TDS Section 194Q-TDS on Purchase of Goods w.e.f 01.07.2021

Section 194Q

TDS Section on Purchase of Goods-TDS U/S 194Q

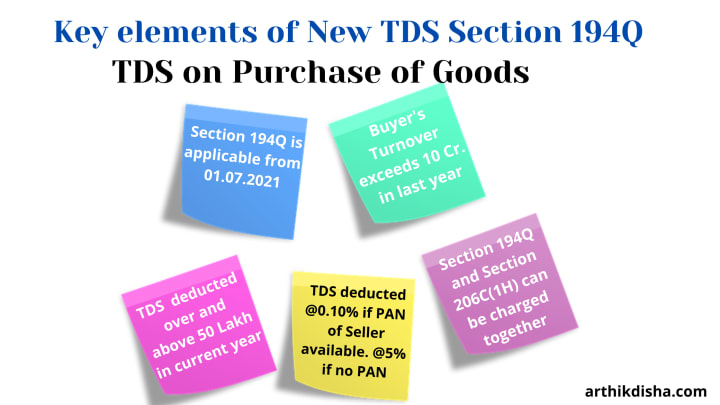

TDS Section 194Q: In the Finance Budget 2021, the Finance Minister has announced to introduce a new TDS section 194Q i.e. TDS on purchase of Goods which is applicable from 1st July 2021.

The idea behind the introduction of this TDS Section 194Q was to increase in the collection of advance income tax similar to Section 206C(1H).

TDS on Purchase of Goods-TDS deduction Section 194Q

________________________________________

The provisions of Section 194Q on Deduction of Tax at source on payment of a certain sum for the purchase of goods states that--

Any person, being a buyer who is responsible for paying any sum to any resident (hereafter in this section referred to as the seller) for purchase of any goods of the value or aggregate of such value exceeding ₹50 Lakhs(Fifty lakh rupees) in any financial year,

shall, at the time of credit of such sum to the account of the seller or at the time of payment thereof by any mode, whichever is earlier, deduct an amount equal to 0.1% of such sum exceeding ₹50 Lakhs as income-tax.

Explanation of the provisions of TDS Section 194Q

________________________________________

The provisions of Section 194Q are given in simple terms as follows:

1. Buyer means: For the purpose of this Section 194Q, 'Buyer' means a person whose total sales, gross receipts or turnover from the business carried on by him exceed ₹10 Crore during the financial year immediately preceding the financial year in which the purchase of goods is carried out;

2. TDS over and above ₹50 Lakh: TDS will be deducted on any sum paid over and above ₹50 Lakh in a financial year. This means TDS is not applicable on the whole amount rather on any sum exceeding ₹50 Lakh only in a financial year;

3. Rate of TDS: TDS @0.10% will have to be deducted on any sum exceeding ₹50 Lakh only;

4. If PAN not submitted: If the seller does not provide his PAN, in that case, the buyer has to deduct TDS @5% as per the newly amended section 206AA of the Income Tax Act;

5. When TDS to be deducted: TDS is to be deducted based on whichever is earlier as per the following:

1. 1. Date of payment and;

2. 2. Credit of the sum to the account of the seller.

When the provisions of TDS Section 194Q does not apply?

________________________________________

Exception: The provision of TDS U/S 194Q does not apply to the following conditions:

1. Tax is deductible under any of the provisions of this Act; and

2. 2. tax is collectable under the provisions of section 206C other than a transaction to which Section 206C(1H) applies.

This should be kept in mind that the provisions of Section 206C(1H) and Section 194Q may be applied jointly if the threshold limit of ₹50 Lakh is fulfilled in a financial year.

What is the difference between Section 194Q and Section 206C(1H)?

________________________________________

The major differences between the two sections are as follows:

Section 194Q-TDS on Purchase of Goods and Section 206C(1H)-TCS on Sale of Goods;

This section is for Tax Deducted at Source(TDS) and This section is for Tax Collected at Source(TCS);

This section is applicable to the purchase of goods and This section is applicable to the sale of goods;

Tax is to be deducted by the Buyer and Tax is to be collected by the Seller;

Deduction of Tax and deposition of tax is the responsibility of the Buyer and Collection of Tax and deposition of tax is the responsibility of the Seller;

Threshold limit of ₹10 Crore is applicable to the Buyer and Threshold limit of ₹10 Crore is applicable to the Seller;

Buyer has to check whether the threshold limit of purchase of ₹50 Lakh has been met and The Seller has to check whether the threshold limit of sale of ₹50 Lakh has been met.

This section is applicable from 01.07.2021 and This section was applicable from 01.10.2020;

TDS U/S 194Q is to be deducted even though on the same transaction Section 206C(1H) is applicable and As per Section 206C(1H) if on any transaction TDS is deducted by a Buyer, Section 206C(1H) will not be applicable on that;

The purpose of the Government mainly was to increase the collection of advanced income tax. This necessitated the Government to introduce the provision of Section 206C(1H);

But later it was seen by the Government that in most of the cases the buyer fulfilled the threshold limit of 50 Lakhs but the seller did not fulfil the threshold limit of 10 Crore.

So the objective of collecting more advanced tax wasn't getting to its full potential. Therefore, probably in the budget 2021, the Finance minister by introducing TDS on Purchase of Goods tried to recalibrate their advance tax collection system.

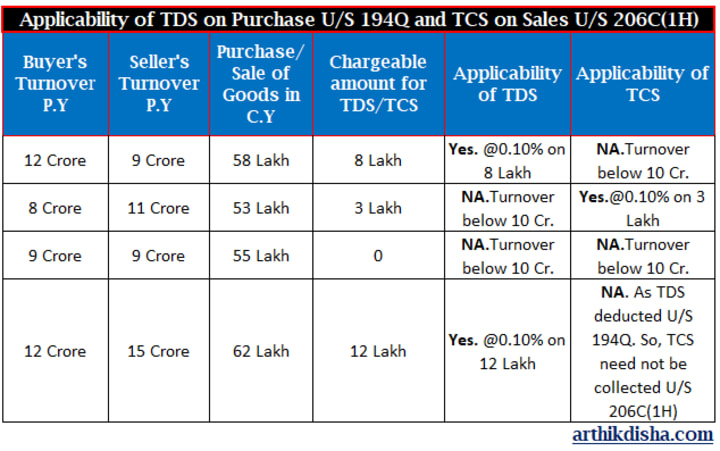

Applicability of TDS Section 194Q with examples

________________________________________

Let us take an easy example to understand the applicability of TDS on Purchase of Goods under TDS Section 194Q.

Before going for the example, one should keep in mind the following two important aspects regarding TDS on purchase of Goods and TCS on Sale of Goods:

1. Tax can be deducted and collected by both the Buyer and Seller U/S 194Q and U/S 206C(1H) respectively on the same transaction. This means these two sections may be applied togetherly;

2. As per Section 206C(1H), if on any transaction TDS is deducted by a Buyer under any other Act, TCS U/S 206C(1H) will not be applicable on that same transaction.

Illustration for easy understanding applicability of Section 194Q and Section 206C(1H):

About the Creator

Arthik Disha

A Personal Finance Blogger. Passionate about finance.

Keep reading

More stories from Arthik Disha and writers in Trader and other communities.

Income Tax Calculator FY 2021-22(AY 2022-23)Excel Download

Income Tax Calculator FY 2021-22 Excel Download(AY 2022-23) Every year the taxpayers especially the salaried persons keep on waiting for the Finance Budget hoping that there will be some tax reliefs, additional tax deductions or an increase in income tax slabs so that their total tax outlay gets reduced.

By Arthik Disha3 years ago in Trader

The Future of Algorithmic Trading and AI in Finance

In recent years, the financial industry has witnessed a rapid transformation driven by advancements in technology, particularly in the fields of algorithmic trading and artificial intelligence (AI). These technologies have revolutionized the way financial markets operate, providing new opportunities and challenges for traders, investors, and financial institutions alike. In this article, we will explore the future of algorithmic trading and AI in finance, examining the key trends, challenges, and opportunities that lie ahead.

By BLESSING COOL 3 days ago in Trader

Comments

There are no comments for this story

Be the first to respond and start the conversation.