An Author Attempts Acorns

Now that we have that alliterated, here’s a review of my first month micro-investing with Acorns.

If it's a stereotype that writers are bad investors, I suppose I’ve gone ahead and enforced it. Since there are so many apps that advertise making micro-investing easy, I figured I’d give it a whirl and try squirreling some money away into investments.

It… could be going better.

Acorns is beautifully designed, I’ve got to give them that. It's a pleasure to use and navigate this app.

I’m no expert with stocks, but even with a conservative strategy, my Acorns account just keeps going down. The app doesn’t give you a ton of control on how your invested money is being allocated or what it’s being used for.

Considering how tiny my investment is, I can understand why. There are some options for the overall type of strategy you want to take; you can be conservative, moderately conservative, moderate, moderately aggressive, or aggressive. I was on the conservative option while seeing these losses.

Here’s a little screencap of what conservative versus aggressive looks like as far as portfolio distribution goes.

With a $30.57 investment split around in different sources, the percentage I have in shares is pretty miniscule, so I can understand why large changes in the market aren’t impacting the account too much. It’s only been about a month, but for a newbie, it’s still a bit disheartening to lose 1.53%, or 0.47 cents, of my tiny investment. Since I took the conservative strategy, I had hoped for it to either stay at the same amount or perhaps have a few cents of growth.

Here’s a little tour of my account.

The summary happily shows you when your balance goes “up” because of dividends, but it doesn’t show you when it goes down because of losses. This format seems to highlight the good and push the bad under the rug.

This makes me suspicious of Acorns; I'd rather see the incremental cents coming and going in the day-to-day summary rather than just when pennies come in.

You’ll see that little “Partner Reward” on my account; I decided to give this a try because my cell provider, Verizon, was doing a little bonus in their rewards program where you could get $15 deposited into your Acorns account for investing $10. I also did their round-up feature, which rounds up the cents on your recent transactions and invests the spare change. This sounds like a cool option since it’s a convenient way to add to your savings in small, almost unnoticeable increments, but there are plenty of traditional savings accounts out there that will do the same thing.

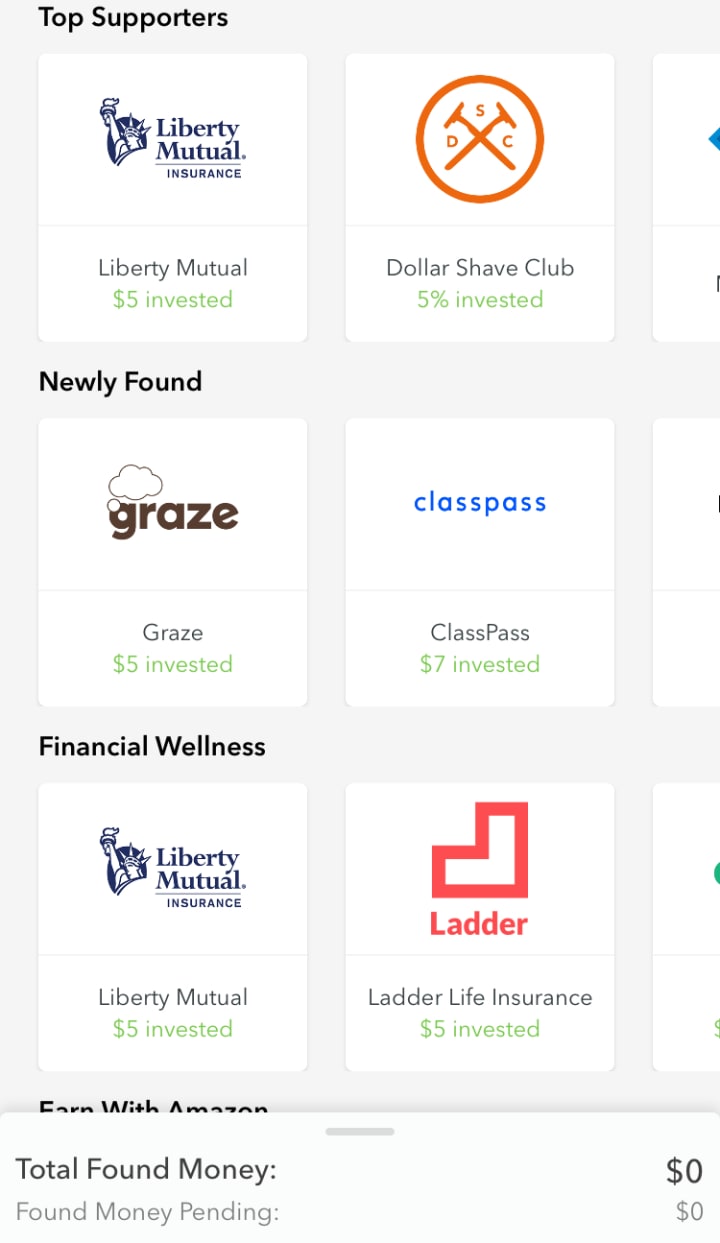

However, it’s the Found Money feature of Acorns that makes me want to take the money and run.

Here’s what that section of the app looks like as of October 2018.

Dozens of businesses will give you a little kickback into your Acorns account if you purchase their goods or services. Acorns will constantly give you information on these opportunities.

Which sounds cool! $5 or more invested here and there, that sounds awesome.

However, in my humble opinion, it makes Acorns feel more like another one of the rewards apps out there like Drop and Ibotta rather than a true tool for investment.

If you want to use it as a rewards app to get little bonuses on your purchases from Dollar Shave Club, Apple Music, or Blue Apron, then that could bring you in some cash.

I feel like this is the only way to make your Acorns account truly profitable. You can make a lot this way. For example, Blue Apron will invest a whopping $30 into your account if you’re a new subscriber to their services. There are some businesses in there that I frequent, like EyeBuyDirect and Expedia, which give 4% and 5% of your purchases back as investments.

It does beg the question if it’s truly worth it, though. Like a lot of rewards programs, you have to go through the app, click their special link, make your purchase in the same session, and so on. Personally, I feel going to the trouble to reap these rewards to watch them slowly deteriorate in my portfolio seems a bit high effort. I just don’t shop from the affiliated vendors often enough to really make the most of that program.

However, if you think of Acorns as a rewards app and hit the Found Money feature hard, you’ll probably be fairly happy with the results you get.

I'm writing this piece to give you an honest and upfront review of my experience with one particular micro-investing app.

If you just want to start saving casually, I’d recommend just opening a traditional savings account rather than investing with Acorns. There are a few banks with savings accounts out there that will give you around 1%, perhaps a smidge more if you Google around for them. These are obviously tiny percentages and don’t yield a whole ton of money, but again, if you want to start casually, it’s a very reliable and safe way to do it.

If you want to start saving more seriously, then I’d definitely suggest you chat with finance folks and not a writer like me who only took statistics in college!

If you really want to delve into investing, I’d consider going for a more traditional route with advisors and the like. I could see myself giving traditional investing a go in the future if I ever had enough money to do it, but I don’t think I’ll be sticking with Acorns.

I’m going to channel my inner squirrel, gather up my nuts, and take them to a differ tree.

If you had a different experience, I’d love to hear! I’m always available on Twitter as @SleeplessAuthor and on Instagram as @SleeplessAuthoress if you want to chat.

About the Creator

Leigh Fisher

I'm a writer, bookworm, sci-fi space cadet, and coffee+tea fanatic living in Brooklyn. I have an MS in Integrated Design & Media (go figure) and I'm working on my MFA in Fiction at NYU. I share poetry on Instagram as @SleeplessAuthoress.

Keep reading

More stories from Leigh Fisher and writers in Trader and other communities.

You Can Still Finish Your Degree While Working Full-Time

Getting a degree when you work full-time is one of the most challenging things a person can do, but if you have a firm objective, it’s worth chasing. If you know what career path you want but you need a degree to get there, you can still do it even if you’re a non-traditional student.

By Leigh Fisher6 years ago in Education

"Stride in Style: Discover the ALDO Men's Albeck Oxford"

In the realm of men's footwear, finding the perfect balance between style, comfort, and versatility can often feel like an elusive quest. Yet, amidst the sea of options, there emerges a beacon of excellence that embodies these qualities seamless: the ALDO Men's Albeck Oxford. As a distinguished member of ALDO's esteemed lineup, the Albeck Oxford stands as a testament to the brand's commitment to crafting footwear that not only exudes sophistication but also delivers unparalleled comfort and durability.

By Kim Long Nguyệt Ngữ3 days ago in Trader

2023 Fashion Designer Shoes Men Casual Platform Sneakes Lace Up Trainers Student Sneakes Mens Vulcanized Shoes Zapatillas Hombre

In the ever-evolving world of fashion, footwear has become more than just a functional accessory; it's a statement of style, personality, and individuality. One of the most intriguing trends to emerge in recent years is the fusion of casual comfort with elevated design, epitomized by the rise of platform sneakers for men. These shoes seamlessly blend streetwear flair with high-fashion sensibilities, creating a versatile option that can effortlessly transition from day to night, casual to formal.

By Wedson Vegasabout 15 hours ago in Trader

Comments

There are no comments for this story

Be the first to respond and start the conversation.