanced to ₹40,000, which is absolutely wrong.

Only the TDS on interest income i.e. the TDS threshold limit has been enhanced under Section 194A of the Income Tax Act.

This means now Banks and other financial institutions would not deduct TDS on interest income if it is below ₹40,000. Tax on interest income will be applicable only when the interest income exceeds ₹40,000 in a year.

Here it needs to be clarified that Section 80TTA deals with tax on saving account interest whereas Section 194A deals with TDS on interest income.

Section 80TTA for AY 2020-21

Of late there have been no updates in Section 80TTA. Therefore, the maximum deduction permissible under Section 80TTA is ₹10,000 for A.Y 2020-21 and also for F.Y 2020-21.

Income Tax on interest on Fixed Deposit

Income Tax on the interest income from Fixed Deposit is taxable as per the applicable tax slab of the taxpayer. There is no income tax deduction for taxpayers below 60 years of age for interest income from FD.

This means any amount received as interest income from FD, it will be treated as other income of the assessee.

This other income will be added with the gross total income and tax will be calculated accordingly as per the applicable tax slab of the assessee.

About the Creator

Arthik Disha

A Personal Finance Blogger. Passionate about finance.

Keep reading

More stories from Arthik Disha and writers in Lifehack and other communities.

10 Easy Steps On How To Write A Will In India For Free

How to make a Will in India/How to Write a Will in India Free? A Will is a legal document that ensures that the Will writer’s (Testator) wishes are fulfilled after his death. I have already written a post on What is a Will. You may go through that.

By Arthik Disha4 years ago in Lifehack

How Instagram Downloader Work and Why You Need One

In the ever-evolving landscape of social media, Instagram reigns supreme as one of the most popular platforms for sharing photos, videos, and stories. With its vast array of captivating content, it's no wonder that users often find themselves wanting to download and save their favorite posts. This is where Ig downloaders come into play. In this inclusive guide, we'll delve deep into the workings of these tools, uncovering their mechanisms, and their benefits, and ultimately understanding why they are indispensable for any avid Instagram user.

By Igstorysaver3 days ago in Lifehack

10 Reasons Why You Should Have Plain Yogurt Daily

10 Reasons Why You Should Have Plain Yogurt DailyConsuming plain yogurt daily can offer numerous health benefits due to its rich nutrient profile and active cultures. Regular consumption of yogurt as part of a balanced diet can promote overall wellness and vitality. In this article, we share the many benefits of eating plain yogurt daily.

By Kaly Johnes5 days ago in Lifehack

Comments

There are no comments for this story

Be the first to respond and start the conversation.