I know this will be controversial, and Dave Ramsey helped me dig out of 15k of credit card debt and learn to live debt-free, sort of. You see I have a credit score that is over 800. I have a home that is paid off, but not the one I live in. I still have credit cards and use them all the time for their rewards and pay 0% interest. Something Dave Ramsey can’t understand.

Also, Dave Ramsey is worth about $200 million and you won’t be worth that much by following the program Dave Ramsey asks you to follow. So why else would Dave Ramsey’s financial advice not be the best for you long term?

This post may contain affiliate links which means that I may receive compensation at no extra cost to you if you make a purchase from a link found on my site. Please review my privacy policy for further details.

These ideas are based on my personal experience and opinion and should not be considered professional financial investment advice. Furthermore, the ideas and strategies should never be used without first assessing your own personal and financial situation, or without consulting a financial professional.

Dave Ramsey on credit cards

When it comes to money management and getting out of debt, Dave Ramsey is a well-known name. However, his advice on credit cards has been met with mixed reviews. He believes that no one should ever use them because they encourage people to spend more than what they can afford and lead to a cycle of debt. Yet many financial experts disagree with this philosophy and argue that credit cards can be beneficial when used responsibly.

Dave Ramsey’s main point is that credit card companies make money by charging high-interest rates and fees for those who fail to pay their balance in full each month. For this reason, he advises consumers not to use them since it will only hurt their finances in the long run.

He has advocated for the use of cash only for many years. He believes that people should live within their means, pay off their debt and invest in a variety of assets. This philosophy has been extremely helpful for his followers, and many people have been able to successfully follow his advice.

He will tell his listeners on his radio / YouTube channel that they shouldn't use credit cards for any reason even if they pay them off every month without fail and that you don't need a credit score.

Moving to a cash-only system means that you will lose your credit score in about 7 - 10 years. Without a credit score, you will need to continue to use cash only.

How credit scores work

Credit scores are an important part of managing your money and making sure you’re set up for success. But what exactly is a credit score, how does it work, and why is it so important?

A credit score is a numeric representation of your financial trustworthiness. It’s calculated by the three major credit reporting bureaus—Experian, Equifax, and TransUnion—using information from your credit reports. Your score can range anywhere from 300-850, with higher numbers being better. The key components they consider when calculating this number include payment history, length of credit history, types of accounts in use, the amount owed on accounts, and new inquiries or applications for new lines of credit.

Your credit score plays an important role in determining whether lenders approve you for loans or other forms of financing. So unless you can pay 100% cash for every big ticket purchase going to a cash-only system will lock you out of an affordable home.

Cash only impact on getting a mortgage

It’s no secret that Dave Ramsey is a well-known figure for his financial advice, but what about when it comes to the process of getting a mortgage? While cash only is one of the main principles preached by Dave Ramsey, it doesn’t necessarily make getting a mortgage any easier.

When attempting to get a mortgage, there are several factors considered by lenders in order to determine if you’re eligible. One factor in particular that can be problematic for those who follow the cash-only mantra is the credit score. Having and maintaining a good credit score is essential when trying to secure a mortgage loan and if you’ve gone completely cash only then your credit score won’t reflect positively on your application. Other factors such as income and debt ratio can also be impacted by residing solely on cash payments as banks will want proof of income from other sources as opposed to just liquid assets.

In addition, Dave Ramsey will tell you that you should get a 15-year mortgage and not a 30-year because the interest rate is lower on a 15-year mortgage. But without a credit score you will be denied a home and if you somehow aren’t your interest rate for either a 15 or 30-year mortgage will be over 10%.

Dave Ramsey also suggests that you don’t spend more than 25% of your take-home pay on a home. Also, you should pay 20% in cash down (no less than 5% for first-time home buyers and avoid FHA and VA loans).

Let’s break down the numbers

As of December 28th, 2022 the 15-year fixed mortgage rate could be as low as 6.08% if you have a perfect credit score. For the sake of argument, I will use that number even though most would be paying closer to 6.5% with good credit.

According to Lending Tree, if you have no credit score you will be unable to obtain a conventional mortgage (minimum credit score is 620), FHA (minimum credit score is 500), and USDA (minimum credit score is 640).

VA loan doesn’t have a minimum but Dave Ramsey says to avoid those so they are off the table as well now if following his advice. To get a mortgage with no credit score you will need a co-signer (for their credit score, but Dave Ramsey would tell you to never cosign on a loan), have a very large down payment, and go through a manual underwriting process. But for the numbers, let’s say you can obtain a mortgage from a credit union with no credit score at a perfect credit score rate.

If you live in the Denver area I can find 1,000 sq foot homes for sale anywhere from $400k to $700k. I can find 600 sq foot condos for $200k but they would have HOA fees as well. So let’s stick with a $400k home that will need some fixing up to live in it at a 6.08% mortgage rate for 15 years and a 20% down payment.

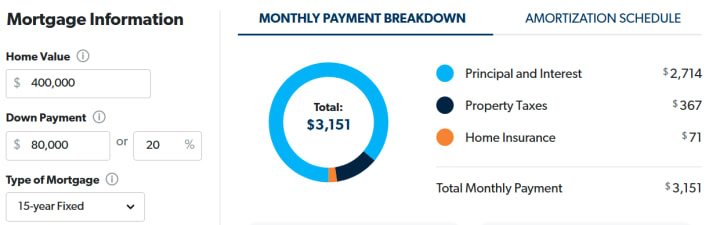

Dave Ramsey Mortgage Calculator - 400k home with an $80k down payment with a 15-year fixed mortgage at the best rate of 6.08% in Dec 2022 will be a $2,714 a month mortgage payment. This doesn't include taxes and insurance monthly.

You will need to save $80,000 in cash and will owe $2,714 a month for the mortgage for the next 15 years. Looking at Dave Ramsey’s no more than 25% take-home rate means you will need to make $10,856 a month after you pay taxes, health insurance, and any other deductions that come out of your paycheck. This means that you probably need to make about $180,000 or more a year to afford a $400k 1000 sq foot home in the Denver Metro area that will need about $5,000 to fix it up to make it livable.

Considering that the median wage in Denver in 2022 was $66,696 it is impossible for a person to buy a home using these numbers.

Wow, you read a lot to get here. Can you do me a favor, please? Can you leave a comment if this was helpful to you or if I missed something? Alternatively, it would help me out a lot if you shared this content with those that might need to see it. Thanks, you are the best!

Dave Ramsey on rent

From his website:

“Your rent payment, including renters insurance (more on that later), should be no more than 25% of your take-home pay.

That means if you’re bringing home $4,000 a month, your monthly rent should cost you $1,000 or less. And remember, that’s 25% of your take-home pay—meaning what you bring in after taxes.

We know, 25% might seem like a low number to you. After all, most people are spending a lot more than that on their housing costs—nearly 36% on average.”

Looking at this and the median wage in Denver is $66,696. Using Dave Ramsey’s math on his website we will take this annual pay multiplied by 80% to account for taxes and health insurance. This means that your take-home pay would be $4,446.40. So you can spend $1,111.60 on rent.

The average rent for an 841 sq foot apartment in the Denver Metro area is $1,994. In fact, only a little over 1% of all listings would meet these numbers. These numbers are for Rentcafe.com and they list most of the major cities in the state of Colorado, and the lowest average rent was $1,407 if you can live about 1.5 hours outside of the Denver metro area (one way) in Greeley.

Dave Ramsey's numbers just don't work

It may not sound like it but I am actually a big fan of the concepts that Dave Ramsey tells people in his baby steps. It would be great if people could make enough money to not spend more than 25% of their take-home pay on rent or a mortgage but this hasn't been true for years.

I totally agree with him that you shouldn't use credit cards unless you can pay them off every month because otherwise the bank issuing you your credit card is making about 30% off of your money mismanagement.

But with inflation, the cost of food is 10% higher. Because of the pandemic rents and interest rates have soared. You can't negotiate your rent at this point because everyone in my area increased their rates by 15% - 25%. And making more income isn't as easy as everyone says. My son applied for many jobs and most are taking 2 - 4 months to respond back to people for an interview.

So while I would love to say, YES FOLLOW DAVE RAMSEY! I just can't. The numbers don't work anymore.

What does work? Create an emergency fund and then try to live within your means. This means that you will need to look at doing two different things at the same time: 1) Cut back on spending and focus on saving money as I speak about in my article, how to save 3000 in 3 months, and 2) Look for ways to make more money.

If you want to make more money in your career check out my article about the 1 strategy to make more money.

Also, you can look at making more passive income and you can learn more about that here.

Join my free Facebook group to get a ton of free resources to help you get out of debt, learn how to invest your money, and work toward having the option of retiring early.

About Dwight Scull

I have been married to my wonderful wife, Rebecca, who puts up with me since 1999. I am a proud father to my Gen Z, son, and daughter-in-law. Grandfather to my favorite granddaughter who was born in 2021.

I lost my mom, father-in-law, and 12 others in 2013 and was DEEPLY in debt. I started reading and watching all the financial info I could find.

I chipped away at my debt and went from a negative $105k net worth having one home paid off, no credit card debt and saving/investing 45%+ of my gross salary.

I used these daily habits to lose 100 pounds and keep it off.

I believe that you can overcome any challenge you face if you just take small daily actions and be consistent with them. It is how you will be financially successful.

Join my free Facebook group to get a ton of free resources to help you get out of debt, learn how to invest your money, and work toward having the option of retiring early.

About the Creator

The Rollercoaster Ride of a Trader's Career

Unveiling the Drama and Humor Behind the Trading World Wanted: Adventurous souls with nerves of steel, a passion for numbers, and a flair for risk-taking. Does this sound like you? Welcome to the chaotic and exhilarating world of trading. Strap yourself in for a wild ride filled with highs and lows, thrills and spills, wins and losses. In this article, we'll delve into the heart-pounding journey of a trader's career, where drama and humor mingle in a dance of chaos and order. Hold on tight as we explore what it truly means to embark on a path where fortunes are made and lost in the blink of an eye.

By Max Gachet6 days ago in Trader

A New Beginning

Tony couldn’t sit still, crossing and uncrossing his legs, trying to calm his trembling hands as Clara stood at the office window deep in thought. The airline ticket in his shirt pocket moved to the beat of his heart¬– each beat bringing back the nightmare causing memories of the words he’d spoken over ten years ago. Thanks to Clara he’d finally gained the courage to buy that ticket.

By Gerald Holmes4 days ago in Fiction

Comments

There are no comments for this story

Be the first to respond and start the conversation.