GST Return Filing

Benefits Of Return Filing On Time

What is the New GST Return System?

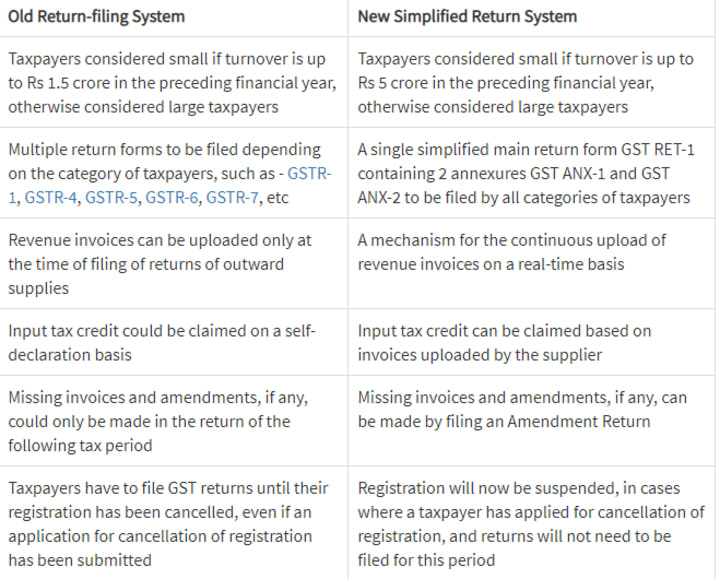

At the 31st GST Council Meet, it was decided to introduce a new Return Plan under GST for taxpayers. This return plan will contain simplified return forms, to facilitate filing for taxpayers registered under GST. Under this New Recovery Program, there will be one main GST RET-1 return and 2 GST ANX-1 and GST ANX-2 connectors. This refund will need to be lodged on a monthly basis, with the exception of small taxpayers who may choose to lodge the same quarterly term. Minor taxpayers are taxpayers with a profit of up to Rs 5 crore in the previous financial year.

Forms to be filed under the New GST Return System

The GST RET-1 principal refund will contain details of all transactions, tax credits incurred, and tax payments, plus interest if any. This return will contain two additional forms namely GST ANX-1 and GST ANX-2. The GST ANX-1 (External Expenditure Addendum) is a detailed reporting of all foreign supplies, internal goods responsible for deferral charges, and imports of goods and services, which will need to be reported as invoices (excluding B2C items) in real-time. GST ANX-2 (Appendix) will report details of all internal feeds. Most of this information will be automatically generated from data uploaded by providers in their GST ANX-1. The recipient of the goods will be able to act on these automated documents, which will be available to them in real-time.

Differences between Current Vs New GST Return Systems

Transition plan to the New GST Return System

The new GST Return program has been piloted from July 2019, and the full program will be rolled out from April 2020 (early October 2019). This transformation plan will be implemented in a phased manner. The pilot phase will be for users to familiarize themselves with the add-ons for the new recovery program.

The previously announced reform program was as follows:

From July to September, during the trial period, taxpayers will continue to submit their GSTR-1 and GSTR-3B forms according to the current system. From October 2019, GST ANX-1 will need to be installed by senior taxpayers, who will replace GSTR-1. However, GSTR-3B will still need to be installed until November 2019. In the case of small taxpayers. they will need to pay taxes using PMT-08, which will replace their GSTR-3B refund.

From December 2019, major taxpayers will have to start installing GST RET-01, which is a major return under the new repayment system. For smallholder taxpayers, their first GST RET-01 will need to be rolled out in the October-December 2019 quarter.

To learn more about switching to the New Return System, click here.

Offline Demo Tool Prototype

GST Network (GSTN) has introduced a web-based interactive tool for offline tools

of the new recovery program. With this demo version of a particular type, the taxpayer will be able to navigate through various pages. This prototype will also allow the user to experience a variety of functions such as drop-down menus, invoice uploads, in-app purchasing confirmation (system-based) purchases, etc.

The taxpayer will be able to analyze and identify the realities of GST's simplified reimbursement for this type. The user can then share feedback or suggestions via GSTN.

Click to learn more about configuring GST ANX-1 and taking action on GST ANX-2 in offline toolbar icons.

Important Changes introduced in the New GST Return System

The Harmonized System of Nomenclature (HSN) code will be required to submit information at the document level (on a profit basis) compared to a separate HSN summary.

The user will also receive HSN with his or her GST ANX-2, wherever the supplier had to announce the HSN code.

B2Bassets, which are responsible for reversing the charging method do not need to be specified by the provider in GST ANX-1, however, the aggregate amount will need to be shown in GST RET-1.

Internal assets binding to RCM must be announced on GST ANX-1 at GSTIN level, by the consignor.

The B2C-L concept has been removed. The interest rate for three-quarter contributors (small taxpayers) will be taken as Rs 5 compared to the current limit of Rs 1.5 crore.

The recipient can report missing invoices at the invoice level (this is when the supplier did not upload the invoice within T + 2 period).

Upload of Invoices under the New GST Return System

Missing invoices:

Whenever a supplier has not uploaded an invoice or a debit note, and a recipient claims ITC, it will be termed as “missing invoices”. When ITC is availed on missing invoices by a recipient, and these missing invoices do not get uploaded by the supplier within the stipulated time frame, then the ITC availed with respect to such debit notes/invoices will be recovered from the recipient.

Locking of invoices:

A recipient will have the option to lock in an invoice if he agrees with the details reported in that invoice. If there is a huge volume of invoices, it may not be practical to lock in individual invoices, and in such cases, deemed locking of invoices will be done on those invoices uploaded which are neither rejected nor have been kept as pending by the recipient.

Unlocking of the invoices:

An invoice on which ITC has already been availed by a recipient will be considered a locked invoice, and will not be open for amendments. In case an amendment needs to be made to a particular invoice, the supplier will have to issue a debit or a credit note. An incorrectly locked invoice can be unlocked by the recipient online, subject to a reversal of the ITC claim made, and an online confirmation thereafter.

Pending invoices:

An invoice that has been uploaded by a supplier, however one of the following scenarios applies to that invoice:

The recipient has not received the supply

The recipient is of the opinion that there is a need for an amendment in the invoice

The recipient is unsure about availing of ITC for the time being

An invoice in such cases will be marked pending by the recipient, and no ITC will be availed by a recipient on these pending voices.

Rejected invoices:

When the recipient’s GSTIN is filled incorrectly by the supplier, the invoice will be visible for a taxpayer who is not the receiver of such supplies. As ITC will not be eligible to be taken on these invoices, the recipient will need to reject these invoices. To make the task of rejecting invoices hassle-free, the matching IT tool will have the option to create a recipient/seller master list via which the correct GSTIN can be identified.

About the Creator

Arvian Business Solutions PVT LTD

Arvian Business Solutions provides fully serviced individual & executive offices, team spaces, and virtual office solutions. You’ll find everything you need to stay connected and focused on your business.

Keep reading

More stories from Arvian Business Solutions PVT LTD and writers in Journal and other communities.

Register For a Trademark in India

What is the Importance of Trademark Registration in India? The trademark plays an important role in promoting goods and provides information about product quality. Enables an entity to acquire individual rights to use, distribute or distribute the marker. This can be done by trademark registration. India is a very competitive market for business owners and company owners, where there are a large number of similar products/products that continue to emerge on a daily basis. Here, to protect your product is necessary to prevent anyone else from using your name or brand name. In this article let us discuss the need/importance of trademark registration in India.

By Arvian Business Solutions PVT LTD3 years ago in Journal

What Are The Benefits of Blogging?

In today's article you will know what are the benefits of blogging. What Is Blogging? Nowadays many people like to do blogging. Blogging is like an online business and you can create your own blog website. Those who want to do this business will have to buy a domain which is not expensive but hosting is also available.

By aman ghanshala4 days ago in Journal

Gossamer

"Murray! Wake up!" He loved that period between waking and dreaming. To him, it was like entering another dimension; more of a dreamscape than dreaming itself. There was an otherness to it that he wanted to grasp and yet deeply respected the fact that it could never be his totally. This is what gossamer was; flighty and light, a wisp of smokiness, an idea suggested but not fully revealed, a slit in cloth, a copse in the wood.

By Rachel Deeming7 days ago in Fiction

Comments

There are no comments for this story

Be the first to respond and start the conversation.