A Microcap's Guide to Uplisting

Uplisting from the OTCQB to the NASDAQ is the dream for all microcap companies and the entrepreneurs that run them.

Statistically, most microcap OTCQB companies fail. Only the great ones don’t and only the very best ones make it to a higher national exchange.

There are very limited paths to a NASDAQ listing. Some VC and private equity-backed companies, such as operationally laden Vice Media founded by Shane Smith and listicle behemoth Buzzfeed, to name a few, learned the hard way that an IPO is not a sure thing. Competition for capital is fierce and valuations hard to determine. Under all circumstances though, almost any founder-CEO needs money to make money to stay afloat, until they prove their true value.

Over five years ago, when Vocal was still just an idea in mine and Justin’s minds, we found ourselves at a crossroads. How would we go about financing a vision with no revenues and no development team, knowing that if we could “build it, it would work, and they would come?” We were on a mission to build the foremost creator platform online. While we knew we had a product in Vocal that venture capital or private equity firms would be attracted to, we also knew that it would be nearly impossible to get people to fund the development of a product that was still in its infancy. While Vocal's proof of concept was not yet achieved, we found our first party data analysis very promising.

Vocal is Born

My personal financing as well as my friends and family were the Company’s angel financing network. Jerrick engaged our platform development partner Thinkmill in late 2014. It was two more years before we got to a minimum viable product and launched the Vocal platform for creators. We had a clear vision of the foundational architecture of a next-generation technology company. Jerrick synthesized my institutional financial services background with Justin’s exceptional design ideology. By late 2015 we had proof of concept for revenues and determined a direction for future capitalization and funding requirements.

In early 2015 we started to reach out to a number of advisors who were familiar with the OTCQB marketplace. By late 2015 we had identified a public entity into which we could integrate our growing intellectual property and technology. Jerrick purchased it with equity, changed the name to Jerrick Media Holdings, Inc. and began trading under the ticker JMDA in February 2016. With no volume to speak of, limited legacy revenues, but a quality investor base, the market settled on a share price hovering between $3.00 - $4.00 (post 20-to-1 reverse split). It stayed that way up until recently, irrespective of any fundamental advances the company and its technology were making.

Our general thesis was to create a growth and value proposition for investors in JMDA. Jerrick's fundamental goal from the start was, and continues to be, a company that embodies the institutional disciplines that are inherent to the financial services industry, with the design elements and technology resources that can create scalable, sustainable, and defensible technology products.

What is an Uplisting?

Exchanges like the Toronto Venture Exchange, the OTCQB and the London AIM exchange are often referred to as “lite exchanges,” which offer great promise but a statistically low probability of success for investors and the companies they invest in. These lite exchanges have looser listing rules, and are tailored towards smaller and more speculative ventures.

Theoretically it is easier to generate returns on a microcap stock compared to a large cap stock. In actuality, though, the scope of the microcap space is such that finding the right opportunity is time consuming and requires the most stringent of due diligence investigations to find the diamond in the rough, let alone capable individual executives and management teams. Even once identified, generating awareness and liquidity on the lite exchanges is a herculean feat.

Why Uplist?

Many quality funds have mandates that preclude them from investing in illiquid and/or OTCQB traded entities. This, by definition, limits shareholder access for many lite exchange companies, and means that listing on a national exchange exponentially opens up the universe of potential investors.

With these newly opened doors, recently uplisted companies benefit from higher trading volumes and, as a result, greater liquidity. Liquidity can be a key factor in a fund manager’s decision to own a stock, as well as financial and other structural factors.

After uplisting, companies may experience significant daily volume increases. Additionally, by virtue of trading on a national exchange, companies may meet the threshold for many Wall Street analysts to cover the company with research. In other words, listing on a main exchange is like a stamp of approval from Wall Street. Garnering research opportunities helps to broaden visibility, awareness and extend reach to new investors through their sales organizations, thus potentially driving further revenues. All of this factors in and creates self-propelling momentum for an uplisted security.

In essence, being on the NASDAQ means more eyeballs on your company, and the opportunity for legitimacy in an ever-increasingly difficult market for young companies to find funding and awareness.

What are the odds of success?

Only 60 companies on average achieve an uplisting each year, representing just 0.0052% of the 10,000 stocks on the OTCQB. Of the companies that uplist, approximately 75% of them uplist to the NASDAQ, as Jerrick plans to do.

There are several important factors that go into determining if, and when, a company decides to uplist, primarily cost, ongoing listing requirements, timing, and adequate advisors. Perhaps most important, though, is a stomach of steel. Only those companies with the most meticulous of business plans and the most qualified of management and advisory teams should even attempt uplisting.

There are 2 ways to be listed on an exchange like NASDAQ: IPO or Uplist

Qualifying for a “main exchange”—like NYSE, NASDAQ, LSE or TSX—is rare at best for a small private company. The process takes years of commitment and willpower. In the absence of an IPO, it is equally rare for a company to upgrade, or uplist, to a main exchange.

An uplisting is viewed generally as a positive development by investors. It means that the company has met certain regulatory standards that warrant its listing to a national securities exchange. With an uplisting, companies hope to improve awareness, price, and liquidity of stock as well as potential of appreciation, as a wider swath of investors can now purchase shares. The flip side is that many can sell shares.

One of the most critical factors before uplisting is to determine the business nature of those that finance the company, the quality of the investors, and the time horizon of their investment. There are many hedge funds who claim to offer uplist financing, but have actually engineered near riskless trades for themselves that offer less incentive for upside and arguably draconian protection against downside. That is why the majority of uplisted microcap stocks eventually trade down, with many of them even being delisted. It is essential to have an investor base that is committed to the success of the company collectively.

An uplisting is often accompanied by some form of capital raise and the associated filing of a Form S-1 to reserve and register new shares to be issued. The S-1 filing must be reviewed and approved by the SEC before the shares can be issued and listed. The S-1 is widely seen as the kickoff filing event for a company’s new listing. It serves simultaneously as the notification of newly registered shares, a signal that a capital raise is imminent, and a chance to strengthen its business plan and growth strategy.

Listing Requirements

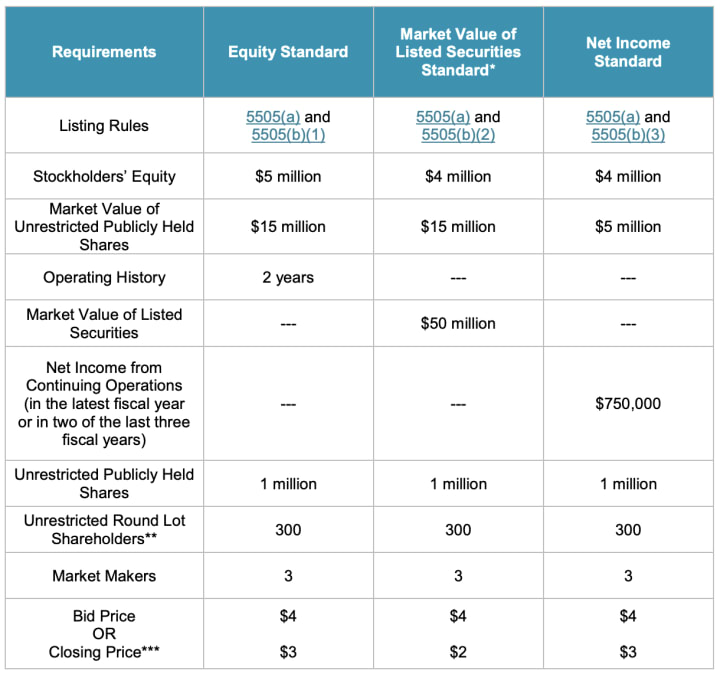

There are three main standards under which a company can get listed on the NASDAQ: the Equity Standard, Market Value of Listed Securities Standard, and Net Income Standard. For small and microcap companies, the Equity Standard, which means reaching a minimum level of stockholders’ equity, is a common path towards meeting the uplisting criteria. Jerrick applied under the Equity Standard, which requires that its uplist transaction is priced at $4.00 or above on the date of uplisting.

The intense scrutiny is why it is imperative to factor in long-term objectives and milestones when considering an uplist. The requirements have changed over the last 5 years and continue to evolve on a regular basis, so uplisting candidates should consistently adapt best practices and check the Nasdaq site for regular updates to avoid delays.

Of all the requirements that must be met for each listing standard, there are three that tend to be the steepest for uplisting companies to overcome and require advanced coordination.

1. Minimum share price

Depending on which standard a company uplists under, a minimum share price needs to be met either as of the day of uplist or for a specified pricing period before it can be approved for uplist. In order to reach the minimum share price requirement, many companies need to enact a reverse split. Executives generally time the split either immediately preceding or in conjunction with the uplisting. The key is to ensure that the timing and ratio of the split will leave you above the minimum share price for whatever time period your listing standard requires, while still leaving enough shares available to raise additional capital needed to meet other listing requirements. The stability in a stock often depends on an organized investor relations and outreach strategy that is both transparent and aggressive.

2. Minimum cash on balance sheet

Both the NYSE and the NASDAQ require companies to prove that they have sufficient cash on hand to continue operating for 12-18 months after the time of listing. The company will often be required to raise capital in order to satisfy this requirement. Cash raised for this requirement also helps companies satisfy the minimum stockholders’ equity, another requirement that must be met prior to listing. The minimum required stockholders’ equity varies based on which listing standard a company is applying under.

3. Minimum number of shareholders

Both exchanges also require a minimum number of shareholders. Among other purposes, an uplist financing serves to ensure that a minimum number of shareholders is met, the purpose being to create liquidity in the marketplace post-uplist. More important is a consistent communication strategy that diversifies and increases the shareholder base. This type of strategy should be implemented from the very beginning of the company’s narrative. The key to finding new investors is disseminating the company’s story through public and transparent awareness programs.

Application and approval process

Companies must file an application and be approved for listing by the selected exchange. The application process includes detailed information on the major shareholders, management team, and reporting practices.

Particular scrutiny is given to the board of directors, including requirements that the majority of directors are independent and corporate governance committees are intact. Determining the makeup, responsibilities, and scope of the board should be made well in advance of the uplisting process. After a company meets the requirements for an uplisting, approval can occur relatively quickly. If an application is not approved, the exchange will typically work with the company on solutions and/or extend the timetable.

Why now is the right time for JMDA

The vast majority of my time in the past 5 years has been directly or indirectly preparing for this very moment. We painstakingly carried out not only a bottom-up financial analysis of the company, but a top-down analysis to make sure that allocation of technology and operational resources were consistent with the overall strategy and core principles of the company. Our financial, product development and business intelligence groups have, for their parts, fine-tuned what has evolved into an extensive financial model with realtime and historical data that serves as proof of concept for Vocal, our technology, and an indication of significant growth opportunity going forward.

Preparing a company for an uplisting has been a richly rewarding and equally humbling experience. Without the confidence of our shareholder base and the talent of Jerrick’s executive team, JMDA could not have arrived at this moment equipped for success.

About the Creator

Jeremy Frommer

Chairman & Co-Founder of Creatd ($CRTD) and Vocal. We have much work to do together.

Keep reading

More stories from Jeremy Frommer and writers in Trader and other communities.

Reversing Forward

Reversing to move forward is part of Jerrick's journey from the OTCQB to the NASDAQ Capital Markets. From inception, Jerrick's goal has been to build a billion dollar company. In fact, that goal drove our decision to go public in the first place. While Jerrick Media Holdings, Inc. became a publicly traded company in February 2016, my particular journey to that point can be traced as far back as 1990.

By Jeremy Frommer5 years ago in Trader

ONE OF THE SAFEST MICROWAVE OVEN IN THE WORLD

In the bustling hub of today's kitchens, few appliances stand as indispensable as the microwave oven. From reheating leftovers to cooking quick meals, these modern marvels have revolutionized the way we approach food preparation and convenience in our daily lives. Among the myriad options available, the BLACK+DECKER EM031MB11 Digital Microwave Oven with Turntable Push-Button Door emerges as a standout choice, combining functionality, safety, and sleek design to meet the diverse needs of contemporary households.

By Kim Long Nguyệt Ngữ6 days ago in Trader

The Business of Nature

Dew drops reflected the light of the sun. The inhabitants of Whispering Woods woke up to the golden droplets of water on the leaves of the flora. The oaks particularly enjoyed the light and the maples did, too. Happiness enveloped all who lived there, even the rocks that cried out in the night delighted in the morning.

By Skyler Saundersabout 17 hours ago in Fiction

Comments

There are no comments for this story

Be the first to respond and start the conversation.