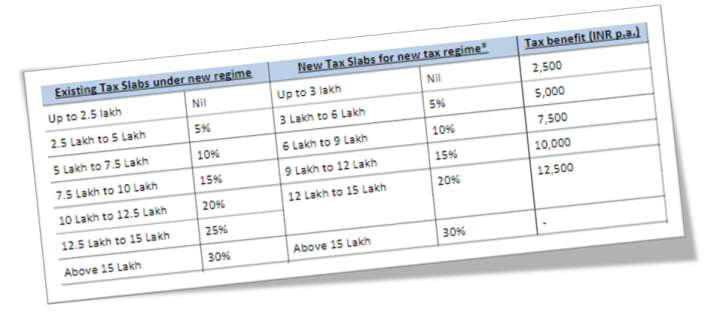

Indian New Tax Slab - 2023

How much you can save on Tax 2023?

Union Budget 2023 (Announced on 1st February 2023)

The Union Budget for 2023 was announced on 1st February 2023 by the finance minister. Highlights of proposals are given below:

The above tax slabs of the new tax regime are now default rates however anyone can still opt for the old tax regime.

Income tax deductions homebuyers get now

Currently, homebuyers can claim an income tax deduction on the interest paid on their home loan under Section 24 (b) of the Income-tax Act, 1961. The maximum amount of deduction that can be claimed is Rs 2 lakh per financial year for a self-occupied property. Homebuyers can also claim income tax deductions on the principal repayment of their home loan under Section 80C of the Income Tax Act. The maximum amount of deduction that can be claimed is Rs 1.5 lakh per financial year. However, various deductions for other investments such as Public Provident Fund (PPF), equity-linked savings schemes (ELSS), life insurance premiums, and Sukanya Samriddhi Scheme are clubbed under Section 80C of the Income-tax Act, 1961.

Expert's comment

Divya Baweja, Partner, Deloitte: As expected, the FM has proposed various changes in the New tax regime to make it more popular. Out of five major announcements made under the personal tax, three proposals have been made for middle-class salaried individuals opting for the new tax regime which are an increase in the rebate under section 87A for people earning taxable income up to Rs 7 lakh, a change in tax slab rates and introduction of the standard deduction and deduction against family pension, making the new tax regime all the more lucrative.

Akash Sinha, Co-founder & CEO, Cashfree Payments: Finance Minister Nirmala Sitharaman has presented a distinctive set of measures in the Union Budget 2023-24 with a streamlined focus on rapid, holistic and inclusive economic growth. It is a well-crafted statement of intent, drawn from the success and learnings from the past with the potential to further enhance India’s growth prospects.

Suresh Agarwal, MD & CEO, Kotak Mahindra General Insurance Company: Taking it a notch above the expectations of the middle class, the budget has a special thrust on women and youth which makes it truly citizen-centric. To remain the fastest growing major economy in the world, it demonstrates the government’s intent to improve a taxpayer’s purchasing power through income tax rebates, enhanced grievance redressal mechanism for direct taxpayers and capital deductions from capital gains on investments, while being overall fiscally prudent to address inflation. Further, rolling out a host of initiatives to support domestic industries, the budget sets positive sentiments in placing India in a resilient position amidst a global slowdown.

About the Indian Tax System:

The Indian tax system is a federal system, where both the central and state governments have the power to impose taxes. The Indian tax system is governed by the Central Board of Direct Taxes (CBDT) and the Central Board of Indirect Taxes and Customs (CBIC), which are responsible for enforcing tax laws and collecting taxes in India.

The Indian tax system includes taxes on income, goods and services, and wealth. The major taxes imposed by the central government are:

Income Tax: A tax on an individual's or company's income from various sources such as salary, business profits, interest, and rent.

Goods and Services Tax (GST): A consumption tax on goods and services, which replaced multiple indirect taxes such as VAT, service tax, and excise duty.

Corporation Tax: A tax imposed on the profits of companies.

The major taxes imposed by state governments are:

Value Added Tax (VAT): A tax on the sale of goods and services.

State GST (SGST): A tax on the supply of goods and services within a state, which is collected by the state government.

In addition to these taxes, there are also taxes imposed by local authorities, such as property tax and entertainment tax.

The Indian tax system is progressive, meaning tax rates increase as the taxable income increases. The government periodically revises tax slabs and tax rates, so it's important to keep up with any updates and changes.

About the Creator

Keep reading

More stories from Senthilkumar M and writers in FYI and other communities.

The Sweet Sensation of Bubble Tea

Bubble tea, also known as boba, is a Taiwanese drink that has become increasingly popular around the world. It is a sweet tea-based beverage that is typically served with chewy tapioca pearls. In this essay, we will explore the history and origins of bubble tea, its ingredients and preparation, and its cultural significance.

By Senthilkumar Mabout a year ago in FYI

The Bloody Blood in Your Veins

Our Origins Today, I read something I didn't know—one more thing to add to all the other things I didn't know. By the time I grow up, I’ll have a collection. But it was intriguing, and it inspired me to write this post. I hope you enjoy it.

By Rene Volpi 6 days ago in FYI

Comments

There are no comments for this story

Be the first to respond and start the conversation.