An individual is much like a business, with assets & liabilities, except that businesses are able to focus on evaluating their current & long term monetary goals through a dedicated financial team, while at an individual level, such sincerity and focus on granularity for financial planning is often missing.

Everyone wants to have a proper financial plan, but only a small percentage of our Indian population has actually one ready.

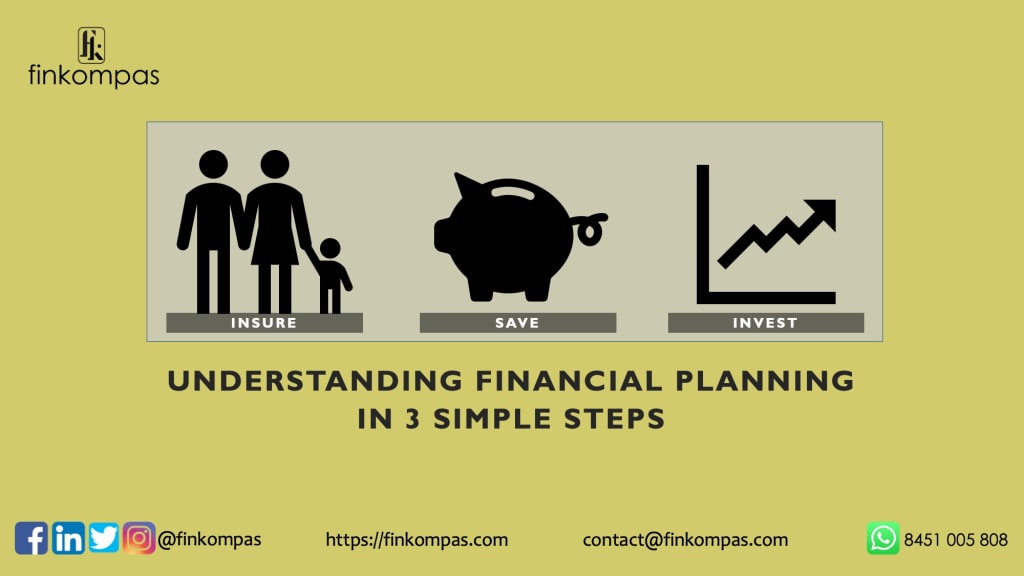

Through this article, we are covering the 3 simple steps which are the core of any financial plan i.e. Insure. Save. Invest. (in that order).

A. Insure

This is the first and most important part of a financial plan. Two key sub-parts of this element are:

i. Term Plan/ Term Insurance: It is the purest and most cost-effective form of life insurance, which provides financial protection in case of death of the life insured during the term of the policy. It is designed to financially protect one's family in case of the death of the main earning member.

Ideally, the sum assured or cover should be at least 15 to 20 times of annual salary. So, if one’s annual salary is Rs 10 lacs, one should try and take a minimum cover of Rs 1.5 crore. So, if something happens to the person, the family gets the sum insured. This amount when invested in a 3 or 5 years Fixed Deposit (assuming 6.6% annual returns), shall add interest of approx. 10 lacs per annum, thereby ensuring the insured person’s family is supported through tough times. If you are the main earning member of the family, the term plan is the first thing you should buy.

ii. Health Insurance/ Medical Insurance: Health Insurance is a type of insurance that in case of a medical emergency offers financial coverage for medical expenses. It provides insurance coverage to the insured with multiple benefits (dependant on the plan), including cashless hospitalization, day-care facility & coverage for terminal & critical illness etc.

Given costly medical expenses, it is advisable to have minimum Rs 1 lac cover per person, implying a family of 4 members should have a minimum family floater health /medical insurance for Rs 4 to 5 lacs. In metros like Mumbai where healthcare is costlier, you can go for top-up health insurance plans wherein you can go for a higher cover of up to Rs 10 - 25 lacs also (depending on the insurer and plan).

Critical illness is an add-on that you may take over & above the basic health insurance cover. It helps cover an assured sum up to Rs 1 Cr and is payable by an insurer in case of diagnosis of some specific medical issues/ailments (list of diseases vary from insurer to insurer).

B. Save

Once you have covered life and health insurance, chances of financial drain and resultant anxiety are minimized. Now, as the next step focus should be to save for an Emergency Fund. The amount here can vary from 6 to 12 months of your monthly expenses (including home loans/other EMIs). So, if your monthly expenses are Rs 1 lac, you should plan to keep an emergency fund of Rs 6 to 12 lacs. It is recommended this amount be kept in the form of Fixed Deposits (considered relatively safer wrt other financial instruments) with high rated banks.

C. Invest

This is the last part of your financial plan. Now, you are good to go. After covering for the above insurances and an emergency fund, you should strive to save at least 25% of your monthly salary. These savings can then be invested in highly rated, higher return financial products like Mutual funds in a lump sum or systematic investment plan (SIP).

The earlier one starts, the better. A small monthly SIP of Rs 1000 when invested over 35 years, can help build a wealth of Rs 1 cr (assuming 12% annual returns, annual 5% incremental SIP). #timepowerofcompounding

You can also go for investment in shares of high quality/blue-chip companies. ELSS funds are also a good investment option for these equity funds invest in stocks as well as provide tax benefits under Income tax sec 80C. The idea is to generate a consistent return over long periods. If you understand how the stock markets work, companies fundamentals, you can start learning and investing. Though, wherever possible it is advisable to go for a professional financial planner.

A proper financial plan can ensure a fulfilling life, with adequate life and health insurance protection as well as wealth creation opportunities for a comfortable retirement.

Stay Healthy, Wealthy & (and the most important) Stay Happy!

We are Finkompas, is a leading financial technology company that aims to simplify your financial life by providing great financial products - loans and investments

Follow us on Facebook, Linkedin, Twitter, Instagram

Home Loan, Personal Loan, Mutual Funds, Equity Funds - Large Cap, Mid Cap, Focused, ELSS.

About the Creator

THE GRAPHICS CARD WILL MEET ALL YOUR DEMANDS ON YOUR PC

In the dynamic realm of computing, few components command as much attention and admiration as the graphics card. These technological powerhouses, often referred to simply as GPUs (Graphics Processing Units), serve as the beating heart of visual processing in modern computers, enabling everything from immersive gaming experiences to complex visual simulations and professional content creation. Among the latest contenders in this arena stands the ASUS Dual GeForce RTX 4070 Super OC Edition Graphics Card, a formidable specimen boasting cutting-edge features and unrivaled performance.

By Kim Long Nguyệt Ngữ4 days ago in Trader

Clinging to Childhood

The playground is empty, as it should be past sundown. There is a warm breeze, and I can see everything despite the late hour. What time is it, anyway? It could very well be past midnight. I can never keep track of time, especially in the summer. A prickly piece of popcorn hides like a stowaway in the left cup of my padded training bra. I stuffed the tissue in last minute— a decision I’m beginning to regret, based on the events that are unfolding rapidly before me. To my left, laying non-chalantly on his back, is my date for the evening. He is two years older, could probably grow facial hair if he wanted to, and drives a secondhand Honda. He may as well be a Man. I, on the other hand, feel like a fraud with my too-short short-shorts, sparkly lip gloss, and makeshift push-up bra. I keep my arms pinned to my sides as I feel the dreaded circles of sweat beginning to manifest on my brand new Abercrombie top. I cup my elbows with my hands and stare down at my hint of cleavage, praying that the tissue doesn’t pop out like a white flag surrendouring my lack of womanhood.

By Marti Maley6 days ago in Fiction

Comments

There are no comments for this story

Be the first to respond and start the conversation.