Will China Bounce Back in 2024?

After three years of lockdowns and economic turmoil, China is hoping for sunnier days in 2024.

After three years of lockdowns and economic turmoil, China is hoping for sunnier days in 2024.

But significant headwinds remain. The government is facing difficult decisions about how much stimulus to provide and what growth targets to set.

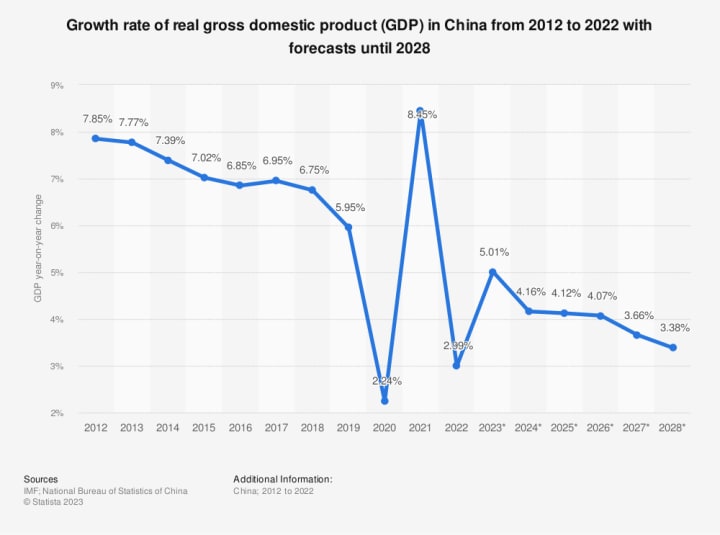

Most forecasters expect GDP expansion of around 4–5% next year, down from over 5% in 2023. Achieving even modest growth will require deft policymaking.

The property market remains China’s Achilles heel. Despite repeated government efforts to shore it up, housing sales plummeted in 2022, construction starts slowed dramatically, and developers struggled with massive debts.

These woes filtered through the economy, depressing demand for raw materials and crimping consumer spending. Although recent policy support has stabilized the sector, a quick, V-shaped rebound looks unlikely.

Most analysts expect a drawn-out recovery over several years. If pessimists are right that oversupply and demographic decline have structurally diminished housing demand, the property drag could persist.

Lacklustre global growth presents another headwind. As major Western economies flirt with recession and worldwide trade slows, external demand for China’s manufactured goods will falter.

Exports held up better than expected this year, but that resilience may not continue as the world economy cools. Russia’s invasion of Ukraine and deteriorating China-U.S. relations add further uncertainty.

On the bright side, China’s pandemic reopening and infrastructure push should buoy domestic consumption and investment.

Consumers still have pent-up demand and excess savings after years of restraint. Capital spending got a late start under the current 5-year plan but should accelerate with ample room in local government budgets. Meanwhile, tax cuts and special bonds have given a fiscal boost.

The policy dilemma facing officials is how aggressively to double down on stimulus given the mixed outlook. Growth could potentially surpass 5% with enough policy support, but that risks inflating new bubbles and adding to already dangerous debt levels. Alternatively, accepting slower growth around 4% would facilitate structural deleveraging while still keeping alive long-term doubling ambitions.

Threading the needle will require nuanced policy calibration. More infrastructure spending is needed but with tighter guardrails to prevent waste. Cheap credit for productive enterprises should continue, but tighter scrutiny of unproductive real estate lending.

China's property downturn has revealed the need for a "new normal" in the country's fiscal policies. The slump has hurt land sales, cutting off a key revenue source for local governments. This makes it harder for them to service debts of state-owned enterprises and government-sponsored financing vehicles. These contingent liabilities are materializing, as Moody's notes.

The central government wants to prevent outright default on publicly-traded bonds issued by local financing vehicles.

But it also wants to avoid a broad bailout, which would encourage reckless future lending. Although any grudging central government assistance will strain public finances, refusing help could also prove fiscally costly if defaults erode confidence in state-owned banks. For now, the relationship between China's central government, local governments and local financing vehicles remains unfinished business.

The housing market needs targeted life support, not another tidal wave of credit.

The new pillar industries of technology, renewable energy and electric vehicles are not as labor-intensive as real estate, which provides a mix of blue-collar construction jobs and white-collar careers in realty and finance. A transition period from one industrial focus to another can disrupt job and career stability.

Cai frets this labor market uncertainty will further restrain consumer spending by Chinese, who will already tend toward caution as the population ages.

In short, while China has bounced back from the pandemic, its economic challenges remain formidable.

Avoiding a protracted slowdown will demand wise policies that balance short-term support with long-term stability. Whether Beijing has the vision and discipline to walk this tightrope will become clearer in 2024.

© Buzzedison

Get step-by-step game plans to secure funding, build efficient systems, and scale your business the smart way delivered to your inbox weekly.

About the Creator

Edison Ade

I Write about Startup Growth. Helping visionary founders scale with proven systems & strategies. Author of books on hypergrowth, AI + the future.

I do a lot of Spoken Word/Poetry, Love Reviewing Movies.

Keep reading

More stories from Edison Ade and writers in Journal and other communities.

When the Robots Took My Job

This is for RM Stockton's Write Club prompt for the month of April: AI Please allow me to vent. For "college," I went to a scam school that is now closed. We were promised internships that were never spoken of again after admissions, and we were promised help finding jobs. The first time I went to the career counselor's office, she was completely frazzled. She had no idea what to do with us, the film majors. The second time I visited her office, I let her know that I'd found myself a job, and she was visibly relieved.

By Rebekah Conard5 days ago in Journal

Tyler Fogarty of Nashville talks about Building a Sustainable Supply Chain: A Guide for Eco-Friendly Businesses

Sustainability is not a fashion choice; it is a way of life that improves the quality of life and gives back to the world that we live in. Just like our personal lives, our professional lives contribute a great deal to the society around us. Many people only focus on one element and replace that with a greener substitute when discussing eco-friendly businesses. But changing a single thing about your company doesn’t make it sustainable—the whole process matters. Let’s see how to make the complete supply chain more eco-friendly.

By Tyler Fogarty3 days ago in Journal

Before Sylvester the Cat, there was Sylvester the Dog

Sylvester was a Merrie Melodies canine Sylvester, the Cat, is a beloved Looney Tunes character who debuted in March 1947 in the animated short Life with Feathers. The iconic Mel Blanc once said that he enjoyed voicing Sylvester, one of his favorite characters. The cartoon short that was near and dear to Blanc's heart was Bird's Anonymous which starred the popular cat.

By Cheryl E Preston5 days ago in Geeks

Comments

There are no comments for this story

Be the first to respond and start the conversation.