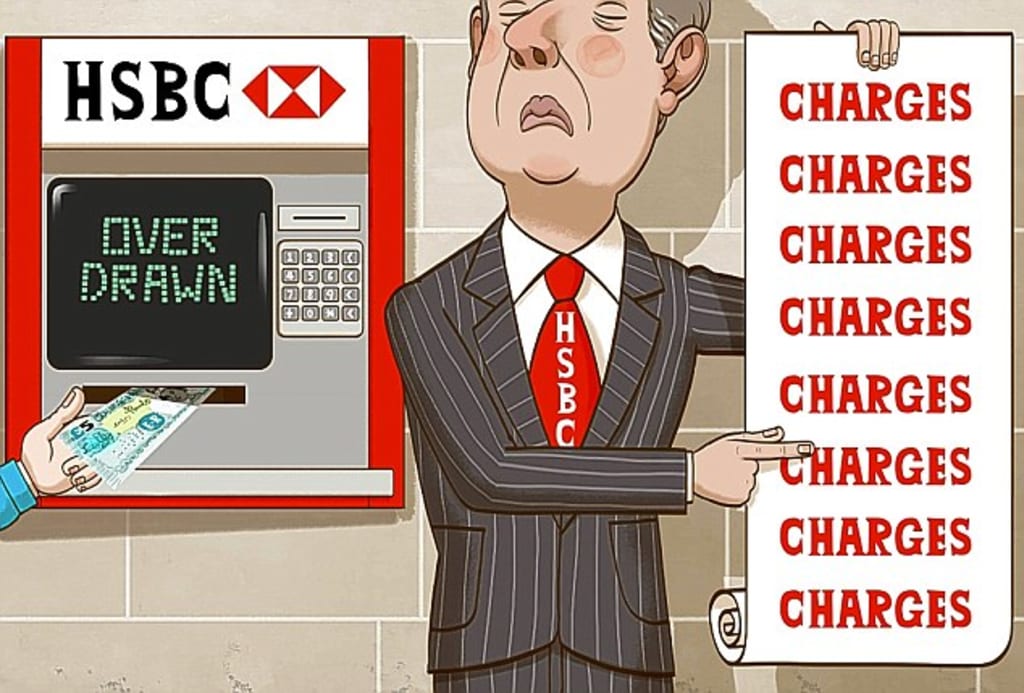

So, what actually is an overdraft?

For many, students particularly, overdrafts are an everyday reality. They exist where you draw amounts from your bank account greater than the account holds. Usually, you can tell you are in your overdraft because your bank balance will show as a negative number. For instance, -£500 indicates you are £500 overdrawn from your bank.

But you knew that anyway, right?

It is very easy to be complacent about having an overdrawn bank account balance, because after all, ‘everyone has an overdraft’. Don’t forget though—you are spending someone else’s money when you are in an overdraft.

Overdrafts are one of the many forms of loans that banks provide to the public. In other words, an overdraft is a debt. And the rules of debt are generally as follows:

1) You borrow money...You, the borrower, gain access to a sum of money from a lender, such as a bank

2)...for a (few) month(s)/year(s)...You have access to this money for a defined period of time, as per the contract you enter into. Once this period has ended, you are required to pay back the loan in full (or instead in regular instalment payments in some cases such as with a mortgage)

3)...for which you may pay interest...For being able to use the lender's money over the defined period of time, you may be subject to interest charges for use of the money during the lending period. Interest is usually payable together with the amount you owe.

4)...or even late penalty fees...You may even be subject to penalty fees should you fail to make a repayment on time and in full, or fail to meet another essential condition of the contract.

Imagine now instead of an overdraft which you can utilise via your contactless debit card, now you had £0.00 in your bank account and a contactless credit card. Now ask yourself honestly…

Would you use your credit card the same way as you use your overdraft?

Of course not! Because you know that in a month’s time, you are going to have to repay at least some of that credit card debt and the interest is going to slowly accumulate if you don’t pay off the full balance in a timely manner.

And if you have no money of your own, there is no way you will be able to finance the purchases you have made on your credit card.

There are therefore only two situations you would use your credit card:

A) You know you are going to earn in a month more than/the same as what you are planning on spending

B) You have to make some unavoidable purchases in an emergency situation.

So why treat your overdraft in any different way?

The students out there with interest-free overdrafts are now going to tell me “But I don’t have to repay my overdraft for a very long time. As long as I don’t exceed my interest-free overdraft limit everything is fine”.

And this is what makes an overdraft more dangerous than other forms of debt…

Because in reality, there is nothing stopping your bank from asking you to repay the full amount tomorrow. The guarantee of being able to borrow long-term is not actually there. So unlike a credit card where you will know what day of the month you will receive your next statement and how long you have to pay that balance, there is no such certainty with your bank account. It is unlikely this will happen as banks typically do not remove an overdraft prematurely, but banks can and will remove your overdraft if they feel it is in their best interest to do so.

Perhaps worse still is if you exceed your interest-free overdraft allowance, you will have to pay a fortune in overdraft fees. In many cases, entering an unarranged overdraft is more expensive than taking out a payday loan. At least with a credit card, your card will (for most people) be declined when you try to make a purchase, meaning it’s not even possible to spend more than your credit limit and so you cannot run the risk of incurring such hefty fees whilst also damaging your credit score.

Long-term, overdraft dependency can inhibit your ability to be more financially responsible with your money and create a never-ending reliance on overdrafts as banks are not giving you the chance to escape your debt by offering you such a large overdraft in the first place. Two million Britons today find themselves in a ‘permanent overdraft’ situation.

And students take note here. When you enter the working world as a fully fledged adult, you will not automatically benefit from an interest-free overdraft. You will likely be given one year to clear your overdraft from the time your account moves from a student account to standard current account, vastly increasing the likelihood you will enter an unarranged overdraft and have to pay the related fees.

So how do you get out of my overdraft for good?

The key to avoiding a vicious debt cycle and improving the health of your bank account is as simple as ensuring that your income exceeds your expenses such that your savings can be used to pay down the utilised portion of your overdraft.

For students who you have graduated, give yourself 8-10 months to completely pay off your overdraft. For those of you who rent, it is particularly important that you watch what you spend and ensure that at the start of every month, the balance in your bank account is higher than it was the same time in the previous month.

But the saving does not stop after you have paid off your overdraft

You need to continue saving well past the point of being debt free. If you suddenly incur unexpected and unavoidable expenses, you are likely to dip back into an overdraft facility you may no longer have as your bank by this point may have fully transferred you to a standard adult current account with no overdraft facility.

As a general rule of thumb, if in your bank account you are able to pay for next month’s rent (including bills) just after paying this month’s rent, you likely will have just about escaped the debt cycle.

If, for instance, you find yourself suddenly unable to work for a week or two due to unforeseen circumstances, you need to ensure at the very minimum you can pay for your rent and bills the following month (just because you find yourself in hospital or a loved one has died doesn’t mean your landlord will waive your rent that month! And sick pay may not be enough).

A failure to pay such ‘priority debts’ can have a detrimental affect on your credit score for as long as six years and may make you ineligible for an overdraft when you actually need one. You can say with some confidence that when you can pay for the next three month’s rent & bills and your next council tax bill, you are truly on your way to living a better, debt-free, financial future.

For more information on overdrafts, tips for avoiding fees, controlling your overdraft and or if you believe your bank has unfairly charged you overdraft, visit the Money Advice Service via the following link:

https://www.moneyadviceservice.org.uk/en/articles/overdrafts-explained

About the Creator

Keep reading

More stories from writers in Trader and other communities.

"Stride in Style: Discover the ALDO Men's Albeck Oxford"

In the realm of men's footwear, finding the perfect balance between style, comfort, and versatility can often feel like an elusive quest. Yet, amidst the sea of options, there emerges a beacon of excellence that embodies these qualities seamless: the ALDO Men's Albeck Oxford. As a distinguished member of ALDO's esteemed lineup, the Albeck Oxford stands as a testament to the brand's commitment to crafting footwear that not only exudes sophistication but also delivers unparalleled comfort and durability.

By Kim Long Nguyệt Ngữ3 days ago in Trader

2023 Fashion Designer Shoes Men Casual Platform Sneakes Lace Up Trainers Student Sneakes Mens Vulcanized Shoes Zapatillas Hombre

In the ever-evolving world of fashion, footwear has become more than just a functional accessory; it's a statement of style, personality, and individuality. One of the most intriguing trends to emerge in recent years is the fusion of casual comfort with elevated design, epitomized by the rise of platform sneakers for men. These shoes seamlessly blend streetwear flair with high-fashion sensibilities, creating a versatile option that can effortlessly transition from day to night, casual to formal.

By Wedson Vegasabout 14 hours ago in Trader

Comments

There are no comments for this story

Be the first to respond and start the conversation.