What is the Impact of War on the U.S. Economy?

Interest Rates, Stock Markets, Oil Prices and More

Financial Markets are always on alert when a threat or actual war erupts. To review this issue, we examine reactions in the U.S. bond market, U.S. oil markets, the U.S. growth trajectory, and the U.S. equity market. The results may be surprising to some, but to seasoned investors, the results should not come as a shock!

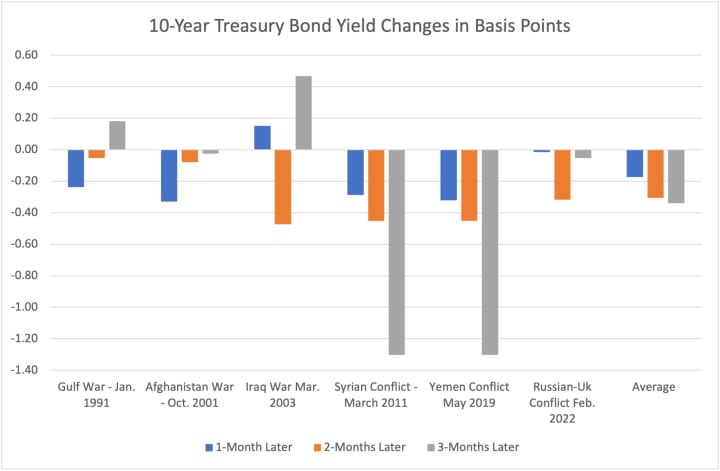

Bond Market

Interest rates are top of mind for investors, given that (since March 2022), the Federal Reserve has hiked short-term interest rates by 525 basis points. As a result, we examine whether the latest Middle East war could push interest rates higher or lower. The evidence reveals that the 10-year Treasury yield, which has risen from 0.54% (March 9, 2020) to 4.64% (Oct. 13, 2023), has moved lower in recent military conflicts as investors have treated U.S. Treasury debt as a safety haven. Still, there is a myriad of factors that can impact Treasury yields at any given point in time, as we have highlighted in prior research. This week, for example, bond traders were disappointed with the latest Consumer Price Index report, which came in slightly above market expectations.

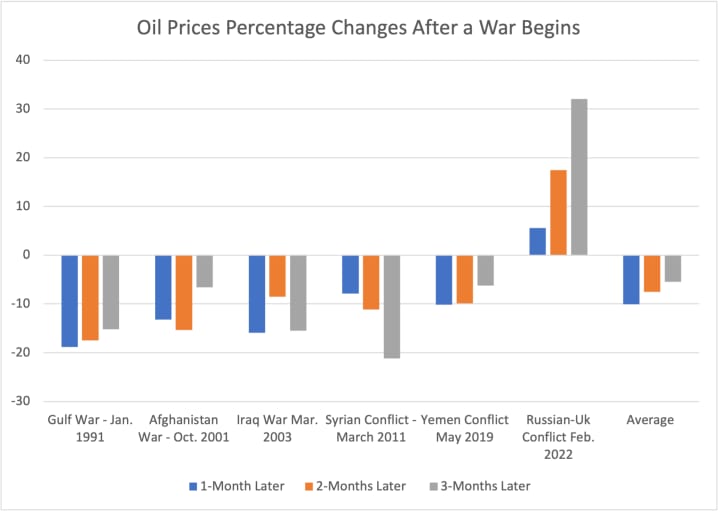

Oil Prices

Another concern circulating in financial markets is that a Middle East conflict can reduce global oil supplies if some countries face stricter restrictions in distributing their petroleum output. By way of example, at the time of this writing, oil prices were moving higher on concerns that the U.S. would impose tighter restrictions on Russian oil exports.

Oil prices could also rise if some OPEC countries use their oil output to influence the war's outcome. Higher oil prices tend to hurt global economic growth and increase inflation pressures. The latter could lead central banks to keep interest rates high to combat inflation, hurting economic growth.

However, except for the Russian-Ukraine military conflict, recent military skirmishes have failed to boost oil prices. Last year, oil prices increased as Russia and OPEC+ chose to restrict output. The big question is whether this group will cut production further beyond its +2.0 million plus barrels of oil per day if this military conflict escalates.

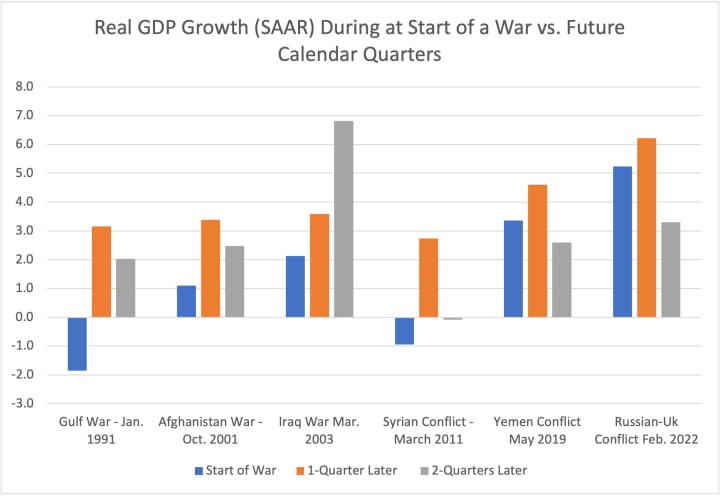

U.S. Economic Growth

A logical extension of our analysis is to track U.S. real GDP growth after military conflicts have started. The evidence fails to find any direct link between the onset of wars and slower U.S. economic growth. Going into the current military battle, the well-respected Atlanta Fed Nowcast GDP model forecasts Q3 2023 Real GDP growth by an outsized +5.1%! That represents a significant cushion over U.S. potential growth of +1.8% and suggests that any speculation that the U.S. economy is in a full-fledged recession is ludicrous. Of course, there are some sectors at any given time that may be suffering recessionary conditions, but a genuine downturn requires that 51% or more of the U.S. economy be experiencing such conditions! As I was reminded recently, just because my right shoulder is hurting doesn’t mean I can't use the strength from my left shoulder to carry a bag of groceries!

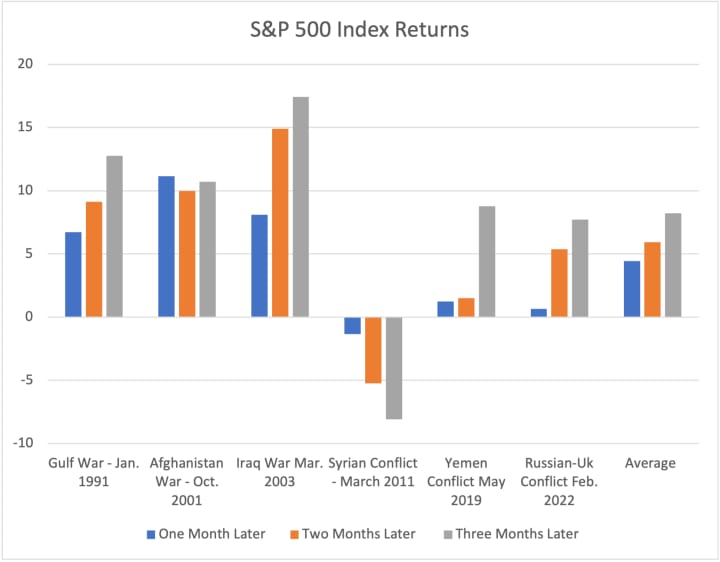

Impact on U.S. Equity Markets

Saving the best for last, some investors have speculated that whenever a military conflict gets started, many things can unravel, and eventually hurt equity prices. Yet apart from the Syrian war, U.S. equity prices have generally increased after a military skirmish. Such evidence suggests that while a military conflict is never a welcome development, it rarely generates lower stock prices!

Summary and Concluding Thoughts

Our analysis suggests that the most significant impact of military conflicts is the human toil that it extracts from both sides. The effect on the bond market is to lower long-term interest rates as the “safety haven” effect springs into action. Oil price movements tend to reflect the behavior of oil-exporting countries, given that the global oil market is less than competitive.

The U.S. economy tends to be boosted by higher military spending, often associated with taking sides in the conflict, which supports economic growth. The combination of these factors, with few exceptions, has historically supported U.S. equity prices.

About the Creator

Anthony Chan

Chan Economics LLC, Public Speaker

Chief Global Economist & Public Speaker JPM Chase ('94-'19).

Senior Economist Barclays ('91-'94)

Economist, NY Federal Reserve ('89-'91)

Econ. Prof. (Univ. of Dayton, '86-'89)

Ph.D. Economics

Keep reading

More stories from Anthony Chan and writers in Trader and other communities.

How the U.S. Can Boost Oil Production and Lower Gasoline Prices?

An increase in oil output would be supported by some climate change advocates if it is temporary until the United States transitions to renewable energy sources. In contrast, some support increased energy production to help ensure the United States recaptures its energy independence status.

By Anthony Chan2 years ago in Trader

Comments

There are no comments for this story

Be the first to respond and start the conversation.