Section 68 Of Income Tax Act-Unexplained Black Money?

Unexplained Cash Credit

Section 68 of Income Tax Act-Unexplained Cash Credit

Section 68 of Income Tax Act 1961, states that if any sum is found credited in the books of accounts of an assessee maintained for any previous year, and the assessee could not provide any explanation about the source and nature thereof,

or the explanation offered by him is not, in the opinion of the Assessing Officer, satisfactory, the sum so credited may be charged to income-tax as the income of the assessee of that previous year.

Therefore, Section 68 of the Income Tax Act clearly demands explanations regarding the source and nature of any cash credited to the books of the assessee, if the Assessing Officer is of the opinion that certain cash credit as found in the books might have gone through tax avoidance.

Further, if the explanations so offered by the Taxpayer is not satisfactory as per the opinion of the Assessing Officer, he is so authorised to charge that unexplained income to tax as the income of the assessee of that previous year for increasing the revenue of the Government.

What is ‘Unexplained Income’ as per Section 68 of Income Tax Act?

Section 68 classically deals with unexplained cash credit in the nature of loans, advances, deposits, share capital and etc.

Unexplained income or unexplained cash credit simply means any income or credit for which the Assessee does not have any valid explanations about the source and nature of such income and it was not reported for income tax purposes.

Or any explanation is given by the Assessee, but the Assessing Officer is not so satisfied with it, in that case, the income will be considered as the unexplained income and subjected to income tax for the year in which it was received.

Therefore, it is seen that the powers so conferred upon as per the provisions of Section 68 of Income Tax Act, the Assessing Officer(A.O) if not so satisfied with the explanations so offered by the taxpayer, may charge that unexplained income to income tax for that previous year in which it was received.

Therefore, to sum it up, we can say that any sum credited in the books of the taxpayer, it also may include gold, other valuable items, for which he offers no sufficient explanation or the I.T authorities are not satisfied with the explanation, such cash credit is called Unexplained Cash Credit/ Unexplained Income as per Section 68 of the Income Tax Act.

What is the purpose of Section 68 of Income Tax Act 1961?

The main purpose of introducing this Act was to arrest the loopholes of tax evasion matters. Generally, dishonest people are more prone to evade tax and try to find out the backdrops and the means through which they can escape their income from subjected to income tax.

Yes, the primary objective is to arrest the menace of Black money. Also, there are various black money restricting provisions such as Income Disclosure Scheme(IDS) effective after Demonetisation so that in conjugation with Section 68, Govt. can restrict such tax evasion cases and restrict the menace of black money.

If you have received any sum it must be disclosed before the income tax authorities. It might be an exempted income. But the Govt. wants you to disclose the sum of money received by you and there are sufficient explanations in terms of its source and nature of such cash credit.

Necessity of Section 68 of Income Tax Act 1961?

Before coming into the applicability of Section 68, we must know why people tend to receive undisclosed income in an unsolicited manner.

You might have seen that during the period of demonetisation, people used to receive unsolicited cash deposits from various third parties into their accounts.

It might so happen that after receiving such cash credits, your total income after receiving such unsolicited cash, did not exceed the basic exemption limit. So you are not supposed to pay any tax on your income.

But the third party who deposited the cash to your account might have escaped tax on that amount had he deposited the cash credit in his account instead of yours.

So, to mitigate such kind of unexplained income or credits, the A.O needs explanations of such receipts that might have escaped assessment.

Applicability of Section 68 of Income Tax Act 1961:

Section 68 will be applicable in the following circumstances:

- A sum is credited to the books of the Assessee and it is chargeable to income tax ;

- The Assessee did maintain books of accounts as per the provisions of Section 2(12A) including Ledgers, Cash Book, Day-book and etc;

- The Assessee could not give any explanation about the nature and source of such cash credits;

- The explanation so provided by the assessee could not satisfy the Assessing Officer;

- The Assessee did not include the sum to his total income for the previous year;

- The Assessee failed to provide any documentary evidence in support to the sum credited to his books of accounts;

- If the Assessee failed to prove the genuineness of the transaction took place to his books of accounts;

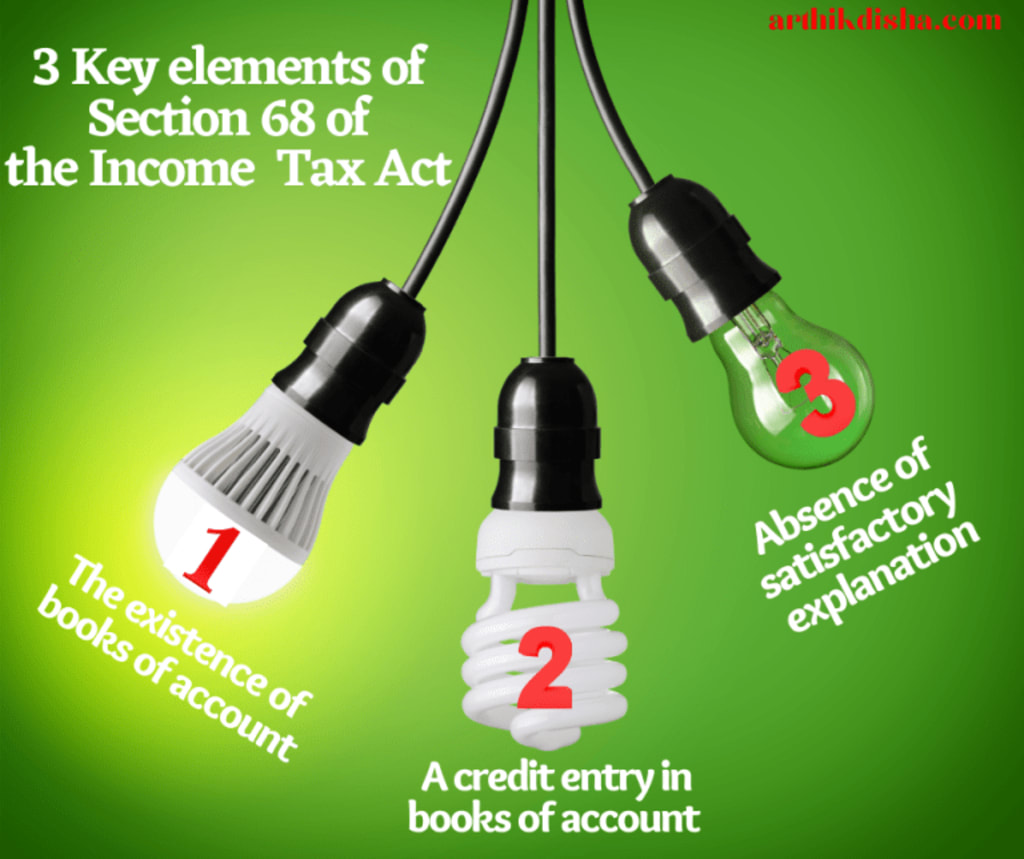

3 Key Elements of Section 68 of Income Tax Act 1961:

The powers so conferred upon Section 68 of Income Tax Act can be invoked only when there is the existence of the following 3 key elements:

1. Existence of Books of Accounts:

The first main element of Section 68 is that there must be books of accounts maintained by the Assessee. Books of accounts include Ledgers, Cash Book, Day Book and other books but not lose sheets/unbound papers that are not bundled to form a permanent book.

2. A credit in the Books of Accounts:

The second most crucial elements of Section 68 is that there is a cash credit in the accounts of the Assessee. This section is inclusive in nature and therefore incorporate other items such as gold, valuable items as the credit entries. Thus, it is not limited to cash and cash credits only.

3. Absence of satisfactory explanation by the Assessee:

The third crucial element of Section 68 is that the absence of sufficient and reasonable explanations by the Assessee to the satisfaction of the Assessing Officer.

The Assessee has to provide documentary evidence if needed in support of the cash credit in his books of accounts. But failing to prove so, may attract invocation of Section 68 by the A.O.

Taxability of Unexplained Cash Credit Under Section 68 of Income Tax Act:

Income Recognition: Section 68 of the I.T Act requires that unexplained income shall have to be recognised as income of the Assessee in the previous year in which it was received.

Section 68 of Income Tax Act Tax Rate:

Section 68 of Income Tax Act Tax Rate: Generally unexplained cash credits are taxed at a rate of flat 60% + 25% Surcharge + 6% Penalty. Therefore, the total tax rate for unexplained income stands to 83.25%.

It should be kept in mind that there is no benefit of the minimum exemption limit and also no benefit of existing tax slab of the Assessee.

Further, it does not allow any deduction from such income and no provision of set-off of loss against such unexplained income.

Section 68 of Income Tax Act Penalty:

If it is seen that the unexplained income has been considered in the income of the Assessee and tax so due has been paid on or before the end of the financial year, no penalty will be levied on such unexplained cash credits.

What are the provisions of Section 115BBE of Income Tax Act?

As per Section 115BBE of Income Tax Act, income tax shall be calculated at 60% where the total income of an assessee includes the following income:

Income generated U/S 68 to 69D: Income referred to in Section 68, Section 69, Section 69A, Section 69B, Section 69C or Section 69D and reflected in the return of income furnished under Section 139; or

Determined by the A.O: Which is determined by the Assessing Officer and includes any income referred to in Section 68, Section 69, Section 69A, Section 69B, Section 69C or Section 69D, if such income is not covered U/S 68 to 69D

Applicable Tax Rate: Such a tax rate of 60% will be further increased by 25% surcharge, 6% penalty, i.e. the final tax rate comes out to be 83.25% (including cess). Provided that such 6% penalty shall not be levied when the income under Section 68, 69, etc., have been included in the return of income and tax has been paid on or before the end of the relevant previous year.

No deduction: In respect of any expenditure or allowance or set-off of any loss shall be allowed to the assessee in computing his income referred to in clause (a) of sub-section (1) of Section 115BBE.

So, the provisions of section 115BBE of Income Tax Act 1961, read with the provisions of Section 68, is a binding provision, that makes the certain deemed income such as unexplained cash credits, unexplained income, unexplained expenditure, unexplained investment to be chargeable to income tax without allowing the benefits of basic exemption limit.

About the Creator

Arthik Disha

A Personal Finance Blogger. Passionate about finance.

Keep reading

More stories from Arthik Disha and writers in Trader and other communities.

How To Invest In Shares-Stock Market Basics India For Beginners

How to Invest in Shares- A Stock Market Basics for Indian Beginner Investors There is a great saying that a country’s economic condition can be judged by its total market capitalization. So, on the other way, a stock market’s total valuation/capitalization reflects a country’s economic prosperity.

By Arthik Disha4 years ago in Trader

THE GRAPHICS CARD WILL MEET ALL YOUR DEMANDS ON YOUR PC

In the dynamic realm of computing, few components command as much attention and admiration as the graphics card. These technological powerhouses, often referred to simply as GPUs (Graphics Processing Units), serve as the beating heart of visual processing in modern computers, enabling everything from immersive gaming experiences to complex visual simulations and professional content creation. Among the latest contenders in this arena stands the ASUS Dual GeForce RTX 4070 Super OC Edition Graphics Card, a formidable specimen boasting cutting-edge features and unrivaled performance.

By Kim Long Nguyệt Ngữ6 days ago in Trader

Valve Supplier in Nigeria

African Valve is the top Valve Supplier in Nigeria. African Valve stands as the premier supplier and manufacturer of valves across Africa with a commitment to excellence, we ensure top-notch products and services. We proudly serve clients across Africa, including Nigeria, Kenya, Algeria, Ghana, Tanzania, Sudan, and Ethiopia, ensuring reliable access to top-tier valve solutions continent-wide. As a reputed valve supplier we provide different types of valves available in different sizes and classes made with high standard material quality to meet the needs of various industries.

By african valvea day ago in Trader

The Fish Song

The room didn’t smell like disinfectants. Its fragrance seemed light and not overbearing. A soft mixture of lavender and mint permeated the space. No beeping machines or any tubes hooked up to four-year-old Kaleeka. Her cacao skin seemed to glow from the light over her head. The family, save for one and the doctors and nurses exited the room like a trail of saints showing their last vestiges of regard.

By Skyler Saunders6 days ago in Fiction

Comments

There are no comments for this story

Be the first to respond and start the conversation.