The Step-by-Step Guide to Passive Wealth For Dummies

It only has 3 steps, not 100.

Are you confused by all the advice and financial jargon out there?

Does it feel like investing is some sort of a dark art reserved for the experts and talking heads on Bloomberg TV?

I’m here to tell you it isn’t.

Investing and growing a successful portfolio is 100% possible for anyone willing to learn the basics.

Don’t let the jargon and scaremongering headlines steer you away from building a brighter financial future for yourself. Without spending countless hours on it.

I had a friend recently ask me about the simplest, most efficient way to start investing for long-term wealth.

The below principles have personally enabled me to grow my portfolio from £0 to over £100k in my twenties, spending about 10 minutes a month on it. And you can, too.

Read on for a straightforward, 3-step process to get you started in no time. But first, we’ll define a few terms you need to be aware of.

The key terms you need to know before getting started

Below are essential terms you’ll come across on your investment journey.

You don’t need to know all the details. Understanding the basics will be enough to get you started.

Asset classes: the types of assets you can invest your money in. There are 5 of them (shares, bonds, commodities such as oil and gold, real estate, and cash).

Portfolio allocation: your portfolio, the sum of your investment value, will be spread across the above asset classes. This spread defines its allocation, also called portfolio composition. Simply put, it’s what your portfolio is made of. For example: 70% stocks, 20% bonds, 10% cash.

Funds: a collection of holdings (business entities such as companies) listed under one umbrella managed by a fund manager. For instance, a single fund may have 50 companies in it. This means the fund’s management team pick and manage the shares from those 50 companies for you. All you have to do is choose that fund and invest your money in it to be invested in all those 50 companies.

Stock picking: this is the opposite of the above approach. Here’s, you’d be researching, analyzing, and picking individual company stocks. This is time-consuming and requires specific expertise and understanding of each company’s financial statements, performance metrics, etc.

Index funds (or trackers): these are types of funds that simply aim to track and replicate the performance of an index, such as the S&P 500. This could also be a benchmark, such as an index that tracks a specific industry. The fund is not trying to “beat the market” (generating higher returns than the given index); rather, it tracks it. As such, index funds, also called trackers, do not require any active management choices. This typically results in much lower costs compared to more active funds.

Passive funds: passive funds, such as trackers, are not actively managed by their fund managers. The fund’s management team oversees the fund’s performance but does not actively pick and choose stocks or the fund’s composition.

Active funds: conversely, these funds are managed more actively. Here, the fund’s manager does pick and choose stocks and influences the make-up of the overall fund. This typically results in higher fees to you as an investor — sometimes, those fees are not justified as such funds are not guaranteed to beat the market.

Diversification: spreading your bets, or not putting all your eggs in one basket. The principle behind this is risk mitigation. If you invest in stocks, bonds, as well as, say, real estate (asset diversification), in companies operating across the global (geographic diversification), and operating across various sectors (sectoral diversification), you’re spreading your risks. If one sector, company, or geography performs poorly, others are likely to compensate for it. If, on the other hand, you invest 100% of your money in one fund focussed on one industry, you’re taking on more risk.

Total Expense Ratio: when you invest in funds, you’ll incur several charges. It’s important to know what those are, as they’ll eat into your returns over time. They include ongoing service charges, management fees, and in some cases, transaction costs (for buying and selling shares).

Fund supermarkets: these are simply platforms that allow you to invest in a range of funds — across sectors, geographies, and asset classes.

You now have all the basics you need to be able to invest in the market successfully.

Let’s dive into 3 simple steps you can take to build your own portfolio, starting today.

1. Open up an investment account

The first thing you’ll need is to do some research on the providers that you can open an investment account with.

One important distinction to make here: I’m not talking about the kind of investment accounts that are used for speculative trading. Rather, the equivalents of IRA and 401(k) in the US or ISAs (Individual Saving Account) and SIPPs (Self-Invested Pension Plan) in the UK.

Look for providers that offer a range of funds through their fund supermarket.

I don’t recommend using banks, though many like HSBC provide such accounts. The reason? Banks tend to have a narrower offer, promoting their own funds and restricting your ability to invest more broadly.

I personally use Fidelity UK because of its intuitive, easy-to-use platform and transparent pricing.

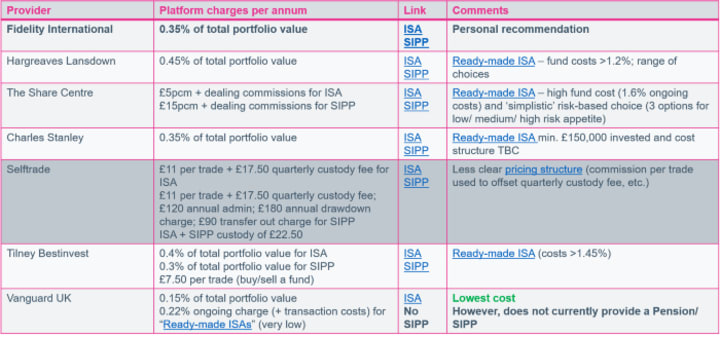

Below is a table showing some of the key providers I’ve compiled for you, especially if you’re based in the UK. If you’re in the US, you can check out the main providers available to you here.

A few things to consider when selecting your investment fund provider are:

a) What are their annual fees?

b) How do their fees vary as your portfolio grows (the fees may come down beyond a certain threshold, making investing more attractive over the long-term)?

c) Do they have any extra charges, such as transaction fees for each time you buy and sell a stock or fund?

Once you’ve chosen a provider, the next step is to do a bit of research and pick some funds to put your money in.

2. Make a fund selection

The range of funds available may seem confusing at first. But once you understand what to look out for, you’ll be able to confidently settle on a small number of funds and start growing your portfolio.

One advantage to fund investing over individual stock picking is that you can invest in, say, 50 companies with one click. By investing in just a few of these funds, you’ll be a well-diversified investor.

To make an informed selection, don’t just pick out any funds. Even the “recommended funds,” the “top 40,” or similar offers from your providers because they sound appealing or are on discount.

Essentially, you need to understand 3factors when choosing your funds.

How the funds perform, what their risk levels are and whether those align with your goals, and the costs involved.

2.1 Understanding fund performance

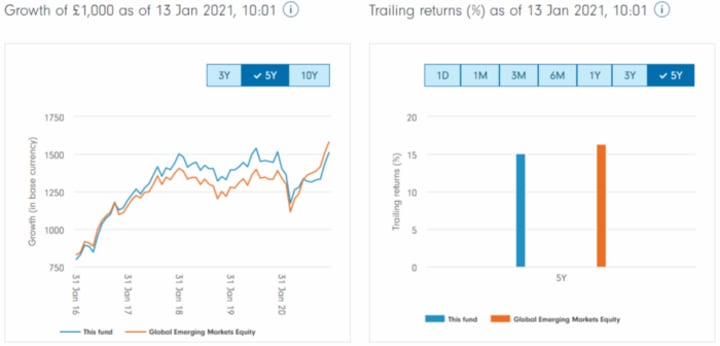

Whenever searching for a fund in your provider’s offering, you’ll come across charts that look like the below.

Don’t let these charts and numbers put you off.

Let’s break it down. What does the above tell us?

a) On the left: this shows the fluctuations in the fund’s returns (in blue) versus its benchmark (an index chosen as a relevant comparison to evaluate the fund’s performance against). The chart visualizes what £1,000 invested on a given date would amount to across a 3, 5, or 10-year timeframe. In other words, it gives you an idea of the growth potential of the fund over the time period.

b) On the right: “trailing returns” represent the total returns generated by the fund over a given time period. Sometimes “year to date” is used, when tracking returns from the start of the year. Again, this compares the selected fund with its benchmark and lets you compare the results over various timeframes.

Looking at a fund’s returns over longer periods of time, such as 5 or 10 years, helps to assess the potential durability of the fund.

Don’t forget that past performance is never a full guarantee that the fund will perform in the same way going forward.

The market conditions may change, and the star fund manager who took a fund to new heights will move on. A number of factors can influence any given fund’s performance.

However, such timeframes give you a good indication of what kind of fluctuation you’re exposing yourself to by investing your money in the fund.

The other side of the coin you need to know about is the fund’s risk level.

2.1 Understanding risk ratings

What’s important here is to ensure you consider the risks involved, based on your immediate need for cash and lifestyle.

If you need to pay for your wedding or college degree 3 months from now, you might what to stay away from riskier funds.

If you’re looking to build your retirement pot over the next 50 years, taking on more risk is much more acceptable. Investing over so many years is more likely to “smooth out” returns over time and protect your total earnings, in spite of global downturns and temporary market crashes.

To work out your “risk appetite,” you can use this risk calculator.

Risk, in this context, means the degree of volatility of a given fund. The more volatile, the more its returns are likely to fluctuate. This means the value of your investments could go up and down when you don’t expect it.

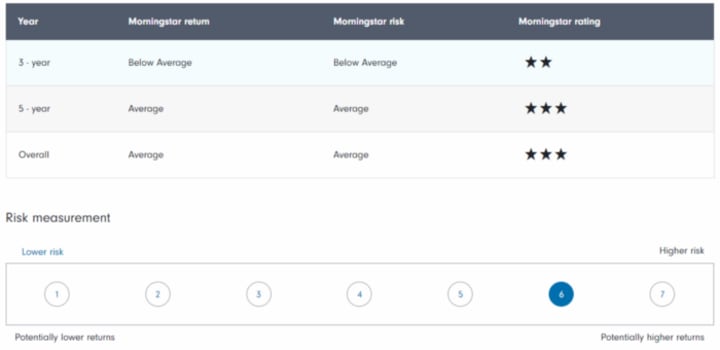

Let’s look at the same fund and its risk rating, shown below.

What does this data tell us? You can see a star-rating representing the overall performance of the fund. Underneath, the risk level is displayed on a simple 1 to 7 scale.

The equation here is: the higher the risk, the higher the potential returns — but also the potential losses.

Again, knowing your own circumstances and cash needs should help you pick a risk level you’re comfortable with.

A number of data points underpin this rating. These include deviation from the fund’s benchmark (“tracking error”), the degree of volatility in its returns (“standard deviation”), and others.

Aside from performance and risk, you need to know about how much it’ll cost you to invest in a fund.

2.3 Understanding fund costs

Broadly speaking, the fees of the funds you’ll invest in are broken down into:

a) Ongoing service charges: fees charged by the manager to cover the ongoing costs of running the fund. These tend to be fairly static from year to year, unless the fund takes a more active management style and increases its fees as a result.

b) Transaction fees: fees associated with the daily trading activity within the funds (buying and selling company shares). These tend to vary, based on the prices of the assets being bought and sold by the fund manager.

Both the above add up to the total expense ratio, a measure of the total cost of any given fund to the investor.

That’s what matters to you — the investor.

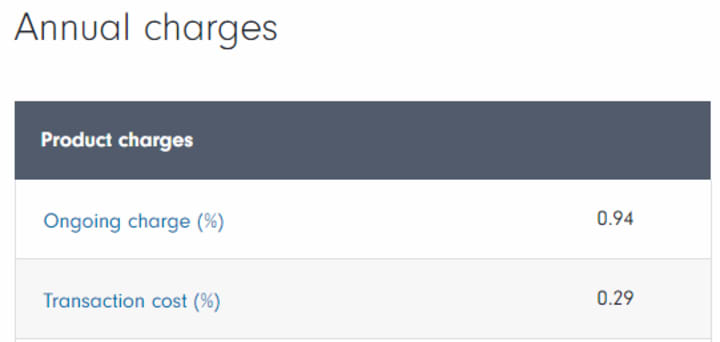

In our example, here’s the cost breakdown of the fund.

In this case, this means you’ll be paying a 1.23% total cost for investing in this fund. So, if you were to invest £1,000 in it, you’d be paying £12.3 in fees.

What you need to understand is that those costs compound over time: the £12.3 above is £12.3 you can’t invest back into growing your portfolio. This may not seem like much, but over decades of investing, it could have a huge impact on your wealth.

As John Bogle, the forefather of index funds and founder of Vanguard put it:

“Compounded over that time frame [60 years], the high costs of investing can confiscate an astounding 70% of your lifetime returns!” — John Bogle

By now, you’ve opened up your investment account. You’ve picked 2 to 5 funds to invest your money in. You’ve done so in light of their performance, their risk levels and their associated costs.

The last step is to set up regular payments into your portfolio.

3. Invest every month on auto-pilot or manually

Depending on your own circumstances, you may want to do this less frequently than every month.

Personally, I do this every month because investing regularly will smooth out returns over time, even though I may hit bad periods with lower returns. It’s also easy to set up a monthly lump sum to invest.

I know how much I can afford to save on a monthly basis by deducting my income from my expenses and keeping a reasonable amount of cash aside in case something unexpected happens.

I then pay that amount of money into my investment portfolio around the same time each month.

There are 2 ways you can invest in your portfolio regularly:

a) Invest on auto-pilot: set up a regular “contribution plan,” choosing the amount of money you wish to put into your portfolio, when, and in which funds.

b) Invest manually: pay into your portfolio and manually allocate how you wish to split that money between your funds.

The first option is the most hands-off way to go.

Just decide how much you can put away each month when you want that money to go out of your bank account into your portfolio, and select which funds you want that money to go into.

Job done.

I personally prefer the second option, only because I like to look at the previous month’s performance and allocate my savings between funds based on that information.

I have no data or evidence to suggest one way may be better than the other.

It’s entirely up to you to decide how closely you want to be involved and how much time you want to dedicate to managing your portfolio.

In any case, to be clear, once you’ve gone through the above 2 steps, this final one will take barely any time at all. I spend about 10 minutes a month on my portfolio, and that would literally come down to 0 had I chosen the “auto-pilot” option.

Once a year or twice at most, you can then adjust your portfolio to make sure it still aligns with your own goals. This is called “rebalancing.” Typically this means returning to the same allocation as you had at the start of the year.

So, if you started the year with 70% invested in stocks and 30% in bonds, this will evolve during the year based on how each fund is managed. It may end up being 80% stocks and 20% bonds at a later point. You may want to recalibrate and go back to the initial ratio if that still matches your goals.

As you go through life, you’ll also want to rebalance your portfolio accordingly.

When nearing retirement or planning for large expenses (such as paying for your kids’ education, buying a home, etc.), you might want to scale back on the risker stocks and put more money into the more stable bonds. And vice-versa.

Beyond this yearly rebalancing, you don’t need to tinker with your portfolio.

Investment legend Ray Dalio himself only does this once a year.

And here’s what Warren Buffet has to say about how long you should be invested in a given stock or fund:

“Our favorite stock holding period is forever.” — Warren Buffett

Changing your portfolio too frequently may damage your returns, as you’ll be incurring fees to switch in and out of funds. Such fees will compound over time and eat up a chunk of your returns over the years.

This could make a big difference when added up over a lifetime of investment!

Investors who hope to “beat the market” and try to time when to enter or exit an investment are likely to fail, anyway.

They get distracted by checking funds’ performance all the time and seek to gain insights they think others, including the pros, don’t have.

I don’t know about you, but incurring higher fees for no additional returns whilst spending hours researching stocks and funds sounds like a bet that’s not worth talking to me.

To be honest, I don’t want to be spending hours on anything here.

I want my portfolio to grow quietly and consistently in the background, watching my income increase over time. I’m not looking for any quick gains. And I’m in it for the long haul.

Wrapping up

To summarize, all you really need to start and build a successful investment portfolio boils down to:

a) Open up an investment account that allows you to choose funds from a broad range of options (“fund supermarket”).

b) Select a few funds that meet your risk appetite and financial goals, based on their performance and risk ratings.

c) Invest in your chosen funds regularly, such as every month, and only review your overall portfolio once a year or twice at most.

I hope the above helps you get started on your investment journey.

It’s not all that complicated, and it’s definitely available to anyone who has an Internet connection.

It doesn’t take that much time, either. It literally takes me 10 minutes each month to invest my money. My portfolio’s like a well-oiled machine.

Yes, there is a degree of risk involved. Anything worth doing contains an element of risk. But watching from the sidelines won’t help you build the future you want for yourself.

As Zuckerburg stated:

“The biggest risk is not taking any risk” — Mark Zuckerburg

So what are you waiting for?

This article is for informational purposes only. It should not be considered Financial or Legal Advice. Not all information will be accurate. Consult a financial professional before making any major financial decisions.

About the Creator

Clément Bourcart

Business Consultant, Project Manager, Investor. Medium top writer in 💰Investing, 💵Finance and 🦄Entrepreneurship.

Keep reading

More stories from Clément Bourcart and writers in Trader and other communities.

I Earned £100k in Passive Income in My 20s Following Warren Buffett’s Advice

“If you aren’t willing to own a stock for ten years, don’t even think about owning it for ten minutes.” — Warren Buffett Financial education is a huge, gaping hole in our traditional education systems. Most young graduates leave formal education with no idea about how to manage their finances.

By Clément Bourcart3 years ago in Education

The Rollercoaster Ride of a Trader's Career

Unveiling the Drama and Humor Behind the Trading World Wanted: Adventurous souls with nerves of steel, a passion for numbers, and a flair for risk-taking. Does this sound like you? Welcome to the chaotic and exhilarating world of trading. Strap yourself in for a wild ride filled with highs and lows, thrills and spills, wins and losses. In this article, we'll delve into the heart-pounding journey of a trader's career, where drama and humor mingle in a dance of chaos and order. Hold on tight as we explore what it truly means to embark on a path where fortunes are made and lost in the blink of an eye.

By Max Gachet6 days ago in Trader

Faedaze

Daisy leaned back against the wall of the window bench, the dress she was embroidering on falling to her lap, all but forgotten. Her gaze rested on the trees just beyond the edge of her garden, watching with dreamlike expression on her face, waiting for something others doubted would ever come.

By Kelsey Clarey4 days ago in Fiction

Comments

There are no comments for this story

Be the first to respond and start the conversation.