Social Security: Avoid falling for a false retirement plan

You were not supposed to get Social Security

Quick Background

I love discussing money and retirement planning with people in all walks of life (poor, rich, old, and young). I am probably a little too obsessed with it — it comes from a place of fear, yet gratitude. Growing up poor, my family and friends lacked financial literacy, and they definitely were not financially sharp.

When I was sixteen and seeking my first job, a friend's parents planted a seed by suggesting that I should save ten to fifteen percent of all my earnings towards retirement. I thought this was foolish since I was so young, but the comment always stayed in the back of my mind. It wasn't until I was nineteen, interning for a large corporation, and attended a meeting hosted by Fidelity, when my view changed. Fidelity shared information on the 401(k) and the company match. I was hooked, and that began a lifelong journey of learning personal finance.

Sparked Controversy

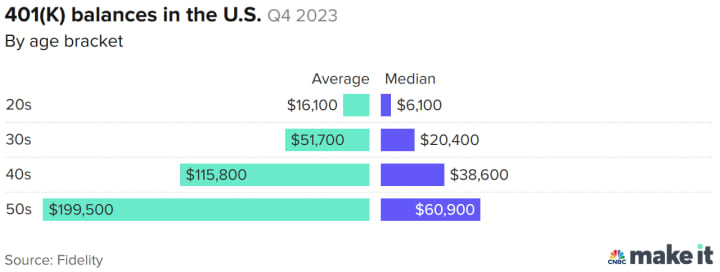

It was about a month ago when I shared information on Facebook that showed the average retirement savings by age (DeVon, 2024) and suggested that people need to invest more aggressively for their retirement because Social Security won't be enough.

I also shared that the average Social Security check is $1,658 per month — $19,896 per year — (MSN, n.d.) which won't be enough to cover most of your essentials such as housing, utilities, food, and prescription drugs. It's even worse for women than men. Average Social Security payment for women is $1,483 versus $1,838 for men.

I then pointed out that the designers did not intend for you to receive Social Security, and that you have sole responsibility for your retirement planning in this post-pension era.

That statement caused much controversy and caused splintered conversations over the next two-to-three weeks. I received messages such as:

- "I've paid into the program for over 40 years; I am owed that money."

- "You are a fool."

- "It must be nice for you to have invested money for your retirement, but we all aren't like you."

Whoa, Whoa, Whoa... Please don't hate on the messenger or the message.

But let me explain.

History of Social Security

On August 14, 1935, President Franklin D. Roosevelt signed into law the Social Security Act. You could receive Social Security payments at 65. But did you know? In 1935, the life expectancy of a man was 61.7 years old and 65.7 years old for women.

That is why I say that you were not supposed to receive any Social Security benefits.

How can a 65-year-old man expect to receive a Social Security check when he is supposed to be dead by 62? They designed the program to ensure that those who live longer are supported and to prevent your grandma from experiencing homelessness in her old age.

It was a safety net that was designed and passed as part of President Roosevelt's New Deal when senior citizen poverty rates exceeded 50 percent (Wikipedia contributors, 2024).

The intention was not for it to be your sole retirement plan and to support you for 20 or 30 years.

Previous Generations

The generations before mine, I'm Generation X, had two advantages that were helpful to them: 1) reasonable cost of living, and 2) company pension, retirement plans, and post-retirement healthcare coverage.

Kids today constantly hear and read of the stories that their grandparents could live on a single-spouse income, have a pleasant home, a car, and free-time to enjoy their family, friends and take vacation. Massive student loan debt was not something they had to be burdened with, either. Many also had the safety and security of a retirement plan as part of the Defined Benefit Pension Plans that became prevalent during the postwar economic boom.

Just a small comparison:

- In the 1950s, the median home value was approximately $7,354, mortgage rate of 4%. Adjusted for inflation to 2024 dollars, the home value was approximately $79,000.

- In 2024, home prices are $325,000 to $425,000 depending on your source (Redfin, National Association of Realtors, or Zillow Home Value Index).

Generation X and Beyond

Generation X was the first generation that has the shifted responsibility to self-fund their retirement. Many companies have moved away from offering pension plans and are now making available 401Ks, or similar, with a potential contribution match.

The Motley Fool (2017) shared that "79% of Americans work for an employer that sponsors a 401(k)-style retirement plan... [but] not everyone who's offered an employer-sponsored plan actually takes advantage of it. Of those 79% of Americans who get the choice to fund a 401(k), only 41% opt to participate. As such, just 32% of the total workforce is saving in a 401(k)" (Backman).

And if they are taking part, they may not be saving enough. Currently, GenX has a median balance of $38,600 in their 401(k).

Why is this a concern?

Retirement Scare

Mentioned above, the average Social Security payment for women is $1,483 per month versus $1,838 for men. If that married couple enters retirement, they will have approximately $3,321 per month ($39,852).

The Bureau of Labor Statistics (BLS) estimates $4,220 in monthly spending ($50,640) for Americans that are age 65 or older. That leaves a yearly gap of nearly $11,000. Where is that money going to come from? Equity in your house? Family? Friends?

To cover that gap, you will need a minimum of $275,000 in your retirement plan (expenses X 25 is the general rule). That will allow you to draw 4% ($11,000) every year.

Let's say you were diligent and saved up $275,000 in your retirement savings. That is amazing! Maybe you are living a comfortable life. It is not extravagant, but you are getting by comfortably.

What happens when your spouse dies? At that point, you will lose one of the two Social Security checks (whichever is lesser). The living spouse now has $50,640 in yearly expenses but is only receiving $28,796 in benefits ($17,796 from Social Security per year and $11,000 per year from retirement). This is a significant gap of $21,844 per year.

Now what? Maybe there is equity in the house? Will you have enough equity to pay for 5, 10, or 20 years of living expenses? Maybe you increase your withdraw rate from your retirement plan? How long will that last?

Many will need to consider selling their house and moving in with their siblings or son or daughter.

Preparing The Next Generation

For someone that is graduating High School (18 years old) or College (22 years old), time is your greatest asset. There are two unknowns that you need to provide estimates for to begin your plan: 1) How much do you need, and 2) Will Social Security be around in 2060? Let's not count on Social Security (it goes back to my philosophy of not relying on the government).

If living expenses are $50,640 today, you will need to plan on $154,000 in 2069 (adjusted for inflation at 2.5% per year). In 2069, you will retire at 65 years old. As such, you need to have $3,850,000 in a retirement plan ($154,000 X 25 and then you can withdraw 4% when you retire).

Since its inception, the S&P 500 index has returned an average of 9.82%. Using 9.82%, you will need to invest $545 per month from 22 years old until 65 years old (43 years).

Relax! This is just a north star to get you thinking in the right direction. Too many people don't even think of these things until they are in their 30s or 40s, when it is getting late to make significant growth in their investments.

Will you really need $154,000 per year in living expenses? Maybe not. Will Social Security still be around? Most likely. If we estimate $1,500 per month in Social Security Benefits, then you only need to invest $475 per month because you only need $3,400,000 versus $3,850,000 in your retirement account. Then, there are things like a company 401(k) match which will absolutely help. This could probably get your monthly investments to $250 to $400 per month.

Do Not Stress... Just Start!

It is extremely easy to get stressed out about this. Do not stress. If you are 18 years old, open a brokerage account and start with $10 or $20 per month. As you get older, increase your contribution. The primary goal from 18 to 22 is to just build an investment habit. This is not hard.

Even if you miss the target, or the target is too much, you can recalibrate during major life changes such as getting married or professional promotions. Maybe you only save $1,000,000 or $500,000. Is it better to come up a little short versus having nothing saved at all?

Always think of a North Star Target

(Estimated Yearly Living Expenses minus Estimated Yearly Benefits & Income) X 25

You Can Do This

I am so passionate about your future and believing that you can do this. I have also shifted my graduation gift strategy for my loved ones to help jumpstart their retirement plans. You can read about it from my post, A Different Graduation Gift.

Just get started today! And remember my personal slogan:

Do not rely on your family, your friends, or the government to take care of yourself when you can no longer work, such as if you lose your job, or need to stop because of health issues.

References

DeVon, C. (2024, March 28). How much money Americans in their 50s have in their 401(k)s. CNBC. https://www.cnbc.com/2024/03/28/median-401k-balances-for-americans-in-their-50s.html

Backman, M. (2017, June 19). Does the Average American Have a 401(k)? The Motley Fool. https://www.fool.com/retirement/2017/06/19/does-the-average-american-have-a-401k.aspx

Horsley, S. (2024, May 6). The clock is ticking to fix Social Security as retirees face automatic cut in 9 years. NPR. https://www.npr.org/2024/05/06/1249406440/social-security-medicare-congress-fix-boomers-benefits

MSN. (n.d.). https://www.msn.com/en-us/money/retirement/here-s-the-averagefoxsocial-security-check-for-men-vs-women/ar-AA1crecW

Wikipedia contributors. (2024, March 27). History of social security in the United States. Wikipedia. https://en.wikipedia.org/wiki/History_of_Social_Security_in_the_United_States

Disclaimer

I am not a certified financial planner, and any financial numbers and strategies are for discussion only. Seek professional advice from accountant and/or professional financial planners. But do NOT use a financial advisor that wants to manage your assets for you (known as Assets Under Management at 1%+). Select a pay by hour or visit only.

Thank You

If you find this piece interesting or helpful, please consider leaving a heart, a comment, or even a tip. Your support means a lot to me as a hobbyist writer. Plus it helps with the algorithms.

About the Creator

Stephen Legler

Aspiring author writing first fiction book. I'm passionate to discuss personal finance, religion, tech & occasionally politics. I enjoy reading other people's work & getting to know folks. I play an excellent extrovert. Happy to meet you!

Keep reading

More stories from Stephen Legler and writers in Motivation and other communities.

A Different Graduation Gift

See Affiliate Link Note and Disclaimer at end of article Introduction For the last couple of years, I have changed my graduation gift strategy. Previously, I would provide the High School or College graduate with a generous check or gift cards they could enjoy. Now, I give them a smaller gift card, but also include something I believe will be more valuable to them in the long-term.

By Stephen Legler12 days ago in Motivation

Vocal & my relationship to publishing traditionally

Ever since my small writing beginnings, when I started writing on Vocal in February 2021, I had been in a truly terrible slump & funk when it came to my writing. I had so many unfinished projects, ideas, half finished manuscripts and first chapters that were going nowhere.

By Melissa Ingoldsby4 days ago in Motivation

To Provide Your Final Twenty

He strolls strangely, rearranging and almost stumbling down the corridor toward his loft entryway. I slow my speed, permitting my neighbor — a stodgy ex-marine with one missing tooth, a solid scent of alcohol and fourteen days of unwashed odor continuously going with him — to arrive at his entryway. I crease my nose, almost choking as he tarries ahead.

By Siam3 days ago in Motivation

Comments (1)

Nicely done it.