Saving Money Is A Full-Time Job

How a change of mind and 3 simple things can save you thousands

It’s not even the 15th yet and you have already spent most of your money for the whole month.

You only carry about 20 bucks in your pocket because you know if money is in your purse you will spend it.

You really want these new shoes but you have no savings.

Do these situations sound familiar? Then you are at the right place!

This is a How to Save Money 101 class. It is not about how to make more money or how to save 500$ when you have an income of 3000$ on a monthly basis. I want to help those who struggle with money in general and show them how to make the most of it. Saving money efficiently is not an easy task and requires work and a beneficial mindset. It has to be part of your daily life — like a full-time job.

Here are things that helped me to save thousands over the last few years:

1. Train yourself to get a feeling for money — all your money

One of the most ridiculous things I hear from people who struggle to save money is that they tend to carry only about 20$ to 60$ in their pocket with the explanation that the more cash they see in their purse the more likely they will spend it.

This sounds crazy to me.

When I say you need to get a feeling for money, I mean you should have an overview of all the money you have — whether it be in your pocket, your bank account, or the loose change lying around on the coffee table. This is crucial to be able to save money efficiently.

That way it should not matter if you carry around 10$, 70$, or 200$. If you are aware that the money in your pocket is just one part of your big stock of capital, you will be aware of the full weight of your next purchase and hopefully will not be surprised when you take the next look at your bank account.

2. Write down every transaction you make — every single one

This is the most annoying one as it comes with the most work but it is also the most helpful one. Make sure to keep track of every purchase you make. And I mean every single one.

30$ for groceries? Write it down.

14.39$ for a new book? Write it down.

2$ for a new pencil? Write. it. down.

With this technique, you will never get surprised by a low bank balance ever again. You will also always know much money you still have left for the month — an important point I will come back to a little bit later. And last but not least, you can look back at the month and reflect on your purchases and your personal buying behavior in order to find bad habits.

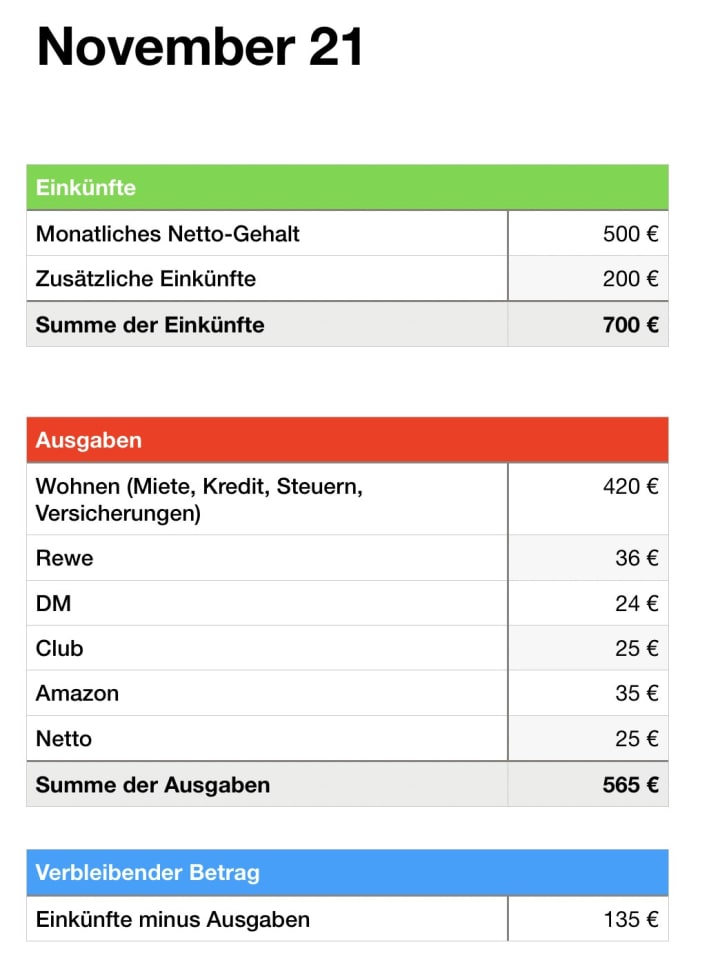

A possible transaction list could look like this:

Please don’t get confused by the german.

The green one says “income” and marks all the money I gain over the month - Be it through a job, something I sell, or any other way I can get to more cash. Here, we have a total of 700€ for the whole month.

The red one says “purchases” and marks all the money I spend over the month while the blue one on the bottom tells me how much money I have left — or when it’s the end of the month how much is saved. As you can see I spent 565€ over the whole of November, which leaves me with 135€ in the end that I can put in my saving stock.

3. Think monthly income — not yearly or weekly

Let’s say you have 500$ monthly for your own use. With this money, you have to cover food, clothes and any fun activities with your friends. At the end of the month, you have 100$ left. These 100$ are saved.

The next month comes around. How much money do you have to make it through the month? 500$. The saved 100$ from last month will not be considered accessible money for this month.

Make sure to reset the amount of cash you feel comfortable spending per month and do not just look at your bank account and consider all the money you have as accessible.

I personally prefer to think in monthly stages. Week to week gets frustrating way too fast as it needs much more planning and organization while yearly is way too late and won’t make for a useful saving plan.

Furthermore, I recommend having a list of your monthly savings for organization purposes. For example, to keep track of my yearly progress I use the same template as for my monthly purchases:

To summarize again: To save money on a regular basis you have to

- get a feeling for all of your money and always have an overview of your whole capital

- keep track of every purchase you make

- think from month to month and reset the amount of “accessible” money every month as well

Doing all these things requires a change of mind when it comes to money in general. It is work, it is dedication. But I promise, once you have integrated those tools into your day-to-day life, saving money will become a lot easier than before.

...

If you liked this article you may also like my Valentine's story or my view on online classes and why I miss them

About the Creator

M.J. Rausch

Geek, wannabe pedagogue and relationship Guru. Come and laugh at me - I mean with me

Keep reading

More stories from M.J. Rausch and writers in Lifehack and other communities.

Different Roles in Toxic Families

I already talked about Disney's new animation movie Encanto and what it has to say about toxicity within a family. But because this movie is brilliant, it doesn't stop there. The movie made sure to portray the different roles people can take on in these problematic households and utilizes the concept of superpowers to its full potential when the powers of the Madrigal Family correlate perfectly to the tasks they have to fulfill in their toxic family dynamics.

By M.J. Rausch2 years ago in Geeks

10 EASY DIY SUMMER COCKTAILS

Here are 10 easy summer cocktails. It is party season and it is the summer time and if you are a cocktail enthusiast, you are probably the one that everyone goes to create the cocktails for your parties, so I thought I’d make it easier for you guys and give you guys 10 easy very refreshing crowd-pleasing cocktails to make for your friends and then you can be the hero of all your parties.

By Ngozi Otoecherea day ago in Lifehack

Comments

There are no comments for this story

Be the first to respond and start the conversation.