Path-Breaking Research Explains Low Consumer Gallup Poll Readings

Why Are Consumers So Depressed?

If an Economist living on Mars came to the U.S. and learned that the U.S. economy expanded by 3.3% in Q4 2023 and was expected to grow by +3.4% in Q1 2024 (according to the widely respected Atlanta Fed nowcast GDP model) with an unemployment rate hovering around its lowest reading in 50 years, she would predict that consumers would be happy. Both real GDP growth rates exceeded the U.S. potential growth rate of +1.8%.

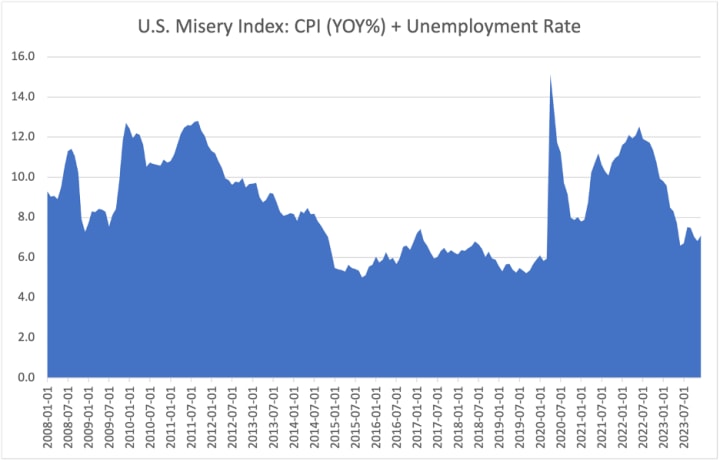

Yet, reality is far from this outcome! Even the U.S. Misery Index, created by an Economist named Arthur Okun, doesn't explain why consumers remain so glum. That index is constructed by adding the 12-month growth rate in the headline Consumer Price Index (CPI) plus the national unemployment rate! The index has dropped sharply but consumers are still unhappy. Lower readings are desirable, while higher readings are unfavorable!

What are U.S. Gallup Polls Telling Us?

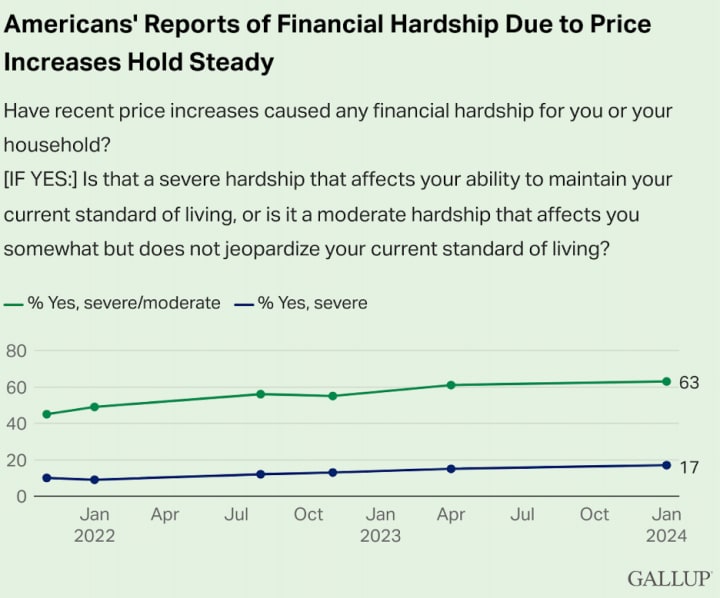

The number one factor mentioned in the widely circulated Gallup Polls is inflation! In a recent Gallop Poll, 63% of Americans view inflation as a severe economic hardship that has painted a dark cloud over their outlook. Many believe wages are not keeping up with the rise in consumer prices.

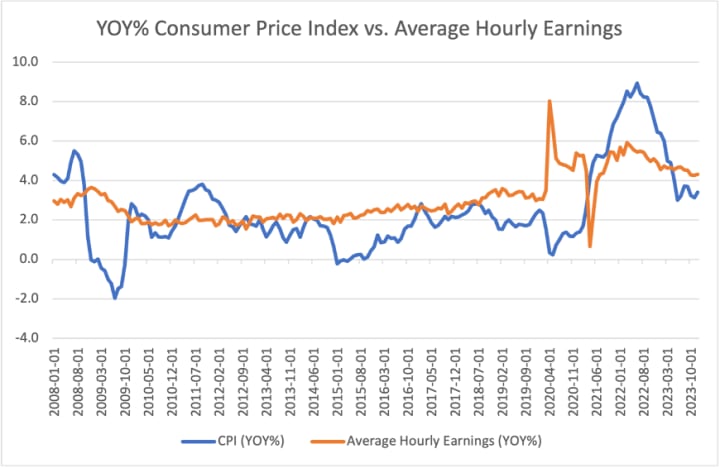

However, a closer look at the latest Consumer Price Index (CPI), which released its latest historical revisions for the past 5 years on Feb. 9, 2024, revealed the index stood at 257.971 (Jan. 2020) just before the global pandemic hit and rose by 18.9% to 306.746 through Dec. 2023! By comparison, wages or average hourly earnings for all workers rose from $28.44 (Jan. 2020) by +21.5% to $34.55 (Jan. 2024). Usually, we don’t get excited with CPI annual revisions, but last year, the data was revised from an annualized Q4 2023 CPI gain of 3.1% to 4.3%. That caused us to wait to publish this article until after the Bureau of Labor Statistics (BLS) released the latest revisions to give our readers the most accurate data description. In the newest revision, the yearly gain through Dec. 2023 was revised upward to +3.4% from +3.3%.

From a non-partisan perspective, such data suggests concerns that wages have not kept up with inflation are unwarranted. However, recent economic research reveals that individuals do not analyze data this way. Instead, Americans incorporate the effects of inflation with a lag. That means that despite the sharp drop in the yearly growth of the CPI from +9.1% (June 2022) to +3.4% (December 2023), consumer sentiment is usually determined by inflation readings observed 6 to 12 months ago! This means it may take many more months for Americans to incorporate the recent U.S. declines in inflation fully. The study also finds that Americans tend to be risk-averse when viewing inflation. In simple terms, this means that the adverse effects of rising inflation outweigh the positive impact of equivalent declines in inflation.

Let’s think outside the box for one moment. This line of consumer reasoning makes sense because Fed Chair Powell has stated that the Fed intends to lower interest rates only after it is fully convinced that the downtrend in inflation is genuine. The delay in lowering policy rates means that consumers will have to face the disappointing impact of higher mortgage rates for a while longer, which will continue to restrict their ability to buy and sell houses!

Another fascinating research finding is that individuals favoring the opposition party who fail to occupy the White House after an election tend to be much more pessimistic about the economy, even when the economy's performance is improving! This finding applies to both major political parties and may explain why Republicans are more pessimistic about the U.S. economy than Democrats.

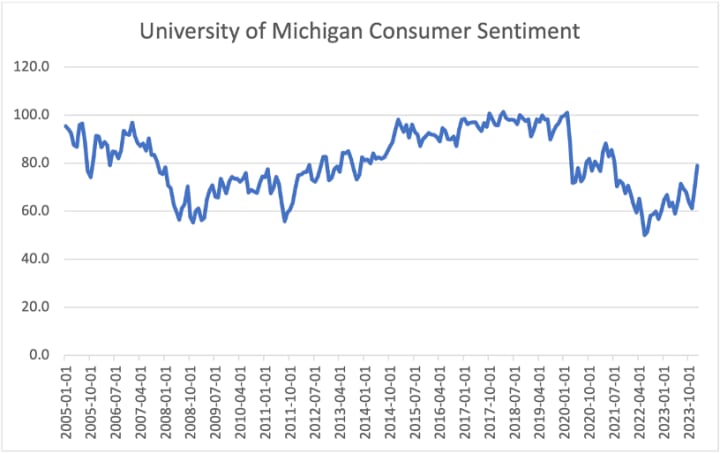

Interestingly, one aspect of this psychological process, namely the lagged effect of lower inflation, may be starting to show up, as evidenced by the latest 9.3-point jump in Consumer Sentiment (Jan. 2024)! It was the most significant monthly increase since a 9.9-point rise in November 2005, albeit the current reading remains sharply below levels observed before the start of the global pandemic!

What Else is Irritating Consumers?

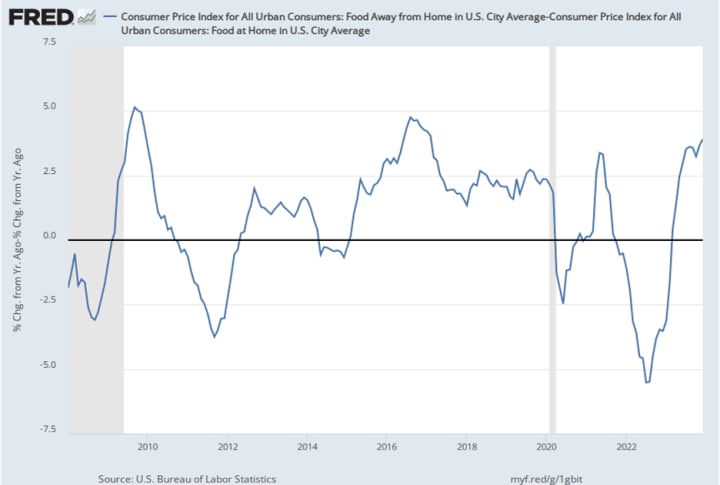

In a world where experiences are meaningful, consumers may be unhappy that food prices away from home (e.g., at restaurants) are rising faster than the cost of preparing the same dishes at home! That has forced consumers to curtail restaurant spending and undoubtedly left a bad taste in their mouths (no pun intended).

Summary and Concluding Thoughts

Despite a tendency to rely on real GDP and national unemployment rate metrics to determine consumer sentiment, recent economic research may explain why many consumers remain pessimistic about the economy. Such research suggests that individuals may be looking at movements in inflation in a risk-averse fashion. As consumers have shifted towards experiential consumption, observing restaurant prices rising faster than the cost of preparing the same dishes at home may also be depressing consumer sentiment.

Additionally, research finds consumers tend to monitor inflation with a lag to ensure that any shift in trends, whether up or down, is permanent. On the political front, economic research also shows that individuals disappointed with a presidential election's outcome may be predisposed to having a negative view of the economy. That means that in a close Presidential election, we should expect higher levels of consumer dissatisfaction irrespective of which political party occupies the White House.

The good news is that if the inflation rate continues to decrease, we should expect a gradual improvement in consumer sentiment. Such green shoots appear to be sprouting in the latest January 2024 University of Michigan Consumer Sentiment reading, which registered its largest monthly jump since Nov. 2005!

About the Creator

Anthony Chan

Chan Economics LLC, Public Speaker

Chief Global Economist & Public Speaker JPM Chase ('94-'19).

Senior Economist Barclays ('91-'94)

Economist, NY Federal Reserve ('89-'91)

Econ. Prof. (Univ. of Dayton, '86-'89)

Ph.D. Economics

Keep reading

More stories from Anthony Chan and writers in Trader and other communities.

The Federal Reserve’s Federal Open Market Committee (FOMC) Will Meet This Week and Ask: “Are We There Yet?”

The answer is that monetary policy is so restrictive that the Fed could justify lowering policy rates. The Fed’s preferred inflation metric, core PCE (which measures consumer prices excluding food and energy components), is now rising at a yearly pace of +2.9% (December 2023), down from a peak growth pace of +5.6% (February 2022). The significant difference between core PCE and core CPI (Consumer Price Index) is that the former weights the price components based on the changing preferences of consumers. Suppose the price of strawberries rises and individuals switch to consuming more blueberries. In that case, blueberries will be weighted more heavily (when constructing the price index) as the shift in demand occurs.

By Anthony Chan4 months ago in Trader

Why the Paxful Clone Script is the Ideal Solution for Crypto Entrepreneurs

Introduction In the ever-evolving world of cryptocurrencies, peer-to-peer (P2P) exchange platforms have surged in popularity due to their decentralized nature and user-centric operations. Among these platforms, Paxful is a standout example. Alphacodez offers a Paxful Clone Script, enabling you to easily create your own P2P crypto exchange platform. This comprehensive guide explores the benefits, features, development process, and more of the Paxful Clone Script by Alphacodez.

By Paul Walker6 days ago in Trader

What Currencies Are Traded in the Forex Market?

The foreign exchange market is the largest global decentralized market where various currency pairs are bought, sold, and exchanged at determined or current prices. Thus, traders need to possess a thorough understanding of the currency pairs that are traded in the Forex market. To simplify, here is an overview of the currency pairs, their types and what are the most traded among them.

By Novak Jovik2 days ago in Trader

Comments

There are no comments for this story

Be the first to respond and start the conversation.